New base energy news issue 953 dated 22 november 2016

Greetings, Attached FYI (NewBase 22 November 2016 ) , from Hawk Energy Services Dubai . Daily energy news covering the MENA area and related worldwide energy news. In today’s issue you will find news about:- • Fitch Affirms Dolphin Energy Bonds at 'A+'; Outlook Stable • Saudi Arabia to establish national water and energy efficiency program • Saudi Aramco Promise of $1bn fees for IPO in London bankers • Sweden's Lundin Petroleum finds more oil in Norwegian Arctic • Azerbaijan: Total and SOCAR sign agreement to develop Absheron • Oil prices rise in anticipation of planned OPEC-led production cut • Oil Extends Gains as OPEC Shows Signs of Progress on Output Deal • Tesla Shock Means Global Gasoline Demand Has All But Peaked we would appreciate your actions to send to all interested parties that you may wish. Also note that if you or your organization wish to include your own article or advert in our circulations, please send it to :- khdmohd@hotmail.com or khdmohd@hawkenergy.net Best Regards. Khaled Al Awadi Energy Consultant & NewBase Chairman - Senior Chief Editor MS & BS Mechanical Engineering (HON), USA Emarat member since 1990 ASME member since 1995 Hawk Energy since 2010

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (15)

Similar to New base energy news issue 953 dated 22 november 2016

Similar to New base energy news issue 953 dated 22 november 2016 (20)

More from Khaled Al Awadi

More from Khaled Al Awadi (20)

Recently uploaded

Recently uploaded (20)

New base energy news issue 953 dated 22 november 2016

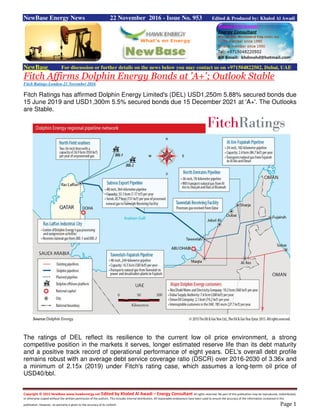

- 1. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 1 NewBase Energy News 22 November 2016 - Issue No. 953 Edited & Produced by: Khaled Al Awadi NewBase For discussion or further details on the news below you may contact us on +971504822502, Dubai, UAE Fitch Affirms Dolphin Energy Bonds at 'A+'; Outlook Stable Fitch Ratings-London-21 November 2016 Fitch Ratings has affirmed Dolphin Energy Limited's (DEL) USD1,250m 5.88% secured bonds due 15 June 2019 and USD1,300m 5.5% secured bonds due 15 December 2021 at 'A+'. The Outlooks are Stable. The ratings of DEL reflect its resilience to the current low oil price environment, a strong competitive position in the markets it serves, longer estimated reserve life than its debt maturity and a positive track record of operational performance of eight years. DEL's overall debt profile remains robust with an average debt service coverage ratio (DSCR) over 2016-2030 of 3.36x and a minimum of 2.15x (2019) under Fitch's rating case, which assumes a long-term oil price of USD40/bbl.

