Problem 14-1A On January 1, 2014, Geffrey Corporation had the followi.pdf

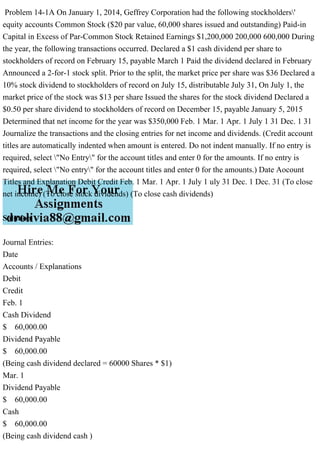

Problem 14-1A On January 1, 2014, Geffrey Corporation had the following stockholders\' equity accounts Common Stock ($20 par value, 60,000 shares issued and outstanding) Paid-in Capital in Excess of Par-Common Stock Retained Earnings $1,200,000 200,000 600,000 During the year, the following transactions occurred. Declared a $1 cash dividend per share to stockholders of record on February 15, payable March 1 Paid the dividend declared in February Announced a 2-for-1 stock split. Prior to the split, the market price per share was $36 Declared a 10% stock dividend to stockholders of record on July 15, distributable July 31, On July 1, the market price of the stock was $13 per share Issued the shares for the stock dividend Declared a $0.50 per share dividend to stockholders of record on December 15, payable January 5, 2015 Determined that net income for the year was $350,000 Feb. 1 Mar. 1 Apr. 1 July 1 31 Dec. 1 31 Journalize the transactions and the closing entries for net income and dividends. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select \"No Entry\" for the account titles and enter 0 for the amounts. If no entry is required, select \"No entry\" for the account titles and enter 0 for the amounts.) Date Aocount Titles and Explanation Debit Credit Feb. 1 Mar. 1 Apr. 1 July 1 uly 31 Dec. 1 Dec. 31 (To close net income) (To close stock dividends) (To close cash dividends) Solution Journal Entries: Date Accounts / Explanations Debit Credit Feb. 1 Cash Dividend $ 60,000.00 Dividend Payable $ 60,000.00 (Being cash dividend declared = 60000 Shares * $1) Mar. 1 Dividend Payable $ 60,000.00 Cash $ 60,000.00 (Being cash dividend cash ) Apr. 1 No entry (New shares = 60000*2 = 120000 Shares @ $20/ 2 =$10 Par value) July. 1 Stock Dividend $ 156,000.00 Dividend Distributable $ 156,000.00 (Being Stock Dividend Declared = 120000 *10% = 12000 Shares*$13 ) July. 31 Dividend Distributable $ 156,000.00 Paid in capital in excess of par- Common Stock (156000-120000) $ 36,000.00 Common Stock (12000 Shares * $10) $ 120,000.00 (Being shares issues for dividend ) Note : total number of shares after Stock Div = 120000+12000 = 132000 Dec. 1 Cash Dividend $ 66,000.00 Dividend Payable $ 66,000.00 (Being cash dividend declared = 132000 Shares * $0.50) Dec. 31 Income Summary $ 350,000.00 Retained earnings $ 350,000.00 (Being net income closed) Retained earnings $ 126,000.00 Cash Dividend (60000+66000) $ 126,000.00 (Being cash dividend closed) Retained earnings $ 156,000.00 Stock Dividend $ 156,000.00 (Being cash dividend closed) Journal Entries: Date Accounts / Explanations Debit Credit Feb. 1 Cash Dividend $ 60,000.00 Dividend Payable $ 60,000.00 (Being cash dividend declared = 60000 Shares * $1) Mar. 1 Dividend Payable $ 60,000.00 Cash $ 60,000.00 (Being cash dividend cash ) Apr. 1 No entry (New shares = 60000*2 = 120000 Shares @ $20/ 2 =$10 Par value) July. 1 Stock Dividend $ 156,000.00 Div.

