Booking open Available Pune Call Girls Shivane 6297143586 Call Hot Indian Gi...

28 June Daily market report

1. Page 1 of 6

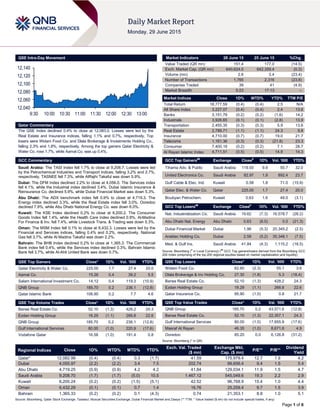

QSE Intra-Day Movement

Qatar Commentary

The QSE Index declined 0.4% to close at 12,083.0. Losses were led by the

Real Estate and Insurance indices, falling 1.1% and 0.7%, respectively. Top

losers were Widam Food Co. and Dlala Brokerage & Investments Holding Co.,

falling 2.3% and 1.8%, respectively. Among the top gainers Qatar Electricity &

Water Co. rose 1.7%, while Aamal Co. was up 0.4%.

GCC Commentary

Saudi Arabia: The TASI Index fell 1.7% to close at 9,208.7. Losses were led

by the Petrochemical Industries and Transport indices, falling 3.2% and 2.7%,

respectively. TASNEE fell 7.3%, while AlRajhi Takaful was down 5.9%.

Dubai: The DFM Index declined 2.2% to close at 4,056.0. The Services index

fell 4.1%, while the Industrial index declined 3.4%. Dubai Islamic Insurance &

Reinsurance Co. declined 5.9%, while Dubai Financial Market was down 5.3%.

Abu Dhabi: The ADX benchmark index fell 0.9% to close at 4,719.3. The

Energy index declined 3.3%, while the Real Estate index fell 3.0%. Ooredoo

declined 7.9%, while Abu Dhabi National Energy Co. was down 6.0%.

Kuwait: The KSE Index declined 0.2% to close at 6,200.2. The Consumer

Goods Index fell 1.4%, while the Health Care index declined 0.9%. Al-Madina

For Finance & Inv. fell 7.4%, while Livestock Trans. & Trading was down 5.3%.

Oman: The MSM Index fell 0.1% to close at 6,432.3. Losses were led by the

Financial and Services indices, falling 0.4% and 0.2%, respectively. National

Gas fell 3.7%, while Al Madina Takaful was down 2.2%.

Bahrain: The BHB Index declined 0.2% to close at 1,365.3. The Commercial

Bank index fell 0.4%, while the Services index declined 0.3%. Bahrain Islamic

Bank fell 3.7%, while Al-Ahli United Bank was down 0.7%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Electricity & Water Co. 225.00 1.7 27.4 20.0

Aamal Co. 15.26 0.4 39.2 5.5

Salam International Investment Co. 14.12 0.4 119.3 (10.9)

QNB Group 185.70 0.2 236.1 (12.8)

Qatar Islamic Bank 106.90 0.2 7.7 4.6

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Barwa Real Estate Co. 52.10 (1.3) 428.2 24.3

Ezdan Holding Group 18.29 (1.1) 266.8 22.6

QNB Group 185.70 0.2 236.1 (12.8)

Gulf International Services 80.00 (1.0) 220.9 (17.6)

Vodafone Qatar 16.58 (1.0) 191.4 0.8

Market Indicators 28 June 15 25 June 15 %Chg.

Value Traded (QR mn) 151.4 177.0 (14.5)

Exch. Market Cap. (QR mn) 640,624.0 642,359.4 (0.3)

Volume (mn) 2.6 3.4 (23.4)

Number of Transactions 1,765 2,316 (23.8)

Companies Traded 39 41 (4.9)

Market Breadth 5:23 17:13 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,777.59 (0.4) (0.4) 2.5 N/A

All Share Index 3,227.07 (0.4) (0.4) 2.4 13.6

Banks 3,151.79 (0.2) (0.2) (1.6) 14.2

Industrials 3,926.65 (0.1) (0.1) (2.8) 13.9

Transportation 2,455.35 (0.3) (0.3) 5.9 13.6

Real Estate 2,789.71 (1.1) (1.1) 24.3 9.8

Insurance 4,710.00 (0.7) (0.7) 19.0 21.7

Telecoms 1,161.36 (0.3) (0.3) (21.8) 23.3

Consumer 7,400.19 (0.2) (0.2) 7.1 28.7

Al Rayan Islamic Index 4,711.51 (0.5) (0.5) 14.9 14.3

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Tihama Adv. & Public Saudi Arabia 119.50 9.9 50.7 32.0