- 2. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 2 DEL operates a large oil and gas project extracting gas from offshore fields in Qatar. KEY RATING DRIVERS Revenue Risk - Stronger We assess DEL as Stronger in respect of revenue risk despite partial exposure to commodity oil and gas prices. The project's long-term fixed-price gas supply contracts account for over 50% of DEL's gross margin and substantially mitigate DEL's exposure to commodity prices. Within the upstream business, DEL can withstand significant oil price declines and is able to break-even at an oil price of USD1.8bbl under Fitch's base case. DEL should be able to withstand the current low oil price environment due to its high financial flexibility. Fitch's rating case factors in stressed oil price levels (see 'Oil and Gas Price Assumptions' dated July 2016), which have been further adjusted down to a long-term USD40/bbl, from USD55/bbl previously. DEL's exposure to market gas prices under short-term interruptible gas sales is sizeable in revenue terms (20% in 2015, 12% in 1H16 of gas revenues excluding third-party gas sales). Our projection of USD6/Mmbtu for interruptible gas sales is still appropriate despite a substantial reduction in global gas prices in 2016. Our unchanged assumption is supported by historical interruptible gas prices achieved by DEL, including in 1H16, and the market advisor's projection of the cost of alternative supply (importing liquefied natural gas to UAE or diesel). The exposure to unrated long-term gas offtakers Abu Dhabi Water and Electricity Company (ADWEC), Dubai Supply Authority (DUSUP) and Oman Oil Company is mitigated by DEL's competitive gas prices under long-term contracts. These are significantly lower than the cost of alternative supply or prices negotiated under short-term interruptible agreements, which approximate market spot prices. Supply Risk - Stronger DEL's exposure to supply risk is assessed as Stronger. The reserve consultant NSAI provided an updated reserve study in 2015 showing that 1P developed reserves (the level of production which is likely to be reached or exceeded with a 90% probability) are sufficient to cover base case requirements until 2026. DEL is progressing with the implementation of the Reservoir Management and Optimisation Project (RMOP) aimed at achieving homogenous reservoir depletion, particularly of liquids, and extending the production plateau. NSAI estimated that RMOP will extend DEL's production plateau to April 2034 in case of partial implementation and to October 2039 in case of full implementation. The Stronger assessment of supply risk is supported by an estimated reserve life extending beyond debt maturity and NSAI's view that projects such as RMOP are common in the oil and gas industry. Operating Risk - Midrange Fitch assesses DEL's operational risk as Midrange. The project's facilities are relatively complex but have been performing well over eight years. On-going technical issues are resolved during scheduled maintenance shutdowns with no significant impact on production and availability, and

- 3. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 3 DEL has consistently met the maximum production targets under the Development and Production Sharing Agreement (DPSA), supporting the positive operational track record of the asset. Debt Structure - Midrange The midrange assessment reflects the complexity of the project's structure (upstream-midstream split, dual waterfall etc.) together with the project's fairly strong structural features. Refinancing risk related to the 2021 bullet bond and associated shareholder debt is addressed by a sinking fund and the mechanism should trap 100% of the bullet requirement, even under Fitch rating case. Despite the sinking fund feature, the financial projections assume that the 2021 bond will be re- financed with amortising debt maturing in 2030. With the addition of USD863m of bank debt in late 2015, the maturity of the debt extends to 2030 and the tail remaining until the end of DPSA is 1.5 years. The proportion of debt exposed to floating unhedged interest rates is about 26%, and Fitch assumes a stressed LIBOR rate in its projections. Financial Profile Under the revised projections Fitch's base case average DSCR over 2016-2030 is 4.02x with a minimum of 2.44x. Under Fitch rating case, which incorporates long-term stress case oil price of USD40/bbl, average DSCR is 3.36x with a minimum of 2.15x (2019). Debt metrics are 20-30bps lower than last year, due to our revised oil price projections. However in our view, DEL's financial profile remains strong, which is supported by low forecast gross debt/cash flows available for debt service of 3x at end-2016. DEL's capex, such as the RMOP and Industrial Water Management Project (IWMP), is not subtracted from cash flows available for debt service when calculating debt metrics in line with the project's documentation, as debt service ranks senior to discretionary capex in the cash waterfall. However, even if this capex was entirely funded from operational cash flows as it occurs, it would not jeopardise debt service, demonstrating the strength of the cash flow profile. In addition, capex related to upstream operations is recoverable through upstream revenues over five years as per the provisions of the DPSA. Peers Peers in this rating category and with similar revenue structure are limited. RasGas is the most comparable peer transaction, with an underlying rating at the same level at 'A+'. RasGas derives its revenues from the sale of LNG and by-products and its revenues are fully exposed to commodity prices versus DEL whose revenue stream is partially contracted. RasGas's revenue risk is assessed as Midrange. RasGas's debt metrics, however, are stronger under the same oil price assumptions, with the average DSCR over the remaining debt life of 5.9x. RATING SENSITIVITIES Fitch is unlikely to upgrade DEL's ratings given the single-site nature of the project's processing facilities in Ras Laffan and the single subsea export pipeline. DEL's ratings would come under downward pressure should the project experience major operating problems, if there is a severe reduction in the length of the production plateau, a prolonged blockade of the shipping route via Strait of Hormuz or a material deterioration in the credit quality of Abu Dhabi, the main market for DEL's natural gas, and Qatar. Fitch currently rates Qatar and Abu Dhabi 'AA'.

