Downloaded 2,450 times

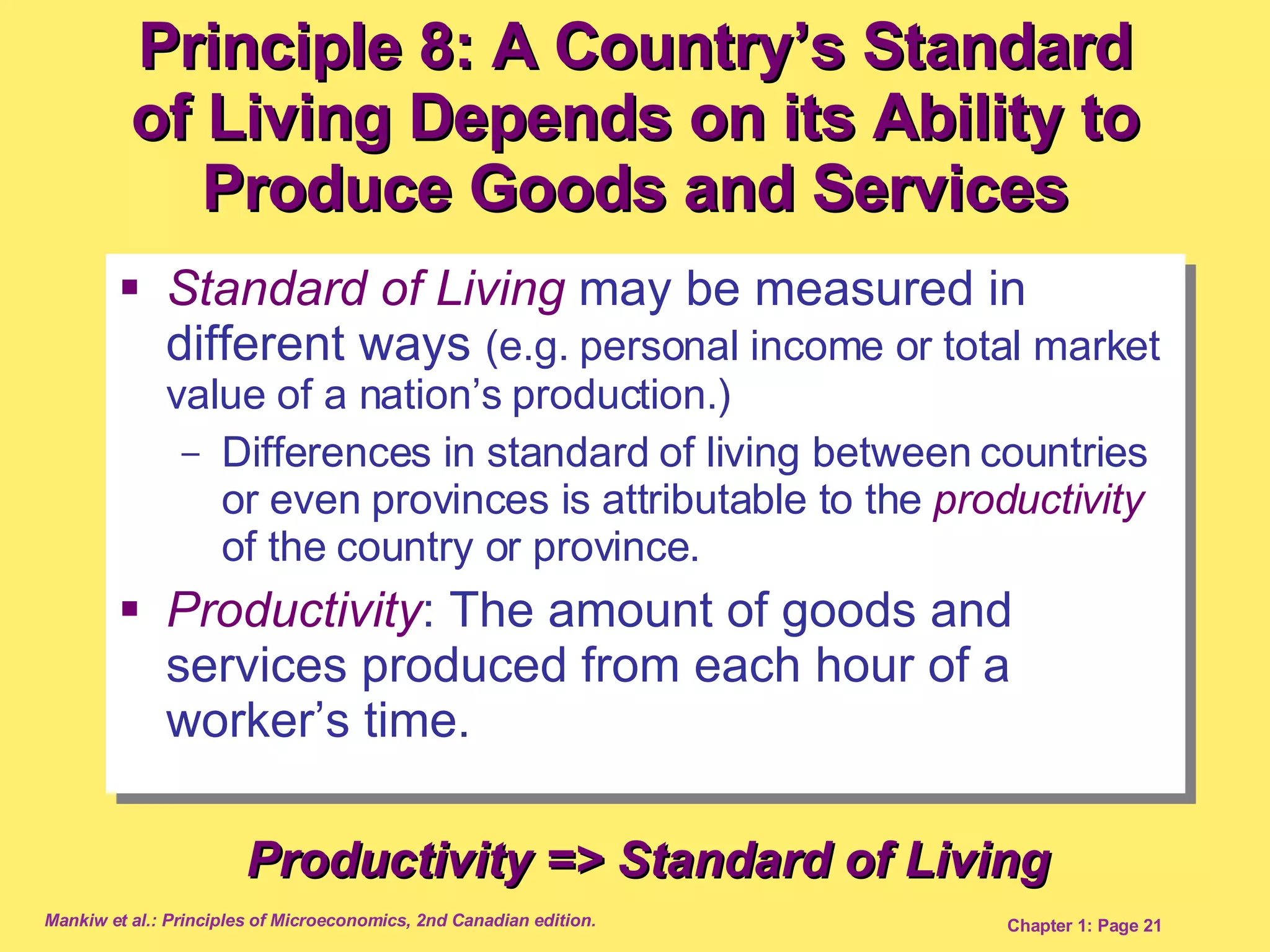

The document outlines 10 principles of economics: 1) People face tradeoffs when making decisions; 2) The cost of something is what you give up to get it; 3) Rational people think at the margin by comparing marginal costs and benefits; 4) People respond to incentives. Trade can make everyone better off and markets are generally a good way to organize economic activity, though governments can improve outcomes during market failures. A country's productivity determines its standard of living. Inflation results from too much money printing by the government, and there is a short-run tradeoff between inflation and unemployment.