United Electronics Co. Saudi Arabia 82.97 1.9 892.4 23.7

Gulf Cable & Elec. Ind. Kuwait 0.58 1.8 71.0 (15.9)

Qatar Elec. & Water Co. Qatar 225.00 1.7 27.4 20.0

Boubyan Petrochem. Kuwait 0.63 1.6 49.0 (3.1)

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Nat. Industrialization Co. Saudi Arabia 19.62 (7.3) 16,578.7 (26.2)

Abu Dhabi Nat. Energy Abu Dhabi 0.63 (6.0) 0.5 (21.3)

Dubai Financial Market Dubai 1.96 (5.3) 20,345.2 (2.5)

Arabtec Holding Co. Dubai 2.58 (5.2) 35,348.1 (7.5)

Med. & Gulf Ins. Saudi Arabia 41.84 (4.3) 1,115.2 (16.5)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Widam Food Co. 62.60 (2.3) 55.1 3.6

Dlala Brokerage & Inv Holding Co. 27.30 (1.8) 5.3 (18.4)

Barwa Real Estate Co. 52.10 (1.3) 428.2 24.3

Ezdan Holding Group 18.29 (1.1) 266.8 22.6

Qatar Insurance Co. 95.90 (1.0) 0.8 21.7

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

QNB Group 185.70 0.2 43,571.6 (12.8)

Barwa Real Estate Co. 52.10 (1.3) 22,357.1 24.3

Gulf International Services 80.00 (1.0) 17,655.9 (17.6)

Masraf Al Rayan 46.35 (1.0) 8,671.6 4.9

Ooredoo 85.20 0.0 6,126.8 (31.2)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,082.99 (0.4) (0.4) 0.3 (1.7) 41.59 175,979.4 12.7 1.9 4.2

Dubai 4,055.97 (2.2) (2.2) 3.4 7.5 202.74 99,656.4 9.4 1.5 5.4

Abu Dhabi 4,719.25 (0.9) (0.9) 4.2 4.2 41.84 129,034.1 11.9 1.5 4.7

Saudi Arabia 9,208.70 (1.7) (1.7) (5.0) 10.5 1,467.12 545,049.6 19.3 2.2 2.9

Kuwait 6,200.24 (0.2) (0.2) (1.5) (5.1) 42.52 96,768.9 15.4 1.0 4.4

Oman 6,432.29 (0.1) (0.1) 0.7 1.4 16.76 25,259.4 9.7 1.5 3.9

Bahrain 1,365.33 (0.2) (0.2) 0.1 (4.3) 0.74 21,353.1 8.8 1.0 5.1

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,040

12,060

12,080

12,100

12,120

12,140

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QSE Index declined 0.4% to close at 12,083.0. The Real

Estate and Insurance indices led the losses. The index fell on the

back of selling pressure from Qatari and non-Qatari shareholders

despite buying support from GCC shareholders.

Widam Food Co. and Dlala Brokerage & Investments Holding

Co. were the top losers, falling 2.3% and 1.8%, respectively.

Among the top gainers Qatar Electricity & Water Co. rose 1.7%,

while Aamal Co. was up 0.4%.

Volume of shares traded on Sunday fell by 23.4% to 2.6mn from

3.4mn on Thursday. Further, as compared to the 30-day moving

average of 13.8mn, volume for the day was 81.3% lower. Barwa

Real Estate Co. and Ezdan Holding Group were the most active

stocks, contributing 16.6% and 10.4% to the total volume,

respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Ratings and Earnings

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

First Gulf Bank

(FGB)

Capital

Intelligence

Abu

Dhabi

FSR/LT FCR/ST

FCR/SR

A+/ A+/A1/2 A+/ A+/A1/2 – Stable –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC

– Local Currency)

Earnings Releases

Company Market Currency

Revenue

(mn) 2Q2015

% Change

YoY

Operating Profit

(mn) 2Q2015

% Change

YoY

Net Profit (mn)

2Q2015

% Change

YoY

Al Firdous Holdings* Dubai AED 19.2 16.2% – – -15.6 NA

Source: Company data, DFM, ADX, MSM (*FY2014-15 results)

News

Qatar

UDCD to disclose financials on July 15 – United

Development Company (UDCD) will announce the financial

reports for the period ending June 30, 2015 on July 15, 2015.