- 4. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 4 The ratings could also come under pressure in case of deterioration of average DSCR to 2030 under Fitch's rating case to levels close to or below 2.4x PERFOMANCE UPDATE DEL's operational performance in 2015 and 2016 was stable, with gas production at the maximum allowable annual level of 730 bcf under DPSA. Condensates' production in 2015 was at the same level as in 2014 at around 33million barrels. DEL is affected by lower oil prices with average achieved condensates' price of USD52/bbl in 2015 and USD40/bbl in 1H16. However, operating costs have been under control and financial performance is generally in line with expectations. Last year's reported annual DSCR was 3.63x and the latest June 2016 reported annual DSCR was 2.81x (excluding the impact of third party gas sales and capex) against previous Fitch base case DSCR of 2.91x for the same period. DEL is on track with the implementation of RMOP and IWMP. The first phase of the drilling works under RMOP is expected to be completed in Q117. SUMMARY OF CREDIT DEL operates a large oil and gas project extracting gas from offshore fields in Qatar, processes gas at Ras Laffan in Qatar and then exports around 2 billion cubic feet a day of clean gas via a 364 km subsea pipeline to Abu Dhabi for onward sale in the UAE and Oman, mostly under long- term contracts. The project also produces a significant amount of condensate and liquefied petroleum gas which are by-products of gas processing.

- 5. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 5 Saudi Arabia to establish national water and energy efficiency program Reuters + NewBase Saudi Arabia will establish a national program to optimise water and energy consumption, it announced in a cabinet statement on Monday, further moves in areas where the government is seeking to cut back huge subsidies. The new program will review policy incentives currently in place for the energy and water sectors, taking into account both economic productivity needs and inequality within society, the statement said. It did not elaborate on where the new program would reside within the government or whether its creation might augur further cuts to the kingdom's extensive water and power subsidies. The announcement comes amid major restructuring of the kingdom's energy and water sectors, intended to support sweeping economic reform plans to wean the world's largest crude exporter off its dependence on oil. As part of the reform drive, Saudi Arabia aims to reduce electricity and water subsidies by 200 billion riyals ($53 billion) and reduce non-oil subsidies by 20 percent by 2020. It introduced its first subsidy cuts for power and water in December, then sacked the minister responsible following a public outcry over how the new water tariffs were applied to average Saudis. Deputy Crown Prince Mohammed bin Salman, who is responsible for the economic reforms, was quoted as saying the water price increases had not been implemented as planned. In May, King Salman restructured the ministries responsible for handling water and energy policies. Through royal decrees, he broke up the old Water and Electricity Ministry and handed responsibility for electricity over to a new Energy, Industry and Natural Resources Ministry headed by Khaled al-Falih, chairman of state oil company Aramco. The water portfolio was incorporated into a new Environment, Water and Agriculture Ministry.

