1. Name ofcompany: GlaxoSmithKline PLC RIC: GSK.L

Price: 1598.00 GBp Date: 12/01/2014

GICS: Healthcare

Company profile:

GlaxoSmithKline PLCisa research-basedpharmaceutical company.The companydevelops,

manufacturesandmarketsvaccines,prescriptionandoverthe countermedicinesaswell ashealth-

relatedconsumerproducts.

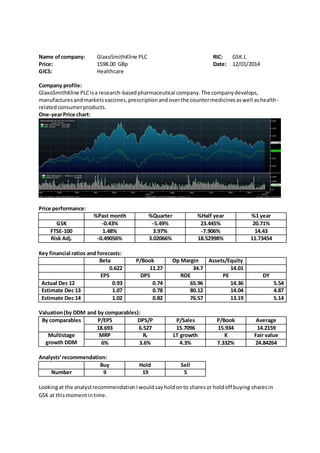

One-yearPrice chart:

Price performance:

%Past month %Quarter %Half year %1 year

GSK -0.43% -5.49% 23.445% 20.71%

FTSE-100 1.48% 3.97% -7.906% 14.43

Risk Adj. -0.49056% 3.02066% 18.52998% 11.73454

Key financial ratios and forecasts:

Beta P/Book Op Margin Assets/Equity

0.622 11.27 34.7 14.01

EPS DPS ROE PE DY

Actual Dec 12 0.93 0.74 65.96 14.36 5.54

Estimate Dec 13 1.07 0.78 80.12 14.04 4.87

Estimate Dec 14 1.02 0.82 76.57 13.19 5.14

Valuation(by DDM and by comparables):

By comparables P/EPS DPS/P P/Sales P/Book Average

18.693 6.527 15.7096 15.934 14.2159

Multistage

growth DDM

MRP Rf LT growth K Fair value

6% 3.6% 4.3% 7.332% 24.84264

Analysts’recommendation:

Buy Hold Sell

Number 9 19 5

Lookingat the analystrecommendationIwouldsayholdonto sharesor holdoff buying sharesin

GSK at thismomentintime.

2. Introduction

GlaxoSmithKline plc(GSK),incorporatedonDecember6,1999, isglobal healthcare group,

whichisengagedinthe creationand discovery,development,manufacture andmarketingof

pharmaceutical products, includingvaccines,over-the-counter(OTC) medicinesandhealth-

relatedconsumerproducts.The Companyoperatesinthree primaryareasof business:

Pharmaceuticals,VaccinesandConsumerHealthcare.

Price performance and newsanalysis:

Date Tesco FTSE-100 Numerical

Calculation

Risk adjusted

31/12/2013 1607 (-0.71%) 6749.09(1.20%) 0.71-0.622*1.20 -0.0364%

29/11/2013 1618.5(-1.52%) 6650.57(-1.20%) 1.51-0.622*1.20 1.52%

31/10/2013 1643.5(5.52%) 6731.43(4.20%) 5.52-0.622*4.20 5.52%

30/09/2013 1557.5(-5.35%) 6462.22(0.80%) 5.35-0.622*0.80 5.35%

30/08/2013 1645.5(-2.29%) 6412.93(-3.14%) 2.29-0.622*3.14 2.29%

31/07/2013 1684(2.18%) 6621.06(6.50%) 2.18-0.622*6.50 2.18%

28/06/2013 1648(-3.82%) 6215.47 (-5.58%) 3.82-0.622*5.58 3.82%

31/05/2013 1713.5(3.19%) 6583.09(2.38%) 3.19-0.622*2.38 3.19%

30/04/2013 1660.5(7.93%) 6430.12(0.29%) 7.93-0.622*0.29 7.93%

29/03/2013 1538.5(5.66%) 6411.74(0.80%) 5.66-0.622*0.80 5.66%

28/02/2013 1456(0.73%) 6360.81(1.34%) 0.73-0.622*1.34 0.73%

31/01/2013 1445.5(8.28%) 6276.88(6.43%) 8.28-0.622*6.43 8.28%

News:Two firm-specificnewsitemsandtwo systematic announcements

Date Newssummary Briefcomments

Jul 27, 2011

03:51:18 AM

Firm-specific

GlaxoSmithKline PLC(GSKLN) wasraisedto

"Buy"from "Sell"atBryan Garnier& Cie by

equityanalystEricLe Berrigaud.The target

price isGBp 1,600.00 pershare.

