This document summarizes various types of health insurance policies including Mediclaim, Group Mediclaim, Cancer Patients Aid Association policy, Critical Illness Insurance, Overseas Medical policy, and Corporate Frequent Travellers policy. It outlines what is covered and excluded in each policy type, such as reimbursement of hospitalization expenses, waiting periods, claim limits, and eligibility.

Kanoe India Healthcare, A division Of Kanoe Softwares proposes a special Medical insurance plan sponsored by Universal Sompo General insurance Co. Limited in joint venture with Allahabad Bank Limited, Indian Overseas Bank, Karnataka Bank Limited, Dabur Investments Corp and Sompo Japan Insurance Incorporation in Public Private Partnership (PPP), aiming to provide assurance of Government/Public sector and superb, hassle free service from private bodies.

Kanoe India Healthcare, A division Of Kanoe Softwares proposes a special Medical insurance plan sponsored by Universal Sompo General insurance Co. Limited in joint venture with Allahabad Bank Limited, Indian Overseas Bank, Karnataka Bank Limited, Dabur Investments Corp and Sompo Japan Insurance Incorporation in Public Private Partnership (PPP), aiming to provide assurance of Government/Public sector and superb, hassle free service from private bodies.

Health Insurance products can be challenging in today’s insurance environment. LionShare Insurance Group offers a complete line of individual health and life insurance products that are crafted to meet you and your family’s specific needs.

There are three types of health insurance cover available in the market today. These are:

Mediclaim:

These policies cover you for hospitalization expenses. Actual hospitalization expenses are paid subject to a maximum limit of the sum assured opted for. All insurers offer policyholders cashless treatment in their network of hospitals. Policyholders can also pay upfront and then claim reimbursement from the insurer.

We recommend Mediclaim as a basic “must have” health insurance to our customers. Mediclaim can be individual or a family floater. In individual every person has his or her own individual policy. In a family floater the members of a family pay a single premium and have one insurance policy that covers the family. Sometimes parents and in-laws can also be included in the family cover. A floater cover provides a lot of flexibility for the family and normally works out more economical.

Fixed Benefit Cover

These is a new class of insurance products in the Indian market. These plans pay a pre-determined sum of money depending upon the number of days a person is in hospital and the type of surgery done. This amount may be more or less than the actual expenses you incur. We recommend this as an additional insurance to purchase after you have the basic mediclaim policy. Similar to the indemnity cover, fixed benefit cover has individual and family floater options. Fixed benefit policies will pay you the benefit even if the actual costs are reimbursed by a mediclaim policy.

Critical Illness plans

In these plans a fixed sum of money is paid if the person gets certain pre-specified diseases. Plans can cover anywhere from 9 to 35 diseases. In our view these plans are best bought after one has the basic medicliam and fixed benefit plans. They are ideal for diseases that are debilitating but may not require constant hospitalization - for example cancer or renal failure.

Each of the insurance plans described here can be taken for a single Individual or may include dependents such as the spouse, minor children, parents, parents-in-law, grandparents and grandchildren.

Arogya Sanjeevani Policy From Future GeneraliColinGenerali

Arogya Sanjeevani Policy, Future Generali India insurance company limited is an affordable health insurance policy that covers the entire family. Secure your family with affordable health insurance policies.

Health Insurance products can be challenging in today’s insurance environment. LionShare Insurance Group offers a complete line of individual health and life insurance products that are crafted to meet you and your family’s specific needs.

There are three types of health insurance cover available in the market today. These are:

Mediclaim:

These policies cover you for hospitalization expenses. Actual hospitalization expenses are paid subject to a maximum limit of the sum assured opted for. All insurers offer policyholders cashless treatment in their network of hospitals. Policyholders can also pay upfront and then claim reimbursement from the insurer.