- 6. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 6 Saudi Reserves According to the Oil & Gas Journal (OGJ), Saudi Arabia had approximately 266 billion barrels of proved oil reserves3 (in addition to 2.5 billion barrels in the Saudi-Kuwaiti shared Neutral Zone, half of the total reserves in the Neutral Zone) as of January 1, 2014, amounting to 16% of proved world oil reserves. Although Saudi Arabia has about 100 major oil and gas fields, more than half of its oil reserves are contained in eight fields in the northeast portion of the country.4 The giant Ghawar field is the world's largest oil field in terms of production and total remaining reserves. The Ghawar field has estimated remaining proved oil reserves of 75 billion barrels,5 more than all but seven other countries. Saudi Aramco Promise of $1bn fees for IPO in London bankers The National - Ivan Fallon Just how much oil does Saudi Arabia have? Oil analysts and global energy strategists have been asking that question for generations, and now it seems we are about to find out. Ever since the formerly American-controlled Saudi Aramco was fully nationalised in the 1980s, Saudi Arabian officials have consistently been saying it has about 260 billion barrels of proven reserves. But no one has ever been able to verify that figure, and in any case it is most unlikely that, as old oilfields have run down and new ones developed, the figure would remain the same for 30 years. But now, in what is being billed – with some justification – as the sale of the century, Saudi Arabia is expected to reveal all as it moves towards a stock exchange flotation, or IPO, of its state oil company. The valuations are astronomical: a figure of US$2 trillion is being talked about in the City of London. That is three times the size of Apple or Google, the two most valuable companies, measured by market capitalisation, the world has ever known. It is also 20 times the size of Shell, Britain’s biggest oil company, and equivalent to 50 per cent of all the companies quoted in London. A listing in London, even a secondary one, would be a major coup for the post-Brexit City. Khalid Al Falih, Saudi Arabia’s energy minister, says he is fully prepared to publish up-to-date estimates of the oil reserves. "This is going to be the most transparent national oil company listing of all time," he told the Financial Times. "Everything that Saudi Aramco has, that will be shared, that will be verified by independent third parties." That would include, he added, financial statements, "reserves ... costs [and] profitability indicators". The stake sale is expected to amount to only 5 per cent of Aramco’s total shares, but even that would amount to US$100 billion, which is four times what China’s Alibaba raised two years ago.

- 7. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 7 It is a long time since there has been such excitement over a new issue in London. There are reports in London of top bankers besieging the Saudi embassy seeking visas as they prepare to fly to Riyadh this week to pitch for the role of advising King Salman and his 31-year-old son, Prince Mohammed bin Salman. The last time the City enjoyed such a bonanza was Glencore, five years ago, where 23 banks were involved in the listing and shared fees of £165 million (Dh746.5m) between them. On the same basis, an Aramco listing would generate fees of $1bn. The kingdom’s reserves are not being sold off – the state will retain its sovereign right over their management. But the verified quantity of Saudi Arabia’s proven oil reserves is of enormous importance. Aramco produces 10 per cent of the world’s oil supply and for the past 30 years world oil prices have been based partly on that 260 billion barrel figure. For decades, Saudi’s role had been as a swing producer, taking its output up or down to balance the oil price. Then in 2014, it surprised global markets by cutting its production, pumping out oil to protect its market share, and forcing the American shale oil industry to shut up shop. The result was that after four years at more than $100 per barrel, the price of oil dropped below $30 earlier this year, before staging a recovery to about $50. Now the country is surprising the world again, this time by lifting the veil. But without disclosure there could be no IPO. Aramco’s listing is part of Saudi Arabia’s grand plan to modernise its economy, the largest in the Gulf, and reduce its dependence on oil. It comes at a time of growing concern among Opec countries at the build-up of unsold oil, particularly off the coast of the UK, which will keep prices down for some time, and increase pressure on Opec to cut production. A report last week from Wood Mackenzie, the energy consultancy, forecast that growth in demand for oil will slow to an annual average of 0.5 per cent in the next 20 years, while renewable energy output could expand almost five-fold. Paul McConnell, the director of global trends for Wood Mac, said that, in the past month alone, 10 oil and gas companies have committed jointly $1bn on clean energy technology – initially focused on carbon capture and storage systems. Just about every oil company in the world is stepping up its investment and Aramco is doing the same. Mr Al Falih, who is also chairman of Aramco, says he hopes that as much as 30 per cent of the kingdom’s electricity will eventually come from a mix of renewables and nuclear power. The company is in the process of building one large wind turbine in the kingdom as a "demonstration", with more to follow. None of those more sober thoughts will bother all those bankers flying into Riyadh this week to take part in a two-day beauty parade. The long-term future of Aramco, oil or Saudi Arabia is secondary. They just want the fees.