GlaxoRises;PESet to BidFor OTC Unit,Dow

JonesSays

GSK LN trading0.8% higher,vol.55% of 3-mo.

dailyavg.;amongtop SXXPHealthcare gainers.

Thisnewsmeansthat GSK

share price is expectedto

grow andone analystnow

saysthat you shouldbuy

sharesnot sell.

May 20 2013

11:45:40

Market

systematic

U.K. Stocks Advance as Benchmark FTSE 100

Closesat12-Year High

U.K. stocks advanced for a second day as the

benchmark FTSE 100 Index closed at its highest

level since September2000.

The FTSE 100 added 32.57 points, or 0.5

percent, to 6,755.63 at the close in London. The

gauge climbed 1.5 percent last week and has

surged 15 percent so far this year, boosted by

central-bank stimulus. The broader FTSE All-

Share Index gained 0.4 percent today for a 13th

straight advance, it’s longest since 1987.

This news article shows that

the Market has risen to its

highest in 12 years. This has

been helped from the

central-bank stimulus. This

also has helped boost

companies in the FTSE 100,

as you can see in the graph

that GSK also rose along

with the market price at this

time.

3. Ireland’s ISEQ Index increased 1.5 percent to

the highestlevelsince September2008.

Oct 7 2013

11:36:10

Market Specific

London Cash Buyers Send Banks North to

RiskierLoans:Mortgages

The risky loans that helped cause the U.K.’s

real-estate crash are making a comeback as

cash buyers from abroad limit lending

opportunities in London and banks instead

venture intothe weakestmarkets.

David Cameron’s government this week

introduces mortgage guarantees designed to

allow people to buy a home costing as much as

600,000 pounds

This article explains the

contribution to the market

price dropping. It is because

banks were continuing to

give out risky mortgages in

weak markets because of

the announcement from the

government. This has

especially affected the

Northregion.

Jul 02, 2013

03:14:52 AM

[NYT]

Firm Specific

GlaxoSmithKline IsInvestigatedinChina

The British pharmaceutical giant

GlaxoSmithKline said on Monday that the

authorities here were investigating whether

senior managers working for the company in

Chinawere involvedin"economiccrimes."

This could harm the

companies brand image as

well as turn out to be a

costly lawsuit if found guilty

of bribery. This could have a

dramaticon the share price.

Valuation:

Multi-stage DDM

Firstyou mustworkout whatK equals-

K= Rf + B (E(Rm)-Rf)

K= 3.6 +0.622*6= 7.332% or 0.07332

Analyst Forecast

V0=

074

1+0.07332

+

0.78

(1+0.07332)2

+

0.82

(1+0.07332)3

+

0.82(1+0.07369)

(0.07332−0.07369) 𝑥(1+0.07332)^3 =204.8904

Economic Model Forecast V0=

0.74

1+0.07332

+

0.78

(1+0.07332)2

+

0.82

(1+0.07332)3

+

0.82(1+0.043)

(0.07332−0.043) 𝑥(1+0.07332)^3 = 24.84264

DDM ROE Forecast

V0=

0.74

1+0.07332

+

0.78

(1+0.07332)2

+

0.82

(1+0.07332)3

+

0.82(1+0.16901)

(0.07332−0.16901) 𝑥(1+0.07332)^3 = -6.07204

The Vo that I woulduse isthe EconomicModel forecastthisisbecause mygrowthrate was higher

than myK for the ROE forecastand analystforecast.Iincludedthe raw betawhencalculatingthe

DDM. The smallestvariationtothe marketprice wasthe EconomicModel forecast,whichcame out

the closest.The othershada muchlarger variationone beingaminusfigure,the other wasmuch

higher.Thisisbecause the growthrateswere muchgreaterthan K and because of thisyoushouldn’t

use theirDDM.

You alsoneedtodiscuss howyou arrive at the estimate of LT growthrate of dividends(e.g.,from

analysts’forecast,ROE*bor macro-economicbasedmodel).If there islarge deviationbetweenV0

4. and marketprice,a report that gainsa highmark wouldoffersome reasonableexplanationsfor the

difference.