We recommend Mediclaim as a basic “must have” health insurance to our customers. Mediclaim can be individual or a family floater. In individual every person has his or her own individual policy. In a family floater the members of a family pay a single premium and have one insurance policy that covers the family. Sometimes parents and in-laws can also be included in the family cover. A floater cover provides a lot of flexibility for the family and normally works out more economical.

Fixed Benefit Cover

These is a new class of insurance products in the Indian market. These plans pay a pre-determined sum of money depending upon the number of days a person is in hospital and the type of surgery done. This amount may be more or less than the actual expenses you incur. We recommend this as an additional insurance to purchase after you have the basic mediclaim policy. Similar to the indemnity cover, fixed benefit cover has individual and family floater options. Fixed benefit policies will pay you the benefit even if the actual costs are reimbursed by a mediclaim policy.

Critical Illness plans

In these plans a fixed sum of money is paid if the person gets certain pre-specified diseases. Plans can cover anywhere from 9 to 35 diseases. In our view these plans are best bought after one has the basic medicliam and fixed benefit plans. They are ideal for diseases that are debilitating but may not require constant hospitalization - for example cancer or renal failure.

Each of the insurance plans described here can be taken for a single Individual or may include dependents such as the spouse, minor children, parents, parents-in-law, grandparents and grandchildren.

Arogya Sanjeevani Policy From Future GeneraliColinGenerali

Arogya Sanjeevani Policy, Future Generali India insurance company limited is an affordable health insurance policy that covers the entire family. Secure your family with affordable health insurance policies.

Maxima is a plan that takes care of your everyday health needs. It is an easy to buy plan that covers expenses incurred in the form of Doctors’ consultations, Pharmacy bills, Diagnostic tests, Dental treatment, Optical services and Annual health check-up. Maxima health plan by Apollo Munich offers comprehensive coverage while taking care of little illnesses too. Along with wide inpatient coverage, Maxima also offer benefits with unique outpatient coverage. With additional critical illness coverage and provision of lifelong renewal, the plan makes insurance coverage feasible at affordable premium rates. Get self as well as your family members insured under this easy to understand plan and enjoy a stress free health future.

Explore the ManipalCigna Lifestyle Protection - Critical Care Prospectus to understand the features and coverage options of the Critical Illness Insurance Policy. Choose between Basic and Enhanced plans offering coverage for a range of critical illnesses, including cancer, heart attack, stroke, organ failure, and more.

More Health Insurance Policy Wording by Reliance Health Insurance. MORE as a product primarily aims in making make health insurance Easy-to-choose, Easy-to-buy and Easy-to-use.

Buy here: https://www.reliancehealthinsurance.com/buy-health-insurance-plans-online.html

Future Advantage Top-Up - Give Your Health Insurance A Backup Plan From Futur...ColinGenerali

Future Advantage Top-Up is a deductible health insurance plan with high Sum Insured options to provide extra coverage at low premium as compared to any traditional health insurance plan.

At L&T Insurance, we put ourselves in your shoes and keep every detail in mind while designing your health plan. We understand that your family’s health is most

precious to you. Which is why we offer you a thoughtful and holistic health insurance plan to reduce your concerns and let you enjoy absolute peace of mind.

NVBDCP.pptx Nation vector borne disease control programSapna Thakur

NVBDCP was launched in 2003-2004 . Vector-Borne Disease: Disease that results from an infection transmitted to humans and other animals by blood-feeding arthropods, such as mosquitoes, ticks, and fleas. Examples of vector-borne diseases include Dengue fever, West Nile Virus, Lyme disease, and malaria.

Tom Selleck Health: A Comprehensive Look at the Iconic Actor’s Wellness Journeygreendigital

Tom Selleck, an enduring figure in Hollywood. has captivated audiences for decades with his rugged charm, iconic moustache. and memorable roles in television and film. From his breakout role as Thomas Magnum in Magnum P.I. to his current portrayal of Frank Reagan in Blue Bloods. Selleck's career has spanned over 50 years. But beyond his professional achievements. fans have often been curious about Tom Selleck Health. especially as he has aged in the public eye.

