Centro Property - Why is the Balance Sheet classified?

•Download as PPTX, PDF•

1 like•700 views

VCE Accounting

Recommended

Recommended

More Related Content

What's hot

What's hot (12)

Viewers also liked

Viewers also liked (20)

Similar to Centro Property - Why is the Balance Sheet classified?

Similar to Centro Property - Why is the Balance Sheet classified? (20)

More from VCE Accounting - Michael Allison

More from VCE Accounting - Michael Allison (20)

Recently uploaded

Recently uploaded (20)

Centro Property - Why is the Balance Sheet classified?

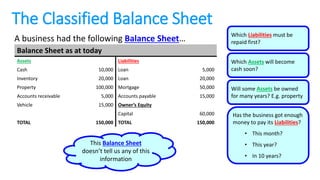

- 1. The Classified Balance Sheet A business had the following Balance Sheet… Balance Sheet as at today Assets Liabilities Cash 10,000 Loan 5,000 Inventory 20,000 Loan 20,000 Property 100,000 Mortgage 50,000 Accounts receivable 5,000 Accounts payable 15,000 Vehicle 15,000 Owner’s Equity Capital 60,000 TOTAL 150,000 TOTAL 150,000 Which Liabilities must be repaid first? Which Assets will become cash soon? Will some Assets be owned for many years? E.g. property Has the business got enough money to pay its Liabilities? • This month? • This year? • In 10 years? This Balance Sheet doesn’t tell us any of this information

- 2. The Classified Balance Sheet Rather than appearing as one big group, each item in the Balance Sheet must be classified Current Assets: assets that will be turned into cash or used within the next 12 months, e.g. • Cash • Inventory (stock) • Accounts receivable (debtors ) Current Liabilities: debts that must be repaid within the next 12 months, e.g. • Bills and expenses (e.g. phone, power, taxes) • Short-term loans • Accounts payable (creditors) Assets Non-Current Assets: assets that the business will own beyond the next 12 months, e.g. • Property • Vehicles Non-Current Liabilities: debts that will be repaid after the next 12 months, e.g. • Long-term loans • Mortgages Liabilities

- 3. The Classified Balance Sheet Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 15,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 15,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 15,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 15,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 15,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 15,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 15,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 20,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 20,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 20,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 20,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Balance Sheet as at today Current Assets Current Liabilities Cash 10,000 Loan – due 180 days 5,000 Inventory 20,000 Accounts payable 15,000 20,000 Accounts receivable 5,000 35,000 Non-Current Liabilities Loan – due 10 years 20,000 Mortgage 50,000 70,000 Non-Current Assets Property 100,000 Owner’s Equity Vehicle 15,000 115,000 Capital 60,000 TOTAL 150,000 TOTAL 150,000 Which Liabilities must be repaid first? Which Assets will become cash soon? Will some Assets be owned for many years? E.g. property Has the business got enough money to pay its Liabilities? • This month? • This year? • In 10 years?

- 4. Why is the Balance Sheet Classified? Which business would you rather be? Business A LiabilitiesAssets Current Non- Current Total $100,000 $50,000 $50,000 $70,000 $10,000 $60,000 Business B LiabilitiesAssets $100,000 $80,000 $20,000 $70,000 $60,000 $10,000 Relevance Information is relevant if it influences the decision-making of the user by helping them: • Evaluate past, present or future decisions • Confirm or correct past decisions Having the classified information enables the firm to make decisions such as: • How will we finance our Current Liabilities? • Should we sell some of our Non- Current Assets? • Should the owner provide a capital contribution? • Which business should I buy? • Which business should I sell to? • Which business should I lend to?

- 5. Centro Properties Centro own and operate shopping centres in Australia and New Zealand

- 6. Centro Properties For the 2006-07 financial year, Centro released their Balance Sheet as follows… Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 0 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 656.6 Non-Current Assets Non-Current Liabilities Investments 3,748.9 Creditors 54.2 Financial assets 2,116,4 Loans 3,603.8 Property 392.2 Other debts 283.7 Plant and equipment 14.0 Provisions 1.7 3,943.4 Intangible assets 555.2 Owner’s Equity Receivables 325 6,827.1 Capital 3,565.1 Total Assets 8,165.1 Total Equities 8,165.1

- 7. Centro Properties • But then a few months later the company announced that it needed to restate the figures in its Balance Sheet • Specifically, a $1.1 billion loan from JP Morgan was originally classified as Non-Current when in fact it was Current and due in 3 months Current Liabilities $ $ Creditors 263.3 Loans 0 Financial instruments 215.7 Provisions 177.5 656.6 Non-Current Liabilities Creditors 54.2 Loans 3,603.8 Other debts 283.7 Provisions 1.7 3,943.4 Listed in here Current Liabilitiesc $ $ Creditors 263.3 Loans 1,096.9 Financial instruments 215.7 Provisions 177.5 1,753.4 Non-Current Liabilities Creditors 54.2 Loans 2,506.8 Other debts 283.7 Provisions 1.7 2,846.4