- 8. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 8 Sweden's Lundin Petroleum finds more oil in Norwegian Arctic Reuters + NewBase Lundin Petroleum has found additional oil and gas in the Norwegian Arctic, the Swedish company and the Norwegian Petroleum Directorate said on Tuesday, lifting the company's shares. The find is located some 60 km (37 miles) from Lundin's Alta find, which the company estimates could contain up to 400 million barrels of oil equivalent (BOE), and 20 km from the Johan Castberg discovery which contains up to 600 million barrels of oil. "The total gross resource estimate for the Neiden discovery is between 25 and 60 million (BOE)," Lundin Petroleum said in a statement. Shares in Lundin were up 4.46 percent at 0709 GMT, making it the best performing stock in the European oil and gas index. "Although a discovery is positive, the preliminary volumes estimate ... was significantly below the pre-drill estimate of 204 million barrels," Swedbank analyst Teodor Sveen-Nilsen, who holds a Reduce recommendation on the stock, wrote in a note to clients. Oil companies such as Statoil and Lundin have great hopes that the Norwegian Arctic, which is much less explored than the North Sea, could contain significant new oil and gas resources. Others are less enthusiastic, however, with Royal Dutch Shell, Total and Eni not participating in the latest oil licensing round organized by Norway, which focused on the Arctic. The only find in production in the Arctic Barents Sea is Eni's Goliat, but others are in development, such as Statoil's Johan Castberg field. Lundin operates the well at the Neiden discovery and has a 40 percent stake. Its partners are Japan's Idemitsu and DEA, the oil firm controlled by Russian billionaire Mikhail Fridman, each hold 30 percent stakes. Lundin will next drill a prospect called Filicudi, also located in the Barents Sea, which the firm estimates could contain up to 258 million BOE.

- 9. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 9 Azerbaijan: Total and SOCAR sign agreement to develop Absheron Source : Total Total and SOCAR, the national oil company of Azerbaijan, have signed an agreement establishing the contractual and commercial terms for a first phase of production of the Absheron gas and condensate field, located in the Caspian Sea and discovered by Total in 2011. 'I’m delighted with this agreement, which we sign on the occasion of the 20th anniversary of Total’s presence in Azerbaijan, and which represents an important step to monetize the Absheron discovery made by Total in 2011' said Patrick Pouyanné, Chairman and CEO of Total. 'This agreement was made possible by the close cooperation between Total and SOCAR, which has allowed us to design a cost-competitive development scheme by tying the field to existing infrastructure in order to deliver gas at a competitive price'. The development involves the drilling of one well at a water depth of 450 meters. Production from this high pressure field will be around 35 thousand barrels of oil equivalent per day, including a significant portion of condensate. The produced gas will supply Azerbaijan’s domestic market. This first phase of production will also enable a dynamic appraisal of the field for future phases. Total is the operator of Absheron with a 40% interest alongside SOCAR(40%) and ENGIE (20%). Total has been present in Azerbaijan since 1996. Total also holds a 5% interest in BTC Co, owner of the BTC oil pipeline (Bakou-Tbilissi-Ceyhan), which connects Baku and the Mediterranean Sea.

- 10. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 10 NewBase 22 November 2016 Khaled Al Awadi NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE Oil prices rise in anticipation of planned OPEC-led production cut Reuters - By Henning Gloystein Oil prices rose to their highest level since October on Tuesday as the market priced in a potential output cut led by producer cartel OPEC, although analysts warned that a failure to agree a cut could lead to a ballooning supply overhang by early 2017. International Brent crude oil futures rose as high as $49.43 per barrel early on Tuesday, their highest since Oct. 31, and they were trading at $49.33 per barrel at 0110 GMT, up 43 cents, or 0.9 percent, from their last settlement. U.S. West Texas Intermediate (WTI) crude futures were up 44 cents, or 0.9 percent, at $48.68 a barrel. The Organization of the Petroleum Exporting Countries (OPEC) is trying by Nov. 30 to bring its 14 member states and non-OPEC producer Russia to agree on a coordinated production cut to prop up the market by bringing production into line with consumption. "With investors becoming more optimistic about OPEC reaching an agreement on production cuts, oil prices should continue to edge higher in trading today," ANZ bank said on Tuesday. Goldman Sachs said in a note to clients that the chances of an OPEC cut had increased as producers needed to react to eroding supply and demand fundamentals, which the bank said "have weakened sharply since OPEC announced a tentative agreement to cut production." Should OPEC and other producers, especially Russia, fail to agree a cutback, Goldman said it expected an oil supply surplus of 0.7 million barrels per day (bpd) for the first quarter of 2017. Oil price special coverage