(QSE)

QEWS to announce financials on July 13 – Qatar Electricity

and Water Company (QEWS) will disclose the financial reports

for the period ending June 30, 2015 on July 13, 2015. (QSE)

QCB to issue T-bills worth QR4bn on July 1 – The Qatar

Central Bank (QCB) will issue new three-month treasury bills

worth QR2bn, along with six-month and nine-month T-bills worth

QR1bn each on July 1, 2015. (QCB)

MDPS: Qatar May trade surplus hits QR15.2bn – According

to statistics released by the Ministry of Development Planning &

Statistics (MDPS), the value of Qatar’s total exports amounted

to QR24.8bn in May 2015, a decrease of 38.9% YoY. However,

the total exports of goods increased by 4.7% MoM in May 2015.

On the other hand, the imports of goods in May 2015 amounted

to QR9.6bn, an increase of 10% YoY. However on a MoM basis,

imports decreased by 9.3%. The foreign merchandise trade

balance, which represents the difference between total exports

and imports, showed a surplus of QR15.2bn in May 2015, a

decrease of QR16.7bn or 52.3% YoY. However, the trade

balance increased by QR2.1bn or 16% MoM. According to a

QNA report, the YoY decrease in total exports was mainly due

to lower exports of petroleum gases and other gaseous

hydrocarbons, reaching QR15.9bn in May 2015, a decrease of

41.4%, petroleum oils & oils from bituminous minerals (crude)

reaching QR3.6bn, and petroleum oils & oils from bituminous

minerals (non crude) reaching QR1.1bn. In May 2015, Japan

was the top destination of Qatar’s exports with QR4.8bn, a

share of 19.3% of the total exports followed by South Korea with

QR4.4bn (17.8%) and India with QR3.1bn (12.5%). The US was

the leading country of origin in May 2015 of Qatar’s imports with

QR1.1bn, a share of 11.6% of the imports followed by China

with QR1.0bn (10%) and the UAE with QR0.9bn (9.6%). During

May 2015, motor cars & other passenger vehicles were at the

top of the imported commodities with QR0.7bn, showing an

increase of 41.8% YoY. Aircraft parts and helicopters stood at

the second place with QR0.5bn, showing an increase of 24.7%

while electrical apparatus for line telephony/telegraphy,

telephone sets, etc were at the third place. (Peninsula Qatar)

MDPS: Industrial sector PPI slid in April 2015 – The Ministry

of Development Planning & Statistics (MDPS) has released the

Monthly Producer Price Index (PPI) for the Industrial sector for

April 2015. The PPI for April 2015 is estimated at 62.2, recording

a decrease of 2.7% MoM and a decrease of 37.4% YoY. The

PPI covers goods relating to Mining (weight: 72.7%),

Manufacturing (weight: 26.8%) and Electricity & Water (weight:

0.5%). Compared with March 2015, the Mining sector PPI for

April 2015 showed a decline of 3.1%, primarily due to the falling

prices recorded in crude petroleum and natural gas. The PPI

declined by 41.5% YoY in April 2015. The Manufacturing sector

PPI decreased by 1.7% MoM in April 2015, while it showed a

decline of 26.8% on a YoY basis. The Electricity & Water PPI

decreased by 0.4% compared with March 2015, resulting from

the price fall in the Electricity sector by 0.6%, whereas it was

down 2.1% YoY. (QSA)

New sponsorship law makes headway – A committee of the

Advisory Council is to complete its review of the draft law

regulating the entry and residence of expatriates, more

commonly known as the new sponsorship law after a meeting

with HE the Minister of Labor and Social Affairs Dr. Abdullah bin

Saleh Al-Khulaifi on Monday. Qatar News Agency (QNA)

reported that the Internal and Foreign Affairs Committee at the

Overall Activity Buy %* Sell %* Net (QR)

Qatari 52.46% 71.36% (28,626,409.72)

GCC 33.04% 5.14% 42,247,901.01

Non-Qatari 14.50% 23.50% (13,621,491.29)

3. Page 3 of 6

Advisory Council discussed the draft law with HE the Prime

Minister and Minister of Interior Sheikh Abdullah bin Nasser bin

Khalifa Al-Thani at a session at the White Palace. (Gulf-

Times.com)

BMI Research: Qatar set for 40% growth in auto sales –

According to a recent report by BMI Research, Qatar is set to

witness over 40% growth in auto sales over the next four years

with total new vehicle sales expected to reach 143,774 units by

2019. The BMI report states that around 101,982 private

vehicles were registered in Qatar in 2014, representing an

annual increase of 8.7% and slightly ahead of BMI's predictions

of just over 6% growth. The BMI calculations were based on

figures from Qatar's Monthly Statistics book prepared by Qatar's

Ministry of Development Planning & Statistics (MDPS). BMI

expects a growth of 8.7% in overall new vehicle sales in 2015, to

reach over 110,000 units. (Gulf-Times.com)

VNI: Qatar ideally placed to boost digital businesses –

According to the 10th annual Cisco Visual Networking Index

(VNI) Forecast 2015 launched on Sunday, Qatar is ideally-

placed to advance digital businesses and society as total

internet users in the Middle East and Africa will grow 1.6-fold to

425mn by 2019 or 27% of the population, due to growing

demand for mobile devices, video and social networking. There

will be around 3.9bn global internet users by 2019, up from

2.8bn in 2014. In the Middle East and Africa, IP traffic will grow

six-fold by 2019, a compound annual growth rate of 44%.