- 8. Centro Properties Updated Balance Sheet… Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 0 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 656.6 Non-Current Assets Non-Current Liabilities Investments 3,748.9 Creditors 54.2 Financial assets 2,116,4 Loans 3,603.8 Property 392.2 Other debts 283.7 Plant and equipment 14.0 Provisions 1.7 3,943.4 Intangible assets 555.2 Owner’s Equity Receivables 325 6,827.1 Capital 3,565.1 Total Assets 8,165.1 Total Equities 8,165.1 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 1,096.9 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 656.6 Non-Current Assets Non-Current Liabilities Investments 3,748.9 Creditors 54.2 Financial assets 2,116,4 Loans 3,603.8 Property 392.2 Other debts 283.7 Plant and equipment 14.0 Provisions 1.7 3,943.4 Intangible assets 555.2 Owner’s Equity Receivables 325 6,827.1 Capital 3,565.1 Total Assets 8,165.1 Total Equities 8,165.1 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 1,096.9 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 1,753.4 Non-Current Assets Non-Current Liabilities Investments 3,748.9 Creditors 54.2 Financial assets 2,116,4 Loans 3,603.8 Property 392.2 Other debts 283.7 Plant and equipment 14.0 Provisions 1.7 3,943.4 Intangible assets 555.2 Owner’s Equity Receivables 325 6,827.1 Capital 3,565.1 Total Assets 8,165.1 Total Equities 8,165.1 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 1,096.9 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 1,753.4 Non-Current Assets Non-Current Liabilities Investments 3,748.9 Creditors 54.2 Financial assets 2,116,4 Loans 2,506.8 Property 392.2 Other debts 283.7 Plant and equipment 14.0 Provisions 1.7 3,943.4 Intangible assets 555.2 Owner’s Equity Receivables 325 6,827.1 Capital 3,565.1 Total Assets 8,165.1 Total Equities 8,165.1 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 1,096.9 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 1,753.4 Non-Current Assets Non-Current Liabilities Investments 3,748.9 Creditors 54.2 Financial assets 2,116,4 Loans 2,506.8 Property 392.2 Other debts 283.7 Plant and equipment 14.0 Provisions 1.7 2,846.4 Intangible assets 555.2 Owner’s Equity Receivables 325 6,827.1 Capital 3,565.1 Total Assets 8,165.1 Total Equities 8,165.1 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 1,096.9 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 1,753.4 Non-Current Assets Non-Current Liabilities Investments 3,748.9 Creditors 54.2 Financial assets 2,116,4 Loans 2,506.8 Property 392.2 Other debts 283.7 Plant and equipment 14.0 Provisions 1.7 2,846.4 Intangible assets 555.2 Owner’s Equity Receivables 325 6,827.1 Capital 3,565.1 Total Assets 8,165.1 Total Equities 8,165.1

- 9. Impact of the New Classification Negative impact on the firm’s liquidity. The ability of the business to meet its short-term debts as they fall due. Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 1,096.9 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 1,753.4 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 0 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 656.6 1st Balance Sheet 2nd Balance Sheet Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 0 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 656.6 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 1,096.9 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 1,753.4

- 10. Impact of the New Classification Current Assets Current Liabilities WCR = = 2.04 Working Capital Ratio (WCR) = a measure of liquidity 1st Balance Sheet 2nd Balance Sheet Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 0 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 656.6 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 1,096.9 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 1,753.4 1,338.0 656.6 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 0 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 656.6 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 0 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 656.6 Current Assets Current Liabilities WCR = = 0.76 1,338.0 1,753.4 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 1,096.9 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 1,753.4 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 Creditors 263.3 Debtors 361.2 Loans 1,096.9 Assets for sale 785.4 1,338.0 Financial instruments 215.7 Provisions 177.5 1,753.4 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 $1.00Debtors 361.2 Assets for sale 785.4 1,338.0 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ $2.04 $1.00 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ Cash 191.4 $1.00Debtors 361.2 Assets for sale 785.4 1,338.0 Centro Properties: Balance Sheet as at 30 June 2007 (in $ millions) Current Assets $ $ Current Liabilities $ $ $0.76 $1.00 What does this mean? For every $1 of Current Liabilities the firm has, the business has $2.04 in Current Assets to pay them What does this mean? For every $1 of Current Liabilities the firm has, the business has $0.76 in Current Assets to pay them

- 11. Impact of the New Classification $- $1.00 $2.00 $3.00 $4.00 $5.00 $6.00 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 Centro Properties Share Price - December 2007 Day of announcement of error in Balance Sheet

- 12. Centro Properties • The company nearly went bankrupt – changed its name to Federation Centres • The Australian Securities and Investment Commission (ASIC) sued the 7 Directors on Centro’s board • Charged for breaching their “fiduciary duty” to properly scrutinise Centro’s financial reports Sam Kavourakis Audit Committee $167,195 Paul Cooper Audit Committee $104,231 Jim Hall Audit Committee $151,105 Graham Goldie Compliance $158,062 Peter Wilkinson Compliance $104,231 Andrew Scott CEO $3,586,854 Brian Healey Chairman $389,840 GUILTY GUILTY GUILTY GUILTYGUILTY GUILTYGUILTY $0 Fine $0 Fine $0 Fine $0 Fine$0 Fine $30k Fine$0 Fine No Ban No Ban No Ban No BanNo Ban No BanNo Ban

- 13. Questions to Answer • What is a classified Balance Sheet? • Why is a classified Balance Sheet prepared and what does this have to do with Relevance? • What mistake did Centro Properties make when classifying the $1.1 billion loan in the first Balance Sheet? • How did this mistake impact Centro’s liquidity in terms of its Working Capital Ratio?