Recommended

Recommended

More Related Content

Similar to 1Unsatisfactory 0-710.002Less Than Satisfactory 72-75.docx

Similar to 1Unsatisfactory 0-710.002Less Than Satisfactory 72-75.docx (13)

More from felicidaddinwoodie

More from felicidaddinwoodie (20)

Recently uploaded

Recently uploaded (20)

1Unsatisfactory 0-710.002Less Than Satisfactory 72-75.docx

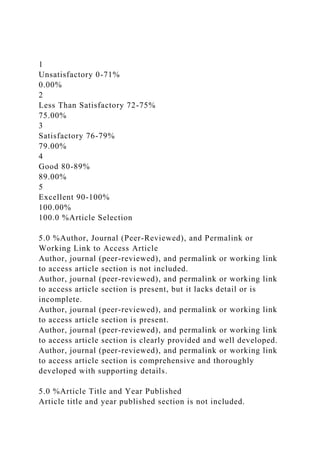

- 1. 1 Unsatisfactory 0-71% 0.00% 2 Less Than Satisfactory 72-75% 75.00% 3 Satisfactory 76-79% 79.00% 4 Good 80-89% 89.00% 5 Excellent 90-100% 100.00% 100.0 %Article Selection 5.0 %Author, Journal (Peer-Reviewed), and Permalink or Working Link to Access Article Author, journal (peer-reviewed), and permalink or working link to access article section is not included. Author, journal (peer-reviewed), and permalink or working link to access article section is present, but it lacks detail or is incomplete. Author, journal (peer-reviewed), and permalink or working link to access article section is present. Author, journal (peer-reviewed), and permalink or working link to access article section is clearly provided and well developed. Author, journal (peer-reviewed), and permalink or working link to access article section is comprehensive and thoroughly developed with supporting details. 5.0 %Article Title and Year Published Article title and year published section is not included.

- 2. Article title and year published section is present, but it lacks detail or is incomplete. Article title and year published section is present. Article title and year published section is clearly provided and well developed. Article title and year published section is comprehensive and thoroughly developed with supporting details. 10.0 %Research Questions (Qualitative) or Hypothesis (Quantitative), and Purposes or Aim of Study Research questions (qualitative) or hypothesis (quantitative), and purposes or aim of study section is not included. Research questions (qualitative) or hypothesis (quantitative), and purposes or aim of study section is present, but it lacks detail or is incomplete. Research questions (qualitative) or hypothesis (quantitative), and purposes or aim of study section is present. Research questions (qualitative) or hypothesis (quantitative), and purposes or aim of study section is clearly provided and well developed. Research questions (qualitative) or hypothesis (quantitative), and purposes or aim of study section is comprehensive and thoroughly developed with supporting details. 5.0 %Design (Type of Quantitative, or Type of Qualitative) Design (type of quantitative, or type of qualitative) section is not included. Design (type of quantitative, or type of qualitative) section is present, but it lacks detail or is incomplete. Design (type of quantitative, or type of qualitative) section is present. Design (type of quantitative, or type of qualitative) section is clearly provided and well developed. Design (type of quantitative, or type of qualitative) section is comprehensive and thoroughly developed with supporting details.

- 3. 5.0 %Setting or Sample Setting or sample section is not included. Setting or sample section is present, but it lacks detail or is incomplete. Setting or sample section is present. Setting or sample section is clearly provided and well developed. Setting or sample section is comprehensive and thoroughly developed with supporting details. 5.0 %Methods: Intervention or Instruments Methods: Intervention or instruments section is not included. Methods: Intervention or instruments section is present, but it lacks detail or is incomplete. Methods: Intervention or instruments section is present. Methods: Intervention or instruments section is clearly provided and well developed. Methods: Intervention or instruments section is comprehensive and thoroughly developed with supporting details. 10.0 %Analysis Analysis section is not included. Analysis section is present, but it lacks detail or is incomplete. Analysis section is present. Analysis section is clearly provided and well developed. Analysis section is comprehensive and thoroughly developed with supporting details. 10.0 %Key Findings Key findings section is not included. Key findings section is present, but it lacks detail or is incomplete. Key findings section is present. Key findings section is clearly provided and well developed. Key findings section is comprehensive and thoroughly

- 4. developed with supporting details. 10.0 %Recommendations Recommendations section is not included. Recommendations section is present, but it lacks detail or is incomplete. Recommendations section is present. Recommendations section is clearly provided and well developed. Recommendations section is comprehensive and thoroughly developed with supporting details. 10.0 %Explanation of How the Article Supports EBP or Capstone Explanation of how the article supports EBP or capstone section is not included. Explanation of how the article supports EBP or capstone section is present, but it lacks detail or is incomplete. Explanation of how the article supports EBP or capstone section is present. Explanation of how the article supports EBP or capstone section is clearly provided and well developed. Explanation of how the article supports EBP or capstone section is comprehensive and thoroughly developed with supporting details. 10.0 %Presentation The piece is not neat or organized, and it does not include all required elements. The work is not neat and includes minor flaws or omissions of required elements. The overall appearance is general, and major elements are missing. The overall appearance is generally neat, with a few minor flaws or missing elements. The work is well presented and includes all required elements.