EPS DPS ROE

Actual Dec 12 0.93 0.74 65.96

Estimate Dec 13 1.07 0.78 80.12

Estimate Dec 14 1.02 0.82 76.57

Analysts’ forecast Economic model ROE*b

LT growth rate 7.369% 4.3% 16.901%

How I calculate ROE*b

b= 1- AvgDPD/ AvgEPS

b= 1-0.78/1.006= 0.2277

ROE*b= Avg ROE * b

ROE*b=0.2277* 74.216

You getthe longtermgrowthrate of dividendsforROE*bas seeninthe calculationsabove.You

needtofindthe average forEPS and DPS.This helpscalculate b.Thentoget ROE*b youfindthe

average ROE and multiplyb.

You can findthe analystsforecastforlongtermgrowth rate on BloombergbytypingANR inthe top

leftbox andthe figure canbe foundon that page.

By comparables:

Use sectormedianratioto estimate fairprice usingPE,P to Book, DividendYield,Price toSalesand

take the medianvalue of these fairpricesasthe intrinsicvalue bycomparable

Numerical calculationsneedtobe shown.

PE DY P to Book P to Sales

Tesco 14.36 5.54 11.27 2.48

Sector median 20.10 4.83 12.85 2.92

EPS DPS BVPS Sales PS

Tesco 0.93 0.74 1.240 5.38

Answersand calculationsfor valuation by comparable (see tearsheet):

Sectormedian* GSK EPS= 20.10*0.93=18.693

SectorMedianDY/DPS= 4.83/0.74= 6.527

SectorMedianP to Book * BVPS= 25

SectorMedianP to Sales* SalesPS= 4.3%

SML analysis:

The securitymarketline (SML) analysisiswhere youuse agraph or othervisual chartsto show the

expectedreturn-betarelationshipof the CAPM.

SML isthe mean-betarelationship;the line of bestfitisthe riskpremiumof the marketportfolio.

The beta of a securityisthe bestwayto measure itsriskas betais proportional tothe variance that

the securitycontributestothe prime riskyportfolio.The SMLprovidesabenchmarkforevaluationof

investmentperformance.

5. E(rm)=Rf-B(E(Rm)-Rf)

Raw Beta- 3.6+0.622*6= 7.332%

AdjustedBeta- 3.6+0.748*6=8.088%

Beta=1 – 3.6+1*6

Beta=0 - 3.6+0*6= 3.6%

Alpha- a+Rf+B (E(Rm)-Rf)

Raw Beta- 0.015+3.6+0.622*6= 7.347%

AdjustedBeta- 0.015+3.6+0.748*6=8.103%

As youcan see fromthe graph whenbetaisat 0 the expected returnisat3.60. Howeverthisisthe

leastriskybeta.Whenthe betais at 1 the expectedreturnis9.60% howeverthe betaismuch

higher.Asyoucan see fromthe SML calculationsthatwiththe Raw Beta (0.622 GSK’sexpected

returnsare 7.332% and the adjustedbeta(0.748) is8.088%. This can be comparedto the alpha

whichcan be seenwhere the linesinterceptthe SML.Asyou can see the figuresare slightlyhigher

than the SML line whichmeansthatthe sharesare undervalued.

Discussionof PE versus DDM methods:

The PE advantagesare that it’san easyratioto calculate andunderstand.Itisa muchbetterwayto

showthe real value of a share thanlookingat justprice.The PE allowsyoutolookat paststock

performance andcompare itto the current PE, itcan also be estimatedforthe future.Itisa very

useful benchmarkingratioasyoucan also compare itto othercompaniesPE.

Some disadvantagesof PEare that it takesintoaccount historical costslike depreciation,but

because itdoesn’ttake inflationintoaccountsothe economicvaluesare notaccurate. Itmay look

simple butit’sa challengingasyouhave to forecastthe earnings,butthese canbe affectedby

variousfactors.You cannotsay whetherthe PEis toohighor low withoutlinkingbacktothe

companies’ longtermgrowthprospectsandcurrentearningspershare.