Follow us on: Pinterest

Introduction

Many have been interested in Tom Selleck health. not only because of his enduring presence on screen but also because of the challenges. and lifestyle choices he has faced and made over the years. This article delves into the various aspects of Tom Selleck health. exploring his fitness regimen, diet, mental health. and the challenges he has encountered as he ages. We'll look at how he maintains his well-being. the health issues he has faced, and his approach to ageing .

Early Life and Career

Childhood and Athletic Beginnings

Tom Selleck was born on January 29, 1945, in Detroit, Michigan, and grew up in Sherman Oaks, California. From an early age, he was involved in sports, particularly basketball. which played a significant role in his physical development. His athletic pursuits continued into college. where he attended the University of Southern California (USC) on a basketball scholarship. This early involvement in sports laid a strong foundation for his physical health and disciplined lifestyle.

Transition to Acting

Selleck's transition from an athlete to an actor came with its physical demands. His first significant role in "Magnum P.I." required him to perform various stunts and maintain a fit appearance. This role, which he played from 1980 to 1988. necessitated a rigorous fitness routine to meet the show's demands. setting the stage for his long-term commitment to health and wellness.

Fitness Regimen

Workout Routine

Tom Selleck health and fitness regimen has evolved. adapting to his changing roles and age. During his "Magnum, P.I." days. Selleck's workouts were intense and focused on building and maintaining muscle mass. His routine included weightlifting, cardiovascular exercises. and specific training for the stunts he performed on the show.

Selleck adjusted his fitness routine as he aged to suit his body's needs. Today, his workouts focus on maintaining flexibility, strength, and cardiovascular health. He incorporates low-impact exercises such as swimming, walking, and light weightlifting. This balanced approach helps him stay fit without putting undue strain on his joints and muscles.

Importance of Flexibility and Mobility

In recent years, Selleck has emphasized the importance of flexibility and mobility in his fitness regimen. Understanding the natural decline in muscle mass and joint flexibility with age. he includes stretching and yoga in his routine. These practices help prevent injuries, improve posture, and maintain mobilit

Recomendações da OMS sobre cuidados maternos e neonatais para uma experiência pós-natal positiva.

Em consonância com os ODS – Objetivos do Desenvolvimento Sustentável e a Estratégia Global para a Saúde das Mulheres, Crianças e Adolescentes, e aplicando uma abordagem baseada nos direitos humanos, os esforços de cuidados pós-natais devem expandir-se para além da cobertura e da simples sobrevivência, de modo a incluir cuidados de qualidade.

Estas diretrizes visam melhorar a qualidade dos cuidados pós-natais essenciais e de rotina prestados às mulheres e aos recém-nascidos, com o objetivo final de melhorar a saúde e o bem-estar materno e neonatal.

Uma “experiência pós-natal positiva” é um resultado importante para todas as mulheres que dão à luz e para os seus recém-nascidos, estabelecendo as bases para a melhoria da saúde e do bem-estar a curto e longo prazo. Uma experiência pós-natal positiva é definida como aquela em que as mulheres, pessoas que gestam, os recém-nascidos, os casais, os pais, os cuidadores e as famílias recebem informação consistente, garantia e apoio de profissionais de saúde motivados; e onde um sistema de saúde flexível e com recursos reconheça as necessidades das mulheres e dos bebês e respeite o seu contexto cultural.

Estas diretrizes consolidadas apresentam algumas recomendações novas e já bem fundamentadas sobre cuidados pós-natais de rotina para mulheres e neonatos que recebem cuidados no pós-parto em unidades de saúde ou na comunidade, independentemente dos recursos disponíveis.