- 5. The overall appearance is neat and professional. 10.0 %Mechanics of Writing (includes spelling, punctuation, grammar, and language use) Surface errors are pervasive enough that they impede communication of meaning. Inappropriate word choice or sentence construction is employed. Frequent and repetitive mechanical errors distract the reader. Inconsistencies in language choice (register) or word choice are present. Sentence structure is correct but not varied. Some mechanical errors or typos are present, but they are not overly distracting to the reader. Correct and varied sentence structure and audience-appropriate language are employed. Prose is largely free of mechanical errors, although a few may be present. The writer uses a variety of effective sentence structures and figures of speech. The writer is clearly in command of standard, written, academic English. 5.0 %Documentation of Sources (citations, footnotes, references, bibliography, etc., as appropriate to assignment and style) Sources are not documented. Documentation of sources is inconsistent or incorrect, as appropriate to assignment and style, with numerous formatting errors. Sources are documented, as appropriate to assignment and style, although some formatting errors may be present. Sources are documented, as appropriate to assignment and style, and format is mostly correct. Sources are completely and correctly documented, as appropriate to assignment and style, and format is free of error. 100 %Total Weightage

- 6. InstructionsSouthern New Hampshire UniversityCollege of Continuing Education (COCE)ACC 202 - Managerial AccountingMILESTONE 1 (Due in Module 2)MILESTONE 2 (Due in Module 4)MILESTONE 3 (Due in Module 5)1.1.1.NameChoose a price range and calculate:Create a Cost of Services Schedule.LocationGroomingVisionDay CareMissionBoarding2.2.2.Identify the following:Calculate the break-even units:Create an Income Statement.Direct MaterialsGroomingRevenue will be provided at the end of week 4.Diret LaborDay CareManufacturing OverheadBoardingPeriod CostsCalculate the break-even for target profits:3.Grooming3.Day CareCalculate the Variable and Fixed Costs for:BoardingCalculate for the Grooming line:GroomingDirect Labor Time VarianceDay CareDirect Labor Rate VarianceBoardingDirect Materials Efficiency VarianceDirect Materials Price Variance ACC202 - MANAGERIAL ACCOUNTING Company Profile/xl/drawings/drawing1.xml#CompanyProfile Variable and Fixed Costs/xl/drawings/drawing1.xml#VariableFixedCosts Cost Classification /xl/drawings/drawing1.xml#CostClassification Contribution Margin/xl/drawings/drawing1.xml#ContributionMargin Break-Even Analysis/xl/drawings/drawing1.xml#BreakevenAnalysis COS Schedule/xl/drawings/drawing1.xml#COGMSchedule Income Statement/xl/drawings/drawing1.xml#'Income%20Statement'!A1 Variances/xl/drawings/drawing1.xml#Variances Instructions Milestone 1/xl/drawings/drawing1.xml#InstructionsMilestone1 Instructions Milestone

- 7. 2/xl/drawings/drawing1.xml#'Instructions%20- %20Milestone%202'!InstructionsMilestone2 Instructions Milestone 3/xl/drawings/drawing1.xml#'Instructions%20- %20Milestone%203'!InstructionsMilestone3 Instructions - Milestone 1Southern New Hampshire UniversityCollege of Continuing Education (COCE)ACC 202 - Managerial AccountingINSTRUCTIONS FOR MILESTONE 1 (Due Week 2)IMPORTANT NOTE:Make sure to completely review the rubric for Milestone 1.Use the data from this milestone and begin working on your final presentation due in Milestone 4 (Week 7).ITEMS TO COMPLETE FOR THIS MILESTONE (Blue Tabs):GENERALYou plan to open a pet services business that will offer dog grooming, day care, and boarding.COMPANY PROFILE TABDetermine a company name. Be creative (e.g., "Inspiring Dog Care").Pick a location (e.g., "Chicago").Define your company's vision and mission for how your business will add value to the community.COST CLASSIFICATIONAccurately classify all of your costs (direct material, direct labor, manufacturing overhead, period costs).Fixed and variable cost designation is provided.VARIABLE AND FIXED COSTSDetermine your per- unit cost per dog for grooming, day care, and boarding.OPERATIONAL AND COST INFORMATION:For simplicity, base all calculations using 30 days in each month.OPERATIONAL DATAGrooming:The groomer can groom 5 dogs a day, 5 days a week.Each grooming takes 1.5 labor hours.Day Care:The day care can house 10 large dogs and 12 small dogs daily.Day care is offered 6 days a week.Boarding:There are 12 kennels (single dog only).Boarding (kennel services) is offered every day.Facilities:The Grooming facility is 200 square feetThe Boarding facility is 2,500 square feetThe Day Care facility is 1,500 square feetGeneral:Loan for start-up costs - monthly payment of $420; in effect immediately; limited cash and loan funding - used angel investorsModest monthly draw of $600 a month for first year;

