Downloaded 17 times

![www.mymuneemji.comwww.mymuneemji.com

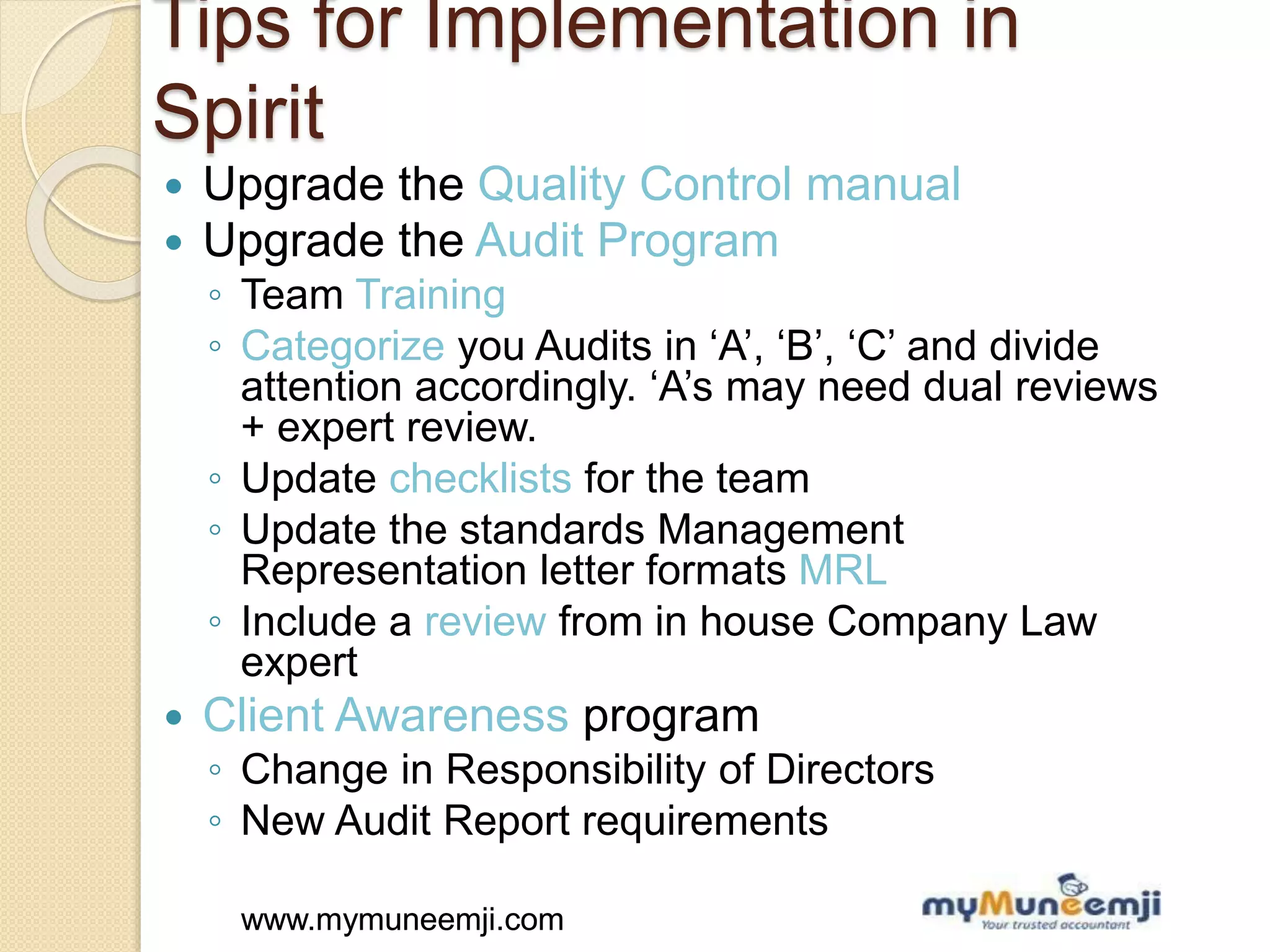

Applicability of CARO, 2015

Includes:

Foreign Companies under Section 2(42)

Excludes:

Banking and Insurance Companies

One Person Company [OPC u/s 2(62)]

Companies with Charitable Objects u/s 8

Private Companies (AND condition)

◦ Capital + Reserve < Rs. 50 Lakhs

◦ Outstanding Loans < Rs. 25 Lakhs

◦ Turnover < Rs. 5 Crores (Any given point in

time)

Small Companies u/s 2(85)](https://image.slidesharecdn.com/seminaronauditreportmmj-150608103457-lva1-app6892/75/Highlights-on-changes-in-Audit-formalities-under-New-Companies-Act-2013-11-2048.jpg)

The document outlines significant changes in audit formalities under the Companies Act 2013, including auditor responsibilities, the appointment process, and key additions to audit reports. It emphasizes the transition to a rules-based model and the increased accountability of directors while providing guidelines for compliance, especially concerning the audit process and reporting of frauds. Additionally, it discusses the applicability and modifications to the Companies Auditor's Report Order (CARO) 2015, urging auditors to enhance their quality control and training.

![KWL Chart Graphic Organizer in Green and Yellow Minimalist Style[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/kwlchartgraphicorganizeringreenandyellowminimaliststyle1-241211092106-322ddd2c-thumbnail.jpg?width=640&height=640&fit=bounds)