1. 370 FinanceAction:

in Financial

Statements

a Performanca: successfully the business

How is beingrun asa tradingconcern? Here

we are concerned so muchwith profit aswitlr profitability.How well is the

not

company usingthe capitalit employs generate

to sales andin turn profits?

t Filtancinlstarrr: Is the gqqrpanysolvent*O tiqt qt.Is it financiallysound?

Tlie ratioscalculated eachofthesecategories

i! haverels'vance-foi differentstakehold-

ers. Shareholders, potentialinvestors, particularlyconcerned

and are wjth the invest-

ment ratios.Performance ratiostell the strategicleaderhowwell the company doing

is

as a busines. Bankersand other providersof loan capitalwill want to know that the

business solventand liquid in additionto howwell it is performing.

is

This form of analysis mostrelevantfor profit-seeking

is businesses,althoughsomeof

the measures provequite enlightening

can whenappliedto not-for-profitorganizations.

Ratiosarecalculated from thepublished accounts organizations, an analysis

of but of

just one setof resultswill only be partly helpfirl.Tiendsareparticularly important,and

thereforethe changes resultsover a numberof yearsshouldbe evaluated.

in Care

shouldbe takento ensurethat the resultsarenot considered isolationfrom external

in

trendsin the economy industry.For example, company's

or the salesmay be growing

quickly,but how do they compare with thoseof their competitors the industryasa

and

whole?Similarly,slow growth may be explained industrycontraction,althoughin

by

turn this might indicatethe needfor diversification.

Hence,industryaverages,and competitorperformance shouldbe usedfor compar-

isons.One problemhere is that different companies present

may their accounts dif-

in

ferent ways and the figures will have to be interpreted before any meaningful

comparisons be made.Furthermore, industry

can the maybe composed companies

of of

varyingsizes variousdegrees conglomeration diversification. this reason

and of and For

certaincompanies be expected behave

may to differentlyfrom their competitors.

In addition,it can be usefulto comparethe actualresultswith forecasts, although

thesewill not normallybe available peopleoutsidethe organization. usefulness

to The

is dependent howwell the forecasts budgets

on and wereprepared.

(

b

p

Financial

statements

The two most important statements

usedfor calculating ratios are the profit and loss

accountandthe balance sheet,simplifiedversions which are illustratedin Tables

of 7.6

and7.7,The full accountsmaybe requiredin order to makecertainadjustments. o

t

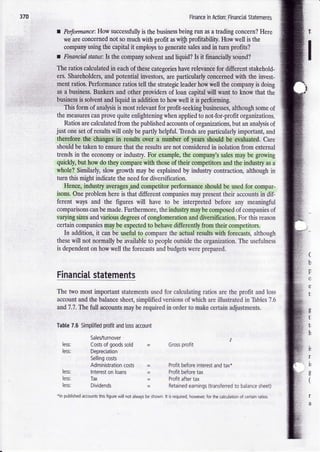

profit

Table Simptified andloss

7.6 account tr

h

5aleVturnover

less: Costs goods

of sold profit

Gross

lt

less: Depreciation

( pllinn r n< tc

i,

Administration

costs Profit

before interest tax*

and tl

reSs: lnterest loans

on Profit

before tax o

c

less: Tax Profit

aftertax (

less: Dividends Retainedearnings (transfened balance

to sheet)

*ln published

accounts figurewill

this not always shown.lt is required,

be however, the calculation certain

for of ratios.