- 11. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 11 Oil Extends Gains as OPEC Shows Signs of Progress on Output Deal Bloomberg - Perry Williams Oil surged for a third day on signs OPEC members have made progress toward finalizing a deal to cut output. January futures rose as much as 1.5 percent in New York after the December contract expired 3.9 percent higher Monday. Talks on assigning quotas to individual countries went well, Libyan OPEC Governor Mohamed Oun said after preliminary meetings at the group’s headquarters in Vienna. Goldman Sachs Group Inc. said it’s now “tactically bullish” on the likelihood of an agreement. U.S. government data Wednesday is forecast to show the smallest expansion of crude stockpiles since January, according to a Bloomberg survey. Oil has rebounded from an eight-week low on Nov. 14 as members of the Organization of Petroleum Exporting Countries make renewed diplomatic efforts before their Nov. 30 meeting to finalize the supply deal they agreed to informally in September. The group’s plan to trim output for the first time in eight years is complicated by Iran’s commitment to boost production and Iraq’s request for an exemption to help fund its war with Islamic militants. “An OPEC deal would push oil through $50,” said Evan Lucas, a market strategist at IG Ltd. in Melbourne. “If it’s a verbal agreement with all non-binding overlays, the market will get positive very quickly. It could then fall back to a band of $45 to $46 a barrel.” West Texas Intermediate for January delivery rose as much as 74 cents to $48.98 a barrel on the New York Mercantile Exchange and was at $48.42 at 8:11 a.m. in London. The December contract expired Monday after rising $1.80 to $47.49, the highest close for front-month prices since Oct. 28. Total volume traded was about 51 percent above the 100-day average. More Confident

- 12. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 12 Brent for January settlement climbed as much as 73 cents, or 1.5 percent, to $49.63 a barrel on the London-based ICE Futures Europe exchange. The contract added $2.04, or 4.4 percent, to $48.90 a barrel on Monday, the highest close since Oct. 28. The global benchmark traded at a 68 cent premium to WTI. The likelihood of a deal also pushed Goldman to be bullish on oil prices in the short term, boosting the bank’s forecast of WTI price to $55 in the first two quarters of next year, versus prior estimates of $45 and $50, respectively, according to analysts including Damien Courvalin in a research note Monday. Oil-market news: U.S. inventories probably rose by 250,000 barrels last week, according to the survey before an Energy Information Administration report. That will be the smallest gain since a 234,000 barrel increase through Jan. 8. The chairman of Commodity Futures Trading Commission is trying to push ahead with controversial rules that clamp down on traders’ ability to speculate in oil and other commodities before President-elect Donald Trump takes office, according to people familiar with the matter.

- 13. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 13 NewBase Special Coverage News Agencies News Release 22 November 2016via Getty Images Tesla Shock Means Global Gasoline Demand Has All But Peaked Bloomberg - Javier Blas JavierBlas2 After fueling the 20th century automobile culture that reshaped cities and defined modern life, gasoline has had its day. The International Energy Agency forecasts that global gasoline consumption has all but peaked as more efficient cars and the advent of electric vehicles from new players such as Tesla Motors Inc. halt demand growth in the next 25 years. That shift will have profound consequences for the oil- refining industry because gasoline accounts for one in four barrels consumed worldwide. “Electric cars are happening,” IEA Executive Director Fatih Birol said in an interview in London, adding that their number will rise from little more than 1 million last year to more than 150 million by 2040. The cresting of gasoline demand shows how rapidly the oil landscape is changing, casting a shadow over an industry that commonly forecasts decades of growth ahead. Royal Dutch Shell Plc, the world’s second-biggest energy company by market value, shocked rivals this month when a senior executive said overall oil demand could peak in as little as five years. The IEA doesn’t share Shell’s pessimism. While the agency anticipates a gasoline peak, it still forecasts overall oil demand growing for several decades because of higher consumption of diesel, fuel oil and jet fuel by the shipping, trucking, aviation and petrochemical industries.