- 8. should be divided evenly among the services (grooming, day care, boarding)SALARY & HIRING DATAGroomer - $12.00 an hour, 40 hours a weekDay Care Attendant - $9.00 per hour, 22 days per month, 8 hours a dayReceptionist - $8.50 per hour, 30 hours a weekKennel Attendant - $11.50 per hour, 22 days per month, 8 hours a dayOTHER COST DATAGrooming:Dog Grooming Arm - $300.Grooming Table - $900Grooming Tub - $2,800Clippers - $136.99; can be used for 100 groomsShampoo - $103.96 per 5-gallon pail; can be used for 100 groomsSalon Tuff Capri Mobile Carry Cart - $90Scissors (7-inch straight) - $194.99; used for 200 groomsScissors (ear and nose) - $7.49; used for 200 groomsDay Care:Fencing for Day Care area - $1,249Fencing Installation - $1,000Toys - $3.29 per 6 pack; one toy will last for two dogs in day care per dayRubberized Flooring for Day Care - $3,800Boarding:12 Kennels; Depreciation is $80 per monthGeneral:Food and Water bowls - $3.59 per unitDay Care - two bowls last for every 75 dogs that attend daycareBoarding - two bowls last for every 100 dogs boarded; two bowls per kennelGrooming - each bowl lasts for 20 grooms and you need 4 bowls at all timesTowels - $34.99 per 12 packDay Care - 12 towels for every 25 dogsBoarding - 12 towels for every 40 dogsGrooming - 2 towels for every groom per dayHeating System - $10,000; Depreciation is $83 per month; Allocate based on square footageRent - $650 per month; Allocate based on square footageUtilities / Insurance - $600 per month; Allocate based on square footageCage Bank - $2,200 per set of 5Dryer - $1,250Cleaning ProductsOdoban - $14.55 per gallon; Each area will dilute 1 oz to 1 gallon of water; Allocate based on square footageSimple Green - $15.66 per gallon; Each area will dilute 1 oz to 1 gallon of water; Allocate based on square footage. ACC202 - MANAGERIAL ACCOUNTING HOME/xl/drawings/drawing2.xml#Home Company ProfileMILESTONE 1 - Company ProfileCompany NameXYZ CorporationLocationVisionMission

- 9. ACC202 - MANAGERIAL ACCOUNTING HOME/xl/drawings/drawing3.xml#Home Cost ClassificationXYZ CorporationMILESTONE 1 - Cost Classification ExerciseINSTRUCTIONS:Classify each item or cost as: Direct Material, Direct Labor, Manufacturing Overhead, or Period Costs.Place an X in the appropriate column. No numbers are needed.The fixed and variable cost classifications have been provided for you. For more information, see Objective 1 in Chapter 5.Item/CostDirect MaterialDirect LaborManufacturing OverheadPeriod CostsFixedVariableGroomerXDay care attendantXReceptionistXKennel attendantFood and water bowlsXFencing for day care areaInstallation of fencingDog grooming arm (attaches to table)12 kennels costDepreciation on kennelsRentXUtilities and insuranceXGrooming tableXGrooming tub 48"XHeating systemXDepreciation on heating systemXClippersShampoo (Crystal Clear: five-gallon pail)XCage bank (set of five)Salon Tuff Capri mobile carry cartTowels Scissors (7-inch straight, ear & nose)Toys (used in day care only)XCleaning products (used throughout)XDryerRubberized flooring (day care)XLoanXDrawX &8ACC202 - MANAGERIAL ACCOUNTING HOME/xl/drawings/drawing4.xml#Home Variable_FixedXYZ CorporationMILESTONE 1 - Variable and Fixed Cost ExerciseINSTRUCTIONS:Determine the per-unit cost for each dog.Fill in the blanks to get the per-unit cost and fixed cost of each service. Most costs are provided for you. Only fill in the missing costs.Based on 5 grooms per dayGROOMINGItemVariable CostsItemFixed CostsShampoo$ - 0Groomer$ - 0Clipper(s)1.37Rent30.95Bowls0.72Loan20.00Towels5.83Utiliti es and Insurance28.57Scissors1.01Depreciation on heating

- 10. system3.95Cleaning Products: Odoban2.08Cleaning Products: Simple Green2.36Draw200.00Total Variable Costs$ 9.97Total Fixed Costs$ 2,367.92Based on 22 dogs per day, 25 operating days for day care, and 22 eight-hour work days for day care attendant.DAY CAREItemVariable CostsItemFixed CostsDay care attendant$ 2.88Rent$ 232.14Toys 0.27Loan150.00Bowls0.19Utilities and Insurance- 0Towels1.40Depreciation on heating system29.64Cleaning Products: Odoban15.59Cleaning Products: Simple Green16.78Draw200.00Total Variable Costs$ - 0Total Fixed Costs$ 858.44Based on 12 dogs per day, 30 operating days for boarding, and 22 eight-hour work days for kennel attendant.BOARDINGItemVariable CostsItemFixed CostsKennel attendant$ - 0Depreciation on kennels$ 80.00Bowls0.86Rent386.90Towels0.87Loan250.00Utilities and Insurance- 0Depreciation on heating system49.40Cleaning Products: Odoban25.98Cleaning Products: Simple Green29.55Draw200.00Total Variable Costs$ 7.35Total Fixed Costs$ 1,378.97 &8ACC202 - MANAGERIAL ACCOUNTING HOME/xl/drawings/drawing5.xml#Home Instructions - Milestone 2Southern New Hampshire UniversityCollege of Continuing Education (COCE)ACC 202 - Managerial AccountingINSTRUCTIONS FOR MILESTONE 2 (Due Week 4)IMPORTANT NOTE:Make sure to completely review the rubric for Milestone 2.Use the data from this milestone and begin working on your final presentation due in Milestone 4 (Week 7).ITEMS TO COMPLETE FOR THIS MILESTONE (Green Tabs):GENERALUse data from Milestone 1 in your analysis.CONTRIBUTION MARGIN ANALYSISSelect a price for each service (grooming, day care, boarding).Determine the variable cost from the Variable_Fixed tab for each service.Calculate the contribution margin for each service based on your sales price and the variable cost for that service.BREAK-EVEN ANALYSISDetermine the fixed cost