É fornecido um conjunto abrangente de recomendações para cuidados durante o período puerperal, com ênfase nos cuidados essenciais que todas as mulheres e recém-nascidos devem receber, e com a devida atenção à qualidade dos cuidados; isto é, a entrega e a experiência do cuidado recebido. Estas diretrizes atualizam e ampliam as recomendações da OMS de 2014 sobre cuidados pós-natais da mãe e do recém-nascido e complementam as atuais diretrizes da OMS sobre a gestão de complicações pós-natais.

O estabelecimento da amamentação e o manejo das principais intercorrências é contemplada.

Recomendamos muito.

Vamos discutir essas recomendações no nosso curso de pós-graduação em Aleitamento no Instituto Ciclos.

Esta publicação só está disponível em inglês até o momento.

Prof. Marcus Renato de Carvalho

www.agostodourado.com

Ozempic: Preoperative Management of Patients on GLP-1 Receptor Agonists Saeid Safari

Preoperative Management of Patients on GLP-1 Receptor Agonists like Ozempic and Semiglutide

ASA GUIDELINE

NYSORA Guideline

2 Case Reports of Gastric Ultrasound

Pulmonary Thromboembolism - etilogy, types, medical- Surgical and nursing man...VarunMahajani

Disruption of blood supply to lung alveoli due to blockage of one or more pulmonary blood vessels is called as Pulmonary thromboembolism. In this presentation we will discuss its causes, types and its management in depth.

These simplified slides by Dr. Sidra Arshad present an overview of the non-respiratory functions of the respiratory tract.

Learning objectives:

1. Enlist the non-respiratory functions of the respiratory tract

2. Briefly explain how these functions are carried out

3. Discuss the significance of dead space

4. Differentiate between minute ventilation and alveolar ventilation

5. Describe the cough and sneeze reflexes

Study Resources:

1. Chapter 39, Guyton and Hall Textbook of Medical Physiology, 14th edition

2. Chapter 34, Ganong’s Review of Medical Physiology, 26th edition

3. Chapter 17, Human Physiology by Lauralee Sherwood, 9th edition

4. Non-respiratory functions of the lungs https://academic.oup.com/bjaed/article/13/3/98/278874

HOT NEW PRODUCT! BIG SALES FAST SHIPPING NOW FROM CHINA!! EU KU DB BK substit...GL Anaacs

Contact us if you are interested:

Email / Skype : kefaya1771@gmail.com

Threema: PXHY5PDH

New BATCH Ku !!! MUCH IN DEMAND FAST SALE EVERY BATCH HAPPY GOOD EFFECT BIG BATCH !

Contact me on Threema or skype to start big business!!

Hot-sale products:

NEW HOT EUTYLONE WHITE CRYSTAL!!

5cl-adba precursor (semi finished )

5cl-adba raw materials

ADBB precursor (semi finished )

ADBB raw materials

APVP powder

5fadb/4f-adb

Jwh018 / Jwh210

Eutylone crystal

Protonitazene (hydrochloride) CAS: 119276-01-6

Flubrotizolam CAS: 57801-95-3

Metonitazene CAS: 14680-51-4

Payment terms: Western Union,MoneyGram,Bitcoin or USDT.

Deliver Time: Usually 7-15days

Shipping method: FedEx, TNT, DHL,UPS etc.Our deliveries are 100% safe, fast, reliable and discreet.

Samples will be sent for your evaluation!If you are interested in, please contact me, let's talk details.

We specializes in exporting high quality Research chemical, medical intermediate, Pharmaceutical chemicals and so on. Products are exported to USA, Canada, France, Korea, Japan,Russia, Southeast Asia and other countries.

Flu Vaccine Alert in Bangalore Karnatakaaddon Scans

As flu season approaches, health officials in Bangalore, Karnataka, are urging residents to get their flu vaccinations. The seasonal flu, while common, can lead to severe health complications, particularly for vulnerable populations such as young children, the elderly, and those with underlying health conditions.