- 14. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 14 For Philip Verleger, president of the consultant PKVerleger LLC in Colorado and a veteran oil- market analyst, the IEA’s outlook is one of the more optimistic outcomes for the global industry. “Refiners across the globe can only hope that this forecast turns out to be right -- because all the indications are today that consumption is going to begin dropping not in 2030, but probably in 2020,” said Verleger. “It’s the best news a dying patient can hope to get.” The projections are part of the analysis the Paris-based IEA did for its “World Energy Outlook 2016” flagship report. The agency forecast that gasoline demand will drop to 22.8 million barrels a day by 2020 from 23 million barrels a day last year. By 2030, consumption will rebound slightly, reaching a peak of 23.1 million barrels a day, before falling again toward 2040. The forecast is more pessimistic than the one released a year ago, when the IEA saw robust demand growth from now until 2030. Gasoline has been the world’s choice to power automobiles. From the 1950s onward, when Henry Ford’s dream that every middle-class American could own a car became reality, gas stations sprung up next to drive-through restaurants and strip malls and transformed the landscape of America and economies across the globe. Now, however, car companies -- most obviously Tesla, but also incumbents such as General Motors Co., BMW AG and Nissan Motor Co. -- are putting their money, and reputations, behind electric vehicles. With technology improving -- especially for batteries -- prices are falling. Tax breaks, particularly in China, are helping sales. Global gasoline demand grew by nearly 20 percent between 1990 and 2015 despite competition from diesel in Europe, where the fuel benefited from tax breaks. In the next 25 years, gasoline consumption will drop 0.2 percent, according to the new IEA calculations. While the number of

- 15. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 15 passenger vehicles will double to 2 billion by 2040, “the amount of oil we use for cars will be lower than today,” Birol said. The biggest victim is likely to be refiners, which have spent billions of dollars over the last two decades to maximize gasoline output at the expense of other fuels. Birol said the changes in fuel- demand growth over the next 25 years will have “major implications” for the industry, which probably will have to re-tool their plants. Diesel Ascendant “Demand for gasoline will be much more affected than heavier fuels -- the refineries’ configuration will be affected," he said. As gasoline demand sputters in advanced economies, middle distillates, fuels used to power trucks and jets, will continue to see growth in the next decade as economies expand. And new international rules will require that the heavy, dirty fuels currently used for marine transit be replaced with lower-sulfur diesel in 2020. Refiners would be wise to target distillates such as diesel in lieu of gasoline as they grapple with fading consumption, said Michael Wojciechowski, vice president of Americas oil and refining markets research at Wood Mackenzie Ltd. in Houston. "Diesel seems to be almost like a utility fuel going forward,” Wojciechowski said. “It’s got its ability to meet a lot of strategic objectives for refiners.”

- 16. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 16 NewBase For discussion or further details on the news below you may contact us on +971504822502, Dubai, UAE Your partner in Energy Services NewBase energy news is produced daily (Sunday to Thursday) and sponsored by Hawk Energy Service – Dubai, UAE. For additional free subscription emails please contact Hawk Energy Khaled Malallah Al Awadi, Energy Consultant MS & BS Mechanical Engineering (HON), USA Emarat member since 1990 ASME member since 1995 Hawk Energy member 2010 Mobile: +97150-4822502 khdmohd@hawkenergy.net khdmohd@hotmail.com Khaled Al Awadi is a UAE National with a total of 26 years of experience in the Oil & Gas sector. Currently working as Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external voluntary Energy consultation for the GCC area via Hawk Energy Service as a UAE operations base , Most of the experience were spent as the Gas Operations Manager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stations . Through the years, he has developed great experiences in the designing & constructing of gas pipelines, gas metering & regulating stations and in the engineering of supply routes. Many years were spent drafting, & compiling gas transportation, operation & maintenance agreements along with many MOUs for the local authorities. He has become a reference for many of the Oil & Gas Conferences held in the UAE and Energy program broadcasted internationally, via GCC leading satellite Channels. NewBase : For discussion or further details on the news above you may contact us on +971504822502 , Dubai , UAE NewBase November 2016 K. Al Awadi

- 17. Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 17