- 11. from the Variable_Fixed tab for each service.Fixed and Variable cost designation is provided.Calculate the break-even units (round up) for each service.Calculate the break-even units (round up) for suggested target profit levels for each service. ACC202 - MANAGERIAL ACCOUNTING HOME/xl/drawings/drawing6.xml#Home Contribution Margin AnalysisXYZ CorporationMILESTONE 2 - Contribution Margin per Unit and Contribution Margin RatioINSTRUCTIONS:Select a price from the scenarios below and compute the contribution for each service based on your selected price.Variable cost per unit comes from your Variable_Fixed tab completed in Milestone 1.SCENARIO (choose one from each category):Dog Day Care1. With pricing at $18 per dog per day, you can expect to have 22 dogs per day.2. With pricing at $20 per dog per day, you can expect to have 15 dogs per day.3. With pricing at $25 per dog per day, you can expect to have 10 dogs per day.Overnight Boarding1. With pricing at $25 per dog per day, you can expect to have 12 dogs per day.2. With pricing at $28 per dog per day, you can expect to have 10 dogs per day.3. With pricing at $30 per dog per day, you can expect to have 7 dogs per day.Basic Groom1. With pricing at $25 per dog per day, you can expect to have 5 dogs per day.2. With pricing at $30 per dog per day, you can expect to have 4 dogs per day.3. With pricing at $35 per dog per day, you can expect to have 3 dogs per day.DAY CAREBOARDINGGROOMINGSales Price$ - 0$ - 0$ - 0Variable Cost per Unit- 0- 0- 0Contribution Margin$ - 0$ - 0$ - 0 &8ACC202 - MANAGERIAL ACCOUNTING HOME/xl/drawings/drawing7.xml#Home Break-Even AnalysisXYZ CorporationMILESTONE 2 - Break- Even AnalysisINSTRUCTIONS:Show all steps and calculations to determine the break-even.Determine the break-even for the target profit levels as outlined in the instructions. Round all

- 12. decimals UP to next whole number.Break-even = Fixed Costs / Contribution MarginDAY CAREBOARDINGGROOMINGSales Price$ - 0$ - 0$ - 0Fixed Costs$ - 0$ - 0$ - 0Contribution Margin$ - 0$ - 0$ - 0Break-Even Units (round up)- 0- 0- 0Target Profit$ 417.00$ 583.00$ 1,000.00Break-Even Units (round up)- 0- 0- 0Target Profit$ 667.00$ 909.00$ 1,500.00Break-Even Units (round up)- 0- 0- 0 &8ACC202 - MANAGERIAL ACCOUNTING HOME/xl/drawings/drawing8.xml#Home Instructions - Milestone 3Southern New Hampshire UniversityCollege of Continuing Education (COCE)ACC 202 - Managerial AccountingINSTRUCTIONS FOR MILESTONE 3 (Due Week 5)IMPORTANT NOTE:Make sure to completely review the rubric for Milestone 3.Use the data from this milestone and begin working on your final presentation due in Milestone 4 (Week 7).ITEMS TO COMPLETE FOR THIS MILESTONE (Purple Tabs):GENERALUse data from Milestone 1 and Milestone 2 in your analysis.Data needed for the income statement will be shared in an announcement at the end of Module Four.COST OF SERVICES SCHEDULE (THIS IS THE SAME AS A COST OF GOODS MANUFACTURED SCHEDULE. THIS IS USED FOR SERVICE COMPANIES.)Use the data at the top of the schedule to complete the report.INCOME STATEMENTUse the data at the top of the schedule to complete the report.Use the data from your COS Schedule.VARIANCESUse the data at the top of the schedule to calculate the following:VarianceFavorable / Unfavorable ACC202 - MANAGERIAL ACCOUNTING HOME/xl/drawings/drawing9.xml#Home COS ScheduleXYZ CorporationMILESTONE 3 - Statement of Cost of ServicesINSTRUCTIONS:The following are the actual numbers for January:MaterialsPurchased $5,000 of MaterialsConsumed 40% of those purchased materialsDirect

- 13. LaborDirect Labor was $6,240Factory OverheadFactory Overhead was $2,800XYZ CorporationStatement of Cost of ServicesFor the Month Ended January 31, xxxxBeginning Work- in-Process Inventory$ - 0Direct Materials:Materials - Beginning$ - 0Add: Purchases for month of January- 0Materials Available for Use$ - 0Deduct: Ending Materials- 0Materials Used $ - 0Direct Labor- 0Factory Overhead- 0Total Manufacturing Overhead$ - 0Deduct: Ending Work-in-Process Inventory- 0Cost of Services$ - 0 &8ACC202 - MANAGERIAL ACCOUNTING HOME/xl/drawings/drawing10.xml#Home Income StatementXYZ CorporationMILESTONE 3 - Income StatementINSTRUCTIONS:Complete the statement in proper form.Revenue will be provided in an announcement at the end of Module 4 (based on actual number of services for your pricing levels).Additional information necessary to complete the income statement:General and Administrative Salaries paid = $1,200Advertising = $100Cleaning Products = $120Depreciation = $83Rent = $650Loan = $420Utilities and Insurance = $600XYZ CorporationIncome StatementFor the Month Ended January 31, xxxxRevenue:Grooming$ - 0Day Care- 0Boarding- 0Total Revenue$ - 0Cost of Goods Sold *- 0Gross Profit$ - 0Expenses:G&A Salaries$ - 0Advertising - 0Cleaning Products- 0Depreciation- 0Rent- 0Loan- 0Utilities and Insurance- 0Total Expenses$ - 0Net Income / Loss$ - 0* Cost of Goods Sold = Cost of Services (COS) There is no finished goods inventory to maintain. &8ACC202 - MANAGERIAL ACCOUNTING HOME/xl/drawings/drawing11.xml#Home VariancesXYZ CorporationMILESTONE 3 - Variance AnalysisINSTRUCTIONS:Prepare the variances and identify whether they are favorable or unfavorable.The below website will provide further assistance with variances:http://accounting- simplified.com/management/variance-