Dr. Vidisha Kumari, a leading epidemiologist in Bangalore, emphasizes the importance of getting vaccinated. "The flu vaccine is our best defense against the influenza virus. It not only protects individuals but also helps prevent the spread of the virus in our communities," he says.

This year, the flu season is expected to coincide with a potential increase in other respiratory illnesses. The Karnataka Health Department has launched an awareness campaign highlighting the significance of flu vaccinations. They have set up multiple vaccination centers across Bangalore, making it convenient for residents to receive their shots.

To encourage widespread vaccination, the government is also collaborating with local schools, workplaces, and community centers to facilitate vaccination drives. Special attention is being given to ensuring that the vaccine is accessible to all, including marginalized communities who may have limited access to healthcare.

Residents are reminded that the flu vaccine is safe and effective. Common side effects are mild and may include soreness at the injection site, mild fever, or muscle aches. These side effects are generally short-lived and far less severe than the flu itself.

Healthcare providers are also stressing the importance of continuing COVID-19 precautions. Wearing masks, practicing good hand hygiene, and maintaining social distancing are still crucial, especially in crowded places.

Protect yourself and your loved ones by getting vaccinated. Together, we can help keep Bangalore healthy and safe this flu season. For more information on vaccination centers and schedules, residents can visit the Karnataka Health Department’s official website or follow their social media pages.

Stay informed, stay safe, and get your flu shot today!

Maxilla, Mandible & Hyoid Bone & Clinical Correlations by Dr. RIG.pptx

10. health ins.

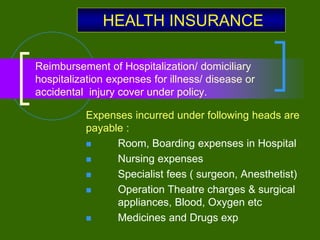

1. Expenses incurred under following heads are

payable :

Room, Boarding expenses in Hospital

Nursing expenses

Specialist fees ( surgeon, Anesthetist)

Operation Theatre charges & surgical

appliances, Blood, Oxygen etc

Medicines and Drugs exp

HEALTH INSURANCE

Reimbursement of Hospitalization/ domiciliary

hospitalization expenses for illness/ disease or

accidental injury cover under policy.

2. Expenses on hospitalization for a minimum period of

24 hours are admissible.

Following types of specific treatment are exempted

from min.24 hours stay in hospital :

-Dialysis, chemotherapy, Radiotherapy,

Eye surgery, Dental surgery, lithotripsy etc.

The criteria has to be satisfied by a hospital/ nursing

A) Registration with local authorities

b) Operation theatre

c) doctors and nursing staff round the clock

3. Special Features of Mediclaim

policy

The costs “ Artificial limbs” are payable under

Mediclaim policy.

Relevant medical expenses incurred during the period

of 60 days after hospitalization and 30 days prior to

hospitalization are treated as part of the claim.

‘Tonsilitis’ diseases is excluded under Domiciliary

Hospitalization benefit.

Epilepsy disease is not excluded during the first year

of operation of policy.

4. Exclusions :

Under medicalim policy any disease contracted by the

insured during the first 30 days from the

commenceement of policy is excluded

All pre-existing diseases are not cover incepts for the

first time.

‘Hernia’ disease is excluded during the first year of

operation of mediclaim policy.

Cataract, fibromyoma, Hydrocele, Fistuala in anus,

Piles, Sinusitis and related disorders also not covered

during first year of operation policy.

5. Cost of spectacles, contact lenses & hearing machine

Dental treatment & cosmetic surgery (but it is

payable if necessitated due to an accident)

Expenses on vitamins and tonics are excluded unless

forming part of treatment.

Voluntary termination of pregnancy, caesarian

section & childbirth.

Naturopathy treatment.

6. • Cumulative bonus : The sum insured is

increased by 5% for each claim free year of

insurance subject to maximum 10 years.

