Is the Fed really as dovish as markets think?

•

0 likes•240 views

Is the Fed really as dovish as markets think?

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (15)

Similar to Is the Fed really as dovish as markets think?

Similar to Is the Fed really as dovish as markets think? (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

Is the Fed really as dovish as markets think?

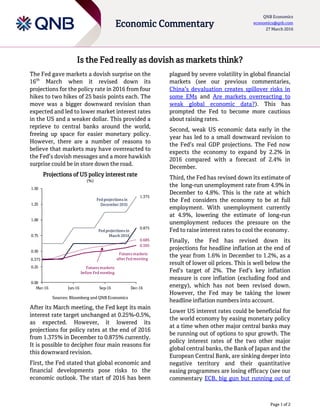

- 1. Page 1 of 2 Economic Commentary QNB Economics economics@qnb.com 27 March 2016 Is the Fed really as dovish as markets think? The Fed gave markets a dovish surprise on the 16th March when it revised down its projections for the policy rate in 2016 from four hikes to two hikes of 25 basis points each. The move was a bigger downward revision than expected and led to lower market interest rates in the US and a weaker dollar. This provided a reprieve to central banks around the world, freeing up space for easier monetary policy. However, there are a number of reasons to believe that markets may have overreacted to the Fed’s dovish messages and a more hawkish surprise could be in store down the road. Projections of US policy interest rate (%) Sources: Bloomberg and QNB Economics After its March meeting, the Fed kept its main interest rate target unchanged at 0.25%-0.5%, as expected. However, it lowered its projections for policy rates at the end of 2016 from 1.375% in December to 0.875% currently. It is possible to decipher four main reasons for this downward revision. First, the Fed stated that global economic and financial developments pose risks to the economic outlook. The start of 2016 has been plagued by severe volatility in global financial markets (see our previous commentaries, China’s devaluation creates spillover risks in some EMs and Are markets overreacting to weak global economic data?). This has prompted the Fed to become more cautious about raising rates. Second, weak US economic data early in the year has led to a small downward revision to the Fed’s real GDP projections. The Fed now expects the economy to expand by 2.2% in 2016 compared with a forecast of 2.4% in December. Third, the Fed has revised down its estimate of the long-run unemployment rate from 4.9% in December to 4.8%. This is the rate at which the Fed considers the economy to be at full employment. With unemployment currently at 4.9%, lowering the estimate of long-run unemployment reduces the pressure on the Fed to raise interest rates to cool the economy. Finally, the Fed has revised down its projections for headline inflation at the end of the year from 1.6% in December to 1.2%, as a result of lower oil prices. This is well below the Fed’s target of 2%. The Fed’s key inflation measure is core inflation (excluding food and energy), which has not been revised down. However, the Fed may be taking the lower headline inflation numbers into account. Lower US interest rates could be beneficial for the world economy by easing monetary policy at a time when other major central banks may be running out of options to spur growth. The policy interest rates of the two other major global central banks, the Bank of Japan and the European Central Bank, are sinking deeper into negative territory and their quantitative easing programmes are losing efficacy (see our commentary ECB, big gun but running out of 0.375 0.875 1.375 0.685 0.595 0.00 0.25 0.50 0.75 1.00 1.25 1.50 Mar-16 Jun-16 Sep-16 Dec-16 Fed projections in December 2015 Fed projections in March 2016 Futures markets after Fed meeting Futures markets before Fed meeting

- 2. Page 2 of 2 Economic Commentary QNB Economics economics@qnb.com 27 March 2016 ammunition?). In emerging markets, lower US interest rates and a weaker dollar provide more room for central banks to cut rates without instigating capital flight and weaker exchange rates. A number of emerging market central banks have already lowered rates since the Fed’s meeting, such as Bank Indonesia and, reportedly, the People’s Bank of China. However, the stimulus from easier monetary policy by a dovish Fed may not last. There are a number of reasons to believe that there are upside risks to the Fed’s central projection of two hikes this year. First, the global economy appears to be getting back on track after a rough start to the year and global financial markets have recovered (see our commentary Markets set the stage for Fed rate hikes). Second, the jobs market in the US remains strong and the economy could soon rise above full employment, increasing the likelihood that the Fed would raise interest rates. Third, the Fed’s projection of two hikes is based on the median of forecasts generated by the participants in Fed meetings. However, a significant proportion of participants still expect more than two hikes. Out of 17 participants, nine project two hikes this year, seven project more than two hikes and only one projects a single hike. This suggests that it would not take a significant improvement in US economic data to tip the Fed back towards a higher number of rate increases. Finally, the Fed’s forecasts for inflation could be too low. Core inflation unexpectedly rose to 1.7% in January from 1.5% in December, rapidly approaching the Fed’s 2% target. The Fed expects this measure of inflation to ease during 2016 and is forecasting 1.6%, in line with its projection in December 2015. However, markets and a number of commentators expect core inflation to remain persistently higher. Therefore, the market response to the dovish Fed may be overdone and markets could have set themselves up for a hawkish surprise down the line. As long as there are no more shocks to economic growth and global financial markets, more than two Fed rate hikes could still be on the cards this year, which could lead to a stronger dollar and tighter monetary policy in emerging markets. QNB Economics Team: Ziad Daoud Acting Head of Economics +974-4453-4642 Rory Fyfe* Senior Economist +974-4453-4643 Ehsan Khoman Economist +974-4453-4423 Hamda Al-Thani Economist +974-4453-4642 Rim Mesraoua Research Analyst +974-4453-4642 * Corresponding authors Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group.