- 14. analysis/material/price.htmlDATA FOR VARIANCE ANALYSIS:Standard Hours / QtyStandard RateActual Hours / QtyActual RateGrooming Labor150$ 12.00180$ 11.50Grooming Materials1,000$ 2.001,200$ 3.00VarianceFavorable/ UnfavorableGroomer Direct Labor Time Variance(Actual Hours - Standard Hours) x Standard Rate$ - 0Groomer Direct Labor Time Variance(Actual Rate - Standard Rate) x Actual Hours$ - 0Groomer Direct Labor Time Variance(Actual Quantity - Standard Quantity) x Standard Price$ - 0Groomer Direct Labor Time Variance(Actual Price - Standard Price) x Actual Quantity$ - 0 &8ACC202 - MANAGERIAL ACCOUNTING HOME/xl/drawings/drawing12.xml#Homehttp://accounting- simplified.com/management/variance- analysis/material/price.html 1 ACC 202 Final Project Guidelines and Rubric Overview Successful entrepreneurs understand all aspects of business, especially costs and costing systems. Managerial accounting provides a framework for strategic analysis and planning with regard to cost behaviors and costing systems. In this final project, you have the opportunity to act as an entrepreneur and apply managerial accounting principles to evaluate and manage costs

- 15. related to your products within a costing system. Additionally, you will demonstrate your ability to communicate your findings effectively to internal stakeholders, just as an actual business owner would need to do. Specifically, you will assume the role of the owner of a hypothetical small business. In your milestone work, you will develop financial strategies prior to opening your business. For the final submission, you will create a presentation for your investors after your business has been in operation for a certain period of time. You will use the provided scenarios to complete your project. The project is divided into three milestones, which will be submitted at various points throughout the course to scaffold learning and ensure quality final submissions. These milestones will be submitted in Modules Two, Four, and Five. The final product will be submitted in Module Seven. In this assignment, you will demonstrate your mastery of the following course outcomes: -202-01: Apply fundamental costing systems to optimize operations within a business -202-02: Assess financial performance to communicate financial planning strategies to internal stakeholders -202-03: Leverage fundamental managerial accounting methods to support the mission of an organization Prompt In a detailed presentation (12 to 15 slides in length, plus speaker notes and an addendum), explain and defend your

- 16. costing strategies (i.e., the business plan created in your first and second milestones) and share your business’s performance to-date (i.e., the work from your third milestone). Be sure to effectively communicate to your stakeholders by breaking down concepts and using investor-friendly language to build their trust and confidence. Specifically, the following critical elements must be addressed. Most of the critical elements align with a particular course outcome (shown in brackets). I. Introduce your presentation A. Outline your company’s profile, including its name, location, and mission and vision. B. Explain for your investors the purpose of the presentation. What do you plan to communicate, and why should your investors pay attention? In other words, try to persuade your investors that the accounting information you are about to share is important. [ACC-202-03] C. Explain and defend your methods for generating the information that you are about to share in terms of your adherence to industry standards and the AICPA code of ethics. In other words, why should your investors trust that you are delivering accurate financial data and that your decision-making process has been ethical? [ACC-202-03] 2

- 17. D. Specifically, be sure to illustrate how your managerial accounting methods support the mission of your organization, using examples. [ACC-202- 03] II. Financial Strategy: Review your original business plan and costing strategies using the prior-to-opening scenario information. A. Justify your use of job order costing. Be sure to compare and contrast the various costing systems you learned about in this course as part of your defense. [ACC-202-01] B. Explain and defend the selling prices that you established for grooming, day care, and boarding. Be sure to reference your cost-volume-profit analysis in your defense. [ACC-202-02] C. Explain and defend your selected target profits for each area of your business. Be sure to reference your cost-volume-profit analysis in your defense. [ACC-202-02] D. Explain and defend your contribution margin per unit and contribution margin ratio. Be sure to reference your cost- volume-profit analysis in your defense. [ACC-202-02] III. Financial Statements: Assess your financial performance to- date using the post-opening scenario information. A. Financial Statements 1. Share the statement of cost of services and logically interpret

- 18. the business’s performance against the provided benchmarks. [ACC-202- 02] 2. Share the income statement and logically interpret the business’s performance against the provided benchmarks. [ACC-202-02] B. Variance Analysis 1. Identify all variances for the direct labor time and the materials price. [ACC-202-02] 2. Evaluate the significance of the variances in terms of the potential to impact future budgeting decisions and planning. [ACC-202-02] IV. In an addendum, submit your completed workbook, including the following: A. Accurately classify all of your costs in the “Cost Classification” tab. [ACC-202-01] B. Conduct a cost-volume profit analysis: 1. Determine your contribution margin per unit and contribution margin ratio in the “Contribution Margin Analysis” tab. [ACC- 202-01] 2. Determine your break-even points for achieving your target profits in the “Break-even analysis” tab. [ACC-202-01] Milestones Milestone One: First Part of Workbook In Module Two, you will submit the “Cost Classifications” and “Variable_Fixed” tabs in your provided final project workbook. This milestone will be graded with the Milestone One Rubric.