Recommended

Recommended

More Related Content

Similar to Problem 14-1A On January 1, 2014, Geffrey Corporation had the followi.pdf

Similar to Problem 14-1A On January 1, 2014, Geffrey Corporation had the followi.pdf (20)

More from ajayelectronics

More from ajayelectronics (9)

Recently uploaded

Recently uploaded (20)

Problem 14-1A On January 1, 2014, Geffrey Corporation had the followi.pdf

- 1. Problem 14-1A On January 1, 2014, Geffrey Corporation had the following stockholders' equity accounts Common Stock ($20 par value, 60,000 shares issued and outstanding) Paid-in Capital in Excess of Par-Common Stock Retained Earnings $1,200,000 200,000 600,000 During the year, the following transactions occurred. Declared a $1 cash dividend per share to stockholders of record on February 15, payable March 1 Paid the dividend declared in February Announced a 2-for-1 stock split. Prior to the split, the market price per share was $36 Declared a 10% stock dividend to stockholders of record on July 15, distributable July 31, On July 1, the market price of the stock was $13 per share Issued the shares for the stock dividend Declared a $0.50 per share dividend to stockholders of record on December 15, payable January 5, 2015 Determined that net income for the year was $350,000 Feb. 1 Mar. 1 Apr. 1 July 1 31 Dec. 1 31 Journalize the transactions and the closing entries for net income and dividends. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts. If no entry is required, select "No entry" for the account titles and enter 0 for the amounts.) Date Aocount Titles and Explanation Debit Credit Feb. 1 Mar. 1 Apr. 1 July 1 uly 31 Dec. 1 Dec. 31 (To close net income) (To close stock dividends) (To close cash dividends) Solution Journal Entries: Date Accounts / Explanations Debit Credit Feb. 1 Cash Dividend $ 60,000.00 Dividend Payable $ 60,000.00 (Being cash dividend declared = 60000 Shares * $1) Mar. 1 Dividend Payable $ 60,000.00 Cash $ 60,000.00 (Being cash dividend cash )

- 2. Apr. 1 No entry (New shares = 60000*2 = 120000 Shares @ $20/ 2 =$10 Par value) July. 1 Stock Dividend $ 156,000.00 Dividend Distributable $ 156,000.00 (Being Stock Dividend Declared = 120000 *10% = 12000 Shares*$13 ) July. 31 Dividend Distributable $ 156,000.00 Paid in capital in excess of par- Common Stock (156000-120000) $ 36,000.00 Common Stock (12000 Shares * $10) $ 120,000.00 (Being shares issues for dividend ) Note : total number of shares after Stock Div = 120000+12000 = 132000 Dec. 1 Cash Dividend $ 66,000.00 Dividend Payable $ 66,000.00 (Being cash dividend declared = 132000 Shares * $0.50) Dec. 31 Income Summary $ 350,000.00 Retained earnings $ 350,000.00 (Being net income closed) Retained earnings $ 126,000.00 Cash Dividend (60000+66000) $ 126,000.00 (Being cash dividend closed) Retained earnings

- 3. $ 156,000.00 Stock Dividend $ 156,000.00 (Being cash dividend closed) Journal Entries: Date Accounts / Explanations Debit Credit Feb. 1 Cash Dividend $ 60,000.00 Dividend Payable $ 60,000.00 (Being cash dividend declared = 60000 Shares * $1) Mar. 1 Dividend Payable $ 60,000.00 Cash $ 60,000.00 (Being cash dividend cash ) Apr. 1 No entry (New shares = 60000*2 = 120000 Shares @ $20/ 2 =$10 Par value) July. 1 Stock Dividend $ 156,000.00 Dividend Distributable $ 156,000.00 (Being Stock Dividend Declared = 120000 *10% = 12000 Shares*$13 ) July. 31 Dividend Distributable $ 156,000.00 Paid in capital in excess of par- Common Stock (156000-120000) $ 36,000.00 Common Stock (12000 Shares * $10)

- 4. $ 120,000.00 (Being shares issues for dividend ) Note : total number of shares after Stock Div = 120000+12000 = 132000 Dec. 1 Cash Dividend $ 66,000.00 Dividend Payable $ 66,000.00 (Being cash dividend declared = 132000 Shares * $0.50) Dec. 31 Income Summary $ 350,000.00 Retained earnings $ 350,000.00 (Being net income closed) Retained earnings $ 126,000.00 Cash Dividend (60000+66000) $ 126,000.00 (Being cash dividend closed) Retained earnings $ 156,000.00 Stock Dividend $ 156,000.00 (Being cash dividend closed)