One advantage of DDM isthat it allowsthe usertovalue the stocksbasedon the dividendthatthe

companypay.It’s a fairlyeasymethodtocalculate asyou justhave to calculate the formula.The

DMM can alsobe reversedsothatthe upto date stockprice can be usedto assignmarket

assumptionsforthe dividendgrowthandmarketreturn.

The disadvantagesof DMM are that it providesavalue fora companyunlessitpaysdividends,the

formulaalsousessome estimatedfigureslike itsfuturedividends. The methodisn’tveryaccurate

9.60%

8.09%

7.33%

3.60%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

0 0.5 1 1.5

SML Analysis

Expected Return

6. whenitcomesto companiesthathave a highgrowthrate on the stocks,it alsoignoresanybuy-

backs which meantheydon’tshowotherwaysof returningcashto stock holders.The DMM isalso

too conservative.

Analysts’view:

Natixis- 24October2013-Quarter undercontrol.

In the face of adverse impactsonsales(China),GSKmanagedtocontrol costsand publishgood

results.The group’sgrowthpotential will neverthelessremainbelow average,due tothe inevitable

erosionof Advairovertime. AfterRoche andNovartis,GlaxoSmithKlineisthe thirdEuropeangroup

to publishagoodset of results, whichwere slightlyaheadof expectations.However,the momentum

didnot come fromstrong sales,butfroman effortoncosts, withthe resultthatthere isno

significantchange tothe group’sprospects.The erosionof Advair’ssalesisneverthelessinevitable

overtime andthe newgenerationneedstosucceedif the respiratoryfranchise istogrow (+4.3% a

yearestimatedover2013-2018). Analyst Recommendation:Neutral rating maintained

Natixis- 25July2013-No valuationleverage

AlthoughQ2figuresdid notdisappoint,theyleave little scope forestimatestobe upgraded.Growth

remainssluggishrelativetothe sector.The marketcouldremainfocusedonthe corruptionaffair

and the prospectof harsherbusinessconditionsinChina. DecentQ2resultsare notenoughforus to

raise our forecasts.Lookingoutto2018, evenif new productsare successful (£5bncontributionin

2018, i.e.19% of sales),salesgrowthwill remainlimitedto2.8% a year(below the sector) with

earningsgrowthaveraging4.6%versus 5.6% for the sector. Analyst Recommendation:Hold

JPMorgan- 14 August2013 - Upside fromupcomingcatalystsbalancesoutearningsrisk

We upgrade toNeutral (UW),settinga £19 PT, 13% potential upside.Whilstwe believecons.*

expectationsfor2014 Core EPScouldprove slightlytooambitious,we seenumerous datapoints

overthe next6m that coulddrive upgrades.AnalystRecommendation:Neutral

JPMorgan- 30 October2013-Updating forQ3 and recentsetbacks,modest accelerationinunderlying

trendsexpectedfor2014.

We update forQ3, and recentsetbacks,includingthe Chinainvestigation,Advair/Breoformulary

non-coverage andpipeline failures,aswell asFX.BothRevenuesandCore EPSare trimmed6-7%

2014-18. With modestaccelerationingrowthtrendsin2014, we anticipate limitedmultiple

expansion,hence we putGSKon 14x 2015 PE, now £17.50 (prev.£19), 7% upside.Reiterate Neutral.

Analysts’recommendation:Neutral

Conclusion:

Overall Iwouldrecommendyoutoholdoff buyingorholdonto any sharesyouhave for this

company. Thisisbecause lookingatthe riskadjustedreturnsinthe past quarter isn’tveryhigh. It

oftenfollowsthe trendwiththe FTSE100. The newscan helpsupportthisasin the past quarter

there have beenproblemsinChina regardingGSKwhichmayaffectthe share price.HoweverIstill

feel youare betteroff toholdon as the price shouldimprove.AlsoIagree withthe analyst

recommendationsfromthe reportgivenandinthe tearsheet,where the majoritythinkthatyou

shouldhold.Asthe numberof people sayingholdwasmuchgreaterthanthe othersand myopinion

fromcarrying outthe researchthatit isthe bestoption. Iwouldalsorecommendusingthe

economicmodel forecastfigurefromDDMas thisiscame out withthe bestresult.Fromlookingat

the SML the stocks are undervaluedsothisalsobacksupmy argument forholding.