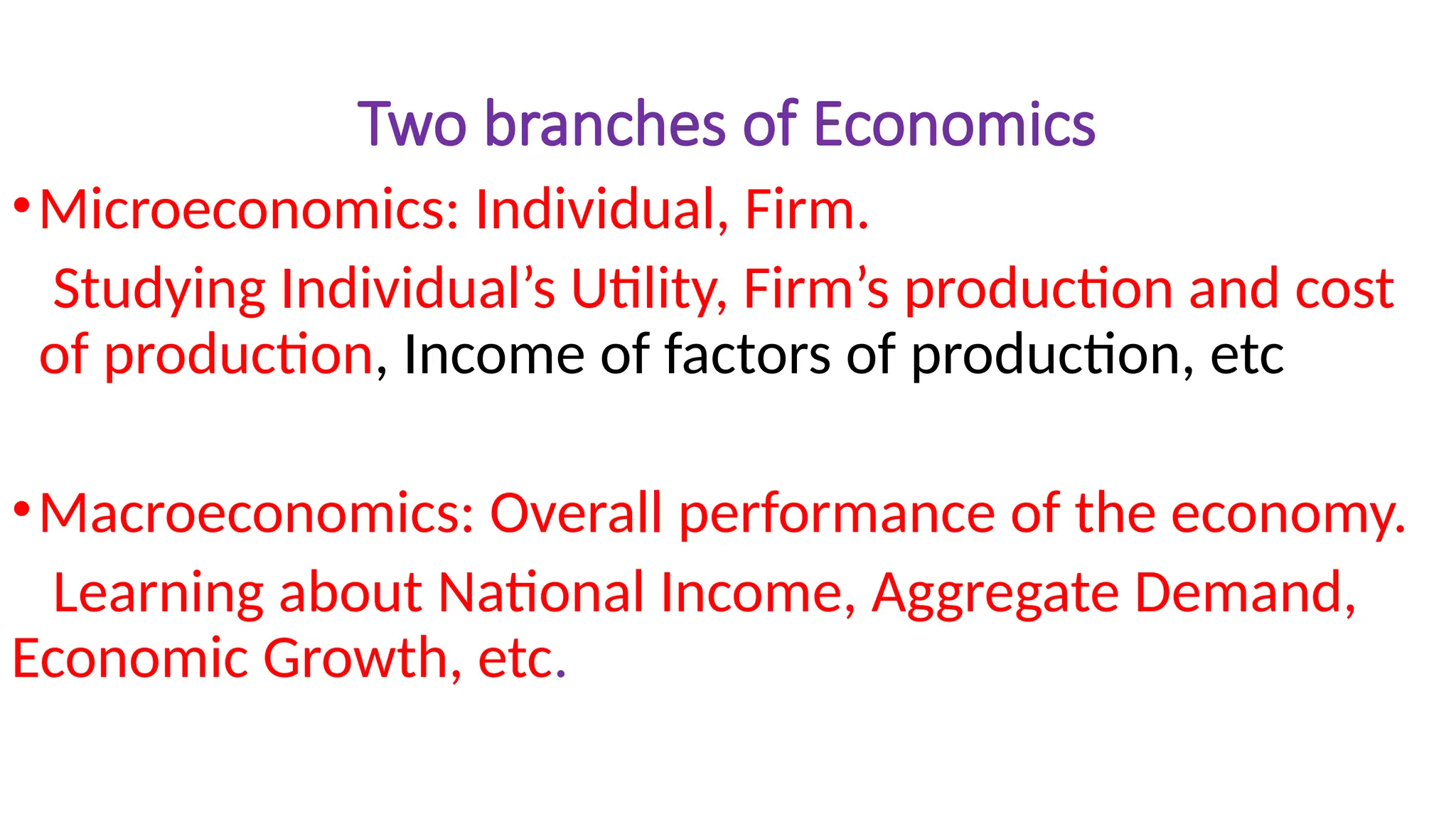

The document outlines key economic concepts, describing the economy as the process of production and consumption guided by principles of efficiency and the allocation of scarce resources. It distinguishes between microeconomics and macroeconomics and introduces ten fundamental principles of economics, such as trade-offs, the cost of alternatives, and the impact of incentives. Additionally, it explores the roles of markets and government in improving economic outcomes and addresses factors influencing living standards and inflation.