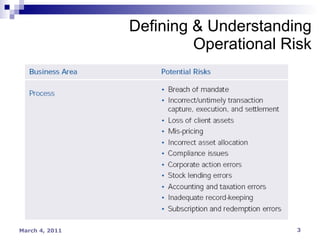

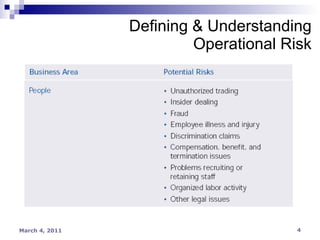

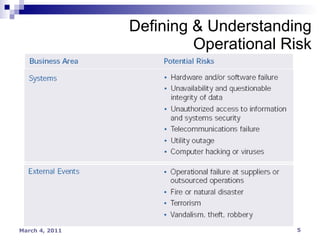

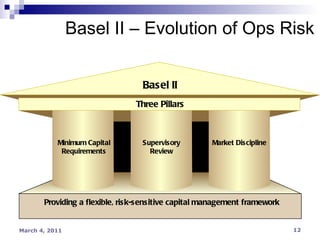

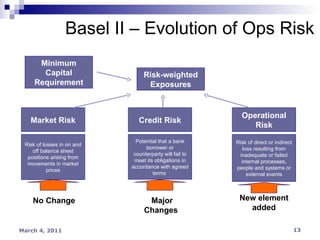

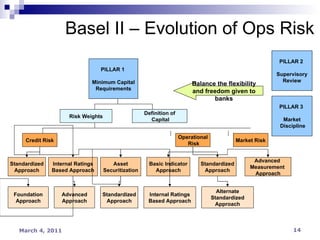

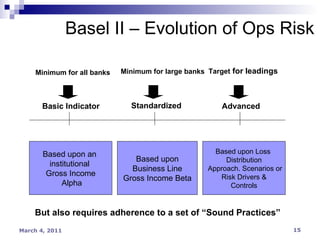

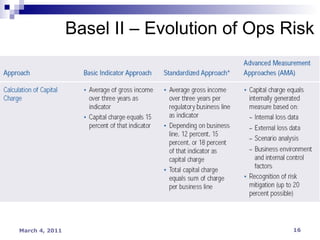

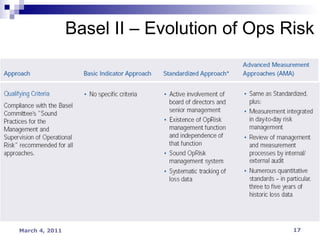

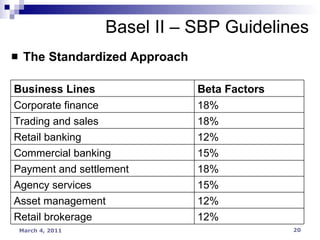

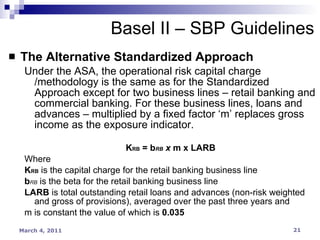

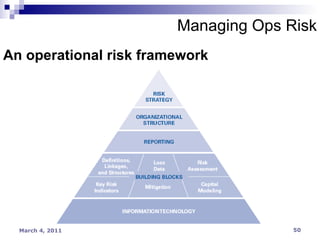

The document discusses operational risk and Basel II regulations. It defines operational risk as losses from internal failures or external events. It outlines the three pillars of Basel II which establish minimum capital requirements, supervisory review, and market discipline. It describes the different approaches for calculating operational risk capital charges, including the Basic Indicator Approach, Standardized Approach, and Advanced Measurement Approach.