- 19. 3 Milestone Two: Second Part of Workbook In Module Four, you will submit the “Contribution Margin Analysis” and “Break-even Analysis” tabs in your provided final project workbook. This milestone will be graded with the Milestone Two Rubric. Milestone Three: Final Workbook In Module Five, you will submit “COS Schedule,” “Income Statement,” and “Variances” tabs in your provided final project workbook. This milestone will be graded with the Milestone Three Rubric. Final Submission: Presentation to Investors In Module Seven, you will submit your final project. It should be a complete, polished artifact containing all of the critical elements of the final prompt. It should reflect the incorporation of feedback gained throughout the course. This submission will be graded with the Final Project Rubric. Deliverables Milestone Deliverable Module Due Grading One Cost Classification Tabs Two Graded separately; Milestone One Rubric Two Financial Scope of the Business Plan Four Graded

- 20. separately; Milestone Two Rubric Three Draft Presentation to Investors Five Graded separately; Milestone Three Rubric Final Submission: Presentation to Investors Seven Graded separately; Final Project Rubric Final Project Rubric Guidelines for Submission: Your presentation to investors must be at least 12–15 slides plus speaker notes, and all citations should follow APA formatting. Critical Elements Exemplary (100%) Proficient (85%) Needs Improvement (55%) Not Evident (0%) Value Introduce: Company’s Profile Meets “Proficient” criteria and judiciously includes details relevant to the target audience of the presentation Outlines the company’s profile, including its name, location, and mission and vision Outlines the company’s profile but fails to include its name, location, and mission and vision Does not outline the company’s profile

- 21. 3 4 Introduce: Purpose [ACC-202-03] Meets “Proficient” criteria and demonstrates nuanced appreciation for the role of managerial accounting in ethically supporting the mission of an organization Explains the purpose of the presentation, including a persuasive case for the importance of the accounting information to be shared Explains the purpose of the presentation, but fails to fully or persuasively make a case for the importance of the accounting information Does not explain the purpose of the presentation 7 Introduce: Defend of

- 22. Methods [ACC-202-03] Meets “Proficient” criteria and demonstrates nuanced appreciation for the role of managerial accounting in ethically supporting the mission of an organization Explains and defends the methods for generating the information in the presentation in terms of their adherence to industry standards and the AICPA code of ethics Explains the methods for generating the information in the presentation, but fails to fully defend the methods in terms of their adherence to industry standards and the AICPA code of ethics Does not explain the methods for generating the information in the presentation 7 Introduce: Support the Mission [ACC-202-03]

- 23. Meets “Proficient” criteria and demonstrates nuanced appreciation for the role of managerial accounting in ethically supporting the mission of an organization Illustrates how the managerial accounting methods support the mission of the organization using specific examples Discusses how the managerial accounting methods support the mission of the organization, but fails to fully or accurately illustrate using specific examples Does not discuss illustrate how the managerial accounting methods support the mission of the organization 7 Financial Strategy: Costing Systems [ACC-202-01] Meets “Proficient” criteria and demonstrates keen insight into key cost behaviors and cost systems

- 24. Justifies the use of job order costing by comparing and contrasting the various costing systems covered in the course Discusses the use of job order costing but fails to fully or accurately justify its use by comparing and contrasting the various costing systems covered in the course Does not discuss the use of job order costing 6 Financial Strategy: Selling Prices [ACC-202-02] Meets “Proficient” criteria and demonstrates strategic ability to propose costing solutions supported by the financial data Explains and defends the selling prices for grooming, day care, and boarding by citing financial data from the cost-volume- profit analysis Explains the selling prices for grooming, day care, and boarding, but fails to fully or

- 25. accurately defend each price by citing financial data from the cost-volume-profit analysis Does not explain the selling prices for grooming, day care, and boarding 8 Financial Strategy: Target Profits [ACC-202-02] Meets “Proficient” criteria and demonstrates strategic ability to propose costing solutions supported by the financial data Explains and defends the target profits for each area of the business by citing financial data from the cost-volume-profit analysis Explains the target profits for each area of the business, but fails to fully or accurately defend each one by citing financial data from the cost- volume-profit analysis Does not explain the target profits for each area of the business

- 26. 8 5 Financial Strategy: Contribution Margin [ACC-202-02] Meets “Proficient” criteria and demonstrates strategic ability to propose costing solutions supported by the financial data Explains and defends the contribution margin per unit and contribution margin ratio by citing financial data from the cost-volume-profit analysis Explains the contribution margin per unit and contribution margin ratio, but fails to fully or accurately defend each by citing financial data from the cost-volume- profit analysis Does not explain the contribution margin per unit and contribution margin ratio 8

- 27. Financial Statements: Statement of Cost of Services [ACC-202-02] Meets “Proficient” criteria and demonstrates sophisticated ability to evaluate critical performance measures for strategic planning Shares the statement of cost of services and logically interprets the business’s performance against the provided benchmarks Shares the statement of cost of services, but there are inaccuracies in the statement, or the interpretation has gaps in logic or fails to address the provided benchmarks Does not share the statement of cost of services 6 Financial Statements: Income

- 28. Statement [ACC-202-02] Meets “Proficient” criteria and demonstrates sophisticated ability to evaluate critical performance measures for strategic planning Shares the income statement and logically interprets the business’ performance against the provided benchmarks Shares the income statement, but there are inaccuracies in the statement or the interpretation has gaps in logic or fails to address the provided benchmarks Does not share the income statement 6 Variance Analysis: Identify [ACC-202-02] Meets “Proficient” criteria and demonstrates sophisticated ability to evaluate critical performance measures for strategic planning

- 29. Accurately identifies all variances for the direct labor time and the materials price Identifies variances for the direct labor time and the materials price, but fails to fully or accurately identify each Does not identify variances for the direct labor time and the materials price 6 Variance Analysis: Significance of the Variance [ACC-202-02] Meets “Proficient” criteria and demonstrates sophisticated ability to evaluate critical performance measures for strategic planning Evaluates the significance of the variances in terms of their potential to impact future budgeting decisions and planning Evaluates the significance of the variances, but fails to fully