Cost of Health checkup :

Reimbursement of medical check up once in

every 4 years subject to no claim preferred.

Age Limit : Between the ages of 5 yrs to 80 years.

Sum insured and premium :

The sum insured is decided by the insured. S.I. is

usually available from Rs.15,000 to Rs.5,00,000.

Tax benefit is available under section 80-D of income

Tax Act.

7. Family discount: 5% discount in the total premium

is allowed to a family comprising the insured and

a) spouse, b) dependent children

c) Dependent parents.

Proposal Form : Following information are required

in proposal form-

a) Average Monthly income

b) Past diseases and treatment

c) Income tax Pan

8. GROUP MEDICLAIM POLICY

A group Mediclaim is available to any group, subject to

the following :

a) The group has a centrl administration point.

b) The prescribed number of persons are covered.

Group policy is issued in the name of Group/

association/ Institution/ corporate body called insured.

The coverage under the policy is the same as under

individual Mediclaim policy with the following

differences :

9. Cumulative bonus & health check up expenses are

not payable.

Group discount in the premium is available.

(cumulative bonus not available)

Renewal premium is subject to Bonus/malus clause

Maternity benefit extension is available at extra prem.

1) A waiting period of 9 months is applicable

for payment off a Maternity claim.

2) Maternity extension is payable only for first

two children.

3) Pre-natal expenses prior to hospitalization

is not payable.

10. This policy is granted to members of the Cancer

Patients Aid Association (CPAA).

The premium is payable to CPAA as part of he

membership fee.

No claim is payable if the insured contracts cancer

within a period of 30 days from the date of becoming

a member of CPAA.

The sum insured is increased by 5% for each

completed year of policy in force prior to claim.

Differences as to the claim are to be referred to

committee set up by CPAA and the insurance co.

Cancer Patients Aid Association Policy

11. Critical Illness Insurance

A critical illness shall means selected diseases by

Insured as like Cancer, Paralysis, Parkinson’s Disease

etc.

Tuberculosis is not specified.

Any critical illness discovered with 90 days of the

inception date of the policy is not covered.

12. Overseas Medical policy

Overseas Medical Policy can be granted

to Indian Resident undertaking bonafide trips for

following purposes :

a) Business & Official purposes

b) Holiday

c) Employment

d) Studies

Age : For adult upto 70 years beyond 70 years is

granted at extra premium.

For children age of 6 months to 5 years are

covered.

13. Period of insurance : Insurance is valid from the

first day of insurance or date and time of

departure from India whichever is later and

expires on the last day of the number of days

specified in the policy or on return to India

whichever is earlier.

Extension of the period of insurance automatic, for

the period not exceeding 7 days and without extra.

14. Risks covered under Policy : (6 Sections)

A) Medical expenses

B) Personal Accident

C) Loss of checked baggage

D) Delay of checked Baggage

E) Loss of passport

F) Personal liability

15. Cosmetic surgery necessary as a result of a covered

accident is not excluded under policy.

Dental services for immediate relief of dental pain

only is not paid upto the full limit of cover under

policy

Permanent partial Disablement is not covered under

Personal Accident section.

Emergency purchase of replacement items is paid if

there is delay or more than 12 hours in delivery of

Baggage

16. •

Under loss of checked baggage, the claim of following

items is not payable :

a) Binolculars,. B) Sun-glasses c) Antiques

Policy does not operate beyond a period of 180 days

continuous absence.

Under Personal Accident section of the policy,

deductible does not apply.

17. Corporate Frequent Travellers Policy

Corporate Frequent Travellers policy is grangted to

a) Officials of companies registered under the Companies Act.

b) Partners of registered firms.

The duration of any one trip under annual policy not to exceed

60 days.

Under world-wide travel Plan, the deposit premium is equal to

premium of at least 500 days.

Employees above 60 years of age have to submit the prescribed

Medical report.

Personal Liability is not covered for Employment & study

purpose policy.