- 30. or accurately identify their potential to impact future budgeting decisions and planning Does not evaluate the significance of the variances 7 Addendum: Classify Costs [ACC-202-01] Meets “Proficient” criteria and demonstrates keen insight into key cost behaviors and cost systems Accurately classifies all costs in the “Cost Classification” tab of the workbook Classifies costs in the “Cost Classification” tab, but fails to fully or accurately classify each Does not classify costs in the “Cost Classification” tab of the workbook 6

- 31. 6 Addendum: Contribution Margin [ACC-202-01] Meets “Proficient” criteria and demonstrates keen insight into key cost behaviors and cost systems Determines the contribution margin per unit and contribution margin ratio in the “Contribution Margin Analysis” tab of the workbook Determines the contribution margin per unit and contribution margin ratio in the “Contribution Margin Analysis” tab of the workbook, but fails to fully or accurately complete the analysis Does not determine the contribution margin per unit and contribution margin ratio in the “Contribution Margin Analysis” tab of the workbook 6 Addendum: Break-

- 32. Even Points [ACC-202-01] Meets “Proficient” criteria and demonstrates keen insight into key cost behaviors and cost systems Determines the break-even points for achieving the target profits in the “Break-even analysis” tab of the workbook Determines the break-even points for achieving the target profits in the “Break-even analysis” tab of the workbook, but fails to fully or accurately complete the analysis Does not determine the break- even points for achieving the target profits in the “Break- even analysis” tab of the workbook 6 Effective Business Communication [ACC-202-02] Meets “Proficient” criteria and demonstrates sophisticated

- 33. ability to effectively communicate to internal stakeholders Main ideas are clearly communicated and references are properly cited throughout the presentation There are minor issues with the communication of ideas or use of citations that negatively impact the effectiveness of the presentation There are critical errors in the communication of ideas that negatively impact basic comprehension of the presentation 3 Total 100% 7 Appendix

- 34. Scenario: Prior to Opening, Part I: You plan to open a pet- services business that will offer dog grooming, day care, and boarding. You can be creative in deciding the name of your business (e.g., “Inspiring Dog Care”), its geographical location (e.g., Chicago), and its mission and vision for adding value to the community. You will be asked to make choices for a few other details to customize your case; otherwise, you should use the information below. There are 12 kennels (single dog only) and the day care area can house 10 large dogs and 12 small dogs each day. The grooming facility is 200 square feet, the boarding facility is 2,500 square feet, and the day care is 1,500 square feet. Your groomer can groom five dogs a day for five days a week; each groom consists of 1.5 labor hours. You also offer dog day care six days a week, and kenneling every day. You have taken out a loan for start-up costs and the monthly payment is $420; it goes into effect immediately and should be accounted for in your costs. With limited cash contribution and loan funding, you located two angel investors. You will collect a modest draw for the first year of $600 a month; remember to divide evenly among the services. Note: For simplicity, base all calculations using 30 days in each month. You estimate the following staffing needs: week our and will work 22 eight-hour days per month

- 35. a week work 22 eight-hour days per month A complete list of additional costs is provided below: o Daycare: Two bowls last for every 75 dogs that attend daycare. o Boarding: Two bowls last for every 100 dogs that are boarded; you need two bowls per kennel. o Grooming: Each bowl lasts for 20 grooms and you need four bowls at all times. $1,000 ies/insurance: $600/month; allocate based on square footage

- 36. 8 based on square footage -gallon pail, which can be used for 100 grooms o Day care: You need to have 12 towels for every 25 dogs. o Boarding: You need to have 12 towels for every 40 dogs. o Grooming: You need to have two towels for every groom per day. -inch straight is $194.99, and (1) ear-and-nose is $7.49; each can be used for 200 grooms. -pack; one toy will last for two dogs in day care, per day. o Odoban: $14.55/gallon: Each area will dilute 1 oz to 1 gallon of water; allocate based on square footage. o Simple Green: $15.66/gallon: each area will dilute 1 oz to 1 gallon of water; allocate based on square footage.

- 37. Scenario: Prior to Opening, Part II: Your market research indicated the following price ranges as optimal for your area: o With pricing at $18 per dog per day, you can expect to have 22 dogs per day. o With pricing at $20 per dog per day, you can expect to have 15 dogs per day. o With pricing at $25 per dog per day, you can expect to have 10 dogs per day. o With pricing at $25 per dog per day, you can expect to have 12 dogs per day. o With pricing at $28 per dog per day, you can expect to have 10 dogs per day. o With pricing at $30 per dog per day, you can expect to have 7 dogs per day. o With pricing at $25 per groom, you can expect to do 5 grooms per day. o With pricing at $30 per groom, you can expect to do 4 grooms per day. o With pricing at $35 per groom, you can expect to do 3 grooms per day. Additionally, you need to compare your break-even points for the following target profits for each area of your business:

- 38. 9 o Break-even o $417 target profit each month o $667 target profit each month o Break-even o $583 target profit each month o $909 target profit each month o Break-even o $1,000 target profit each month o $1,500 target profit each month Post-opening Scenario: Your angel investors are silent in relation to the business; however, they require board meetings for status updates on the company’s financial health. Therefore, you need to analyze your company’s performance over the last month using the data provided below. Note: Your instructor will create an announcement sharing the income statement data by the end of Module Four. All of the data you need for the cost-of- goods-manufactured statement can be found in the “COS Schedule” tab of your workbook. For your variance analysis, use the following financial data:

- 39. Direct Materials/Labor Original Projection Actual Shampoo 1000 ounces ($2/groom) 1200 ounces ($3/groom) Grooming Labor 1.5 hrs/groom @ $12 2.25 hrs/groom @ $11.50 Running head: PICOT STATEMENT 1 PICOT STATEMENT 5 PICOT Statement Grand Canyon University July 1, 2018 PICOT Statement P- Elderly patients (aged 65 years and above) I.- Improving workflow and use of health information technologies C- Home-based care O- Improved quality of care and increased patient safety T- Two months Patient Population and Problem Elderly patients (aged 65 and above) face many health problems within the primary care setting. Consequently, nurses

- 40. and other health care professionals normally grapple with the challenge of improving quality of care and patient safety for this population (Boltz et al. 2016). Elderly patients are often vulnerable to many health hazards that might affect the quality of care and their safety. For instance, their cognitive functioning reduces as their age progress. In addition, they normally have a high propensity to avoid taking prescriptions and medications. Furthermore, elderly patients normally register high rates of allergic responses, coupled with falls and inability to request for assistance from nurses. Improving workflow within nurses’ working environments can help to reduce these health problems (National Council of State Boards of Nursing,2010). The work processes for nurse and physicians in primary healthcare settings might not be effective in taking preventive measures to ensure that elderly patients’ quality and safety are guaranteed. These include protection form hazards such as immobility, muscle atrophy, falls, and contractures. Intervention The utilization of evidence-based practice can support nursing interventions to improve workflow and quality of care. The task of improving workflow should focus on integrating technologies into the existing nurses’ work environments such as people, roles, and work procedures. Nurses and other healthcare team should complete tasks by adhering to the appropriate work procedures. Healthcare institutions should introduce health information systems such as EHRs in order to optimize the benefits to nursing care (Grain et al. 2014). There is need to introduce systems that support nurses in the delivery of their duties and responsibilities. For instance, technological systems should be introduced to support nurses in their efforts to complete the tasks of documentation of vital signs of elderly patients, as well as ability to develop charts of vital signs and search functions (Isono et al. 2017). In addition, nurses who operate in busy environments should develop a work breakdown sheet that identifies the details of their tasks. Training programs should also be introduced to enhance performance and

- 41. satisfaction. Comparison As an alternative, home-based care can be provided to elderly patients. However, when compared to use of evidence- based practice in primary care, home-based interventions may be associated with various potential adverse effects. For instance, many health professionals are often inaccurate in presuming that home-based care does not come with economic and emotional costs. In most situations, home-based interventions are associated with considerable emotional and financial burden. Most caregivers are often women, and they have a propensity to have minimal access to or control of resources required to assume this responsibility. Sometimes, they are not often available to prevent patients from falling, or avoiding medications. Outcomes The utilization of technology and workflow process improvement initiatives can help to improve safety and quality of care among elderly patients. The outcomes of these nursing interventions are far and wide. This is because they result in reduced cases of falls among elderly patients. In addition, they help to constantly keep records of medications that are taken by the patients and quick detection of the potential problems that might hinder the patients from recovery. Improvements in workflow have the potential to enable nurses and physicians to get important information about patient disease status and healthcare processes. Healthcare agencies that embrace health information systems and improve workflow are able to keep track of progresses being made by many elderly patients within primary care settings. Time These evidence-based interventions can be implemented within a span of two months. Their successes can result in positive health outcomes for elderly patients immediately. In addition, workflow improvements can yield the desired fruits both in the long-term and long-run. In the short-run, nurses are

- 42. most likely to improve their productivity. References Boltz, M., Capezuti, E., Fulmer, T. T., & Zwicker, D. (Eds.). (2016). Evidence-based geriatric nursing protocols for best practice. New York: Springer Publishing Company. Grain, H., Martin-Sanchez, F., & Schaper, L. K. (Eds.). (2014). Investing in E-health: People, Knowledge and Technology for a Healthy Future: Selected Papers from the 22nd Australian National Health Informatics Conference (HIC 2014) (Vol. 204). IOS Press. Isono, H., Suzuki, S., Ogura, J., Haruta, J., & Maeno, T. (2017). Improving the workflow of nursing assistants at a general hospital in Japan. BMJ Open Qual, 6(2), e000106. National Council of State Boards of Nursing. (2010). Nursing Pathways for Patient Safety E- book. New York: Elsevier Health Sciences. Literature Evaluation Table Student Name: Change Topic (2-3 sentences): Criteria Article 1 Article 2 Article 3

- 43. Article 4 Author, Journal (Peer-Reviewed), and Permalink or Working Link to Access Article Article Title and Year Published Research Questions (Qualitative)/Hypothesis (Quantitative), and Purposes/Aim of Study Design (Type of Quantitative, or Type of Qualitative) Setting/Sample Methods: Intervention/Instruments

- 44. Analysis Key Findings Recommendations Explanation of How the Article Supports EBP/Capstone Project Criteria Article 5 Article 6 Article 7 Article 8 Author, Journal (Peer-Reviewed), and

- 45. Permalink or Working Link to Access Article Article Title and Year Published Research Questions (Qualitative)/Hypothesis (Quantitative), and Purposes/Aim of Study Design (Type of Quantitative, or Type of Qualitative) Setting/Sample Methods: Intervention/Instruments

- 46. Analysis Key Findings Recommendations Explanation of How the Article Supports EBP/Capstone © 2015. Grand Canyon University. All Rights Reserved. © 2017. Grand Canyon University. All Rights Reserved.