(Peninsula Qatar)

Kahramaa opens new service center in Industrial Area – The

Qatar General Electricity & Water Corporation (Kahramaa) has

opened a new service center in Industrial Area. The center on

Street No. 100 in Zone No. 56 became operational on Sunday. It

is equipped with many facilities to help customers, including a

spacious waiting lounge. It will remain open from Sunday to

Thursday between 9am to 2pm during Ramadan. (Peninsula

Qatar)

Ashghal completes new FCC building – The Public Works

Authority (Ashghal) has completed the new building of the

Family Consultation Center (FCC) in the Al-Uqla area at a cost

of around QR76.147mn. The FCC offers the public various free

services, which cover different aspects of family life. Work on

the project had started in April 2013. The three-storey building

with a basement measuring 11,400,000 square meters (sqm)

overlooks two streets from the eastern and southern facades,

each 24 meters in width. The total space of the building is

19,283,000sqm. (Gulf-Times.com)

International

Greece shuts banks as expiring bailout sparks withdrawals

– Greece moved to avert a collapse of its financial system,

shutting lenders and imposing capital controls as of Monday, a

measure that will deepen the recession and risk driving the

nation toward an exit from the euro. The move to husband

resources followed the breakdown of aid talks with the

international creditors late on June 26 and the European Central

Bank’s (ECB) decision to freeze its lifeline to Greek banks.

Queues at ATMs and gas stations indicated how daily life was

about to be disrupted in the country. The ECB delivered its blow

on Sunday afternoon. The central bankers froze the ceiling on

the Emergency Liquidity Assistance to Greek lenders at just

below €89bn, refusing for the first time in 2015 to maintain a

buffer as deposits fled. A Greek government official said banks

will be closed for a week until July 6 with limits set on

withdrawals from cash machines. Meanwhile, International

Monetary Fund (IMF) Managing Director Christine Lagarde said

the IMF will be prevented by its rules from providing additional

financial assistance to Greece if they miss a June 30 payment.

(Bloomberg, Reuters)

Japan industrial production drops in May, denting recovery

– Japan’s industrial production dropped more than forecast in

May, sapping a recovery in the world’s third-largest economy.

The trade ministry said output fell 2.2% from April when it had

increased 1.2%. Retail sales rose 1.7% from the previous

month, more than estimated. According to a government survey

included in Monday’s output report, manufacturers plan to

increase production 1.5% in June and expand output 0.6% in

July. The rebound from recession last year is showing signs of

losing momentum at a time when global uncertainty is

increasing with a slowdown in China and financial turmoil in

Greece. (Bloomberg)

BIS: Low rates posing risk to global financial stability,

growth – The Switzerland-based Bank for International

Settlements (BIS) in its annual report said global interest rates

are too low and pose a rapidly growing risk to financial stability

and economic growth. The central bank said economic growth

across the world is uneven, debt burdens in many areas are

high and rising, and the explosion of credit growth shows

financial imbalances are building up again. It said a prolonged

period of ultra-low rates would further weaken the financial

sector and squeeze bank profitability, but a “normalization” of

borrowing costs would reverse the debt-fueled inflation of asset

prices and hit banks’ own loss-absorbing equity capital. The BIS

report added that central banks with inflation targets are at a

growing risk of policy errors because they are struggling to

adequately understand what drives inflation. The BIS further

stated that a decade of robust growth has broadly strengthened

emerging market economies but the associated asset price

booms and credit surges have increased their vulnerability to

crises. Its study estimated that government and non-financial

private sector debt was around 50% higher relative to GDP than

during the Asian crisis of 1997, primarily because private sector

borrowing in emerging economies has doubled in this period to

around 120% of GDP. (Reuters)

Chinese banks dominate global rankings for profits,

strength – According to a study by the Banker magazine,

Chinese banks are strengthening their position as the best

capitalized and biggest profit makers in the world. Chinese

banks filled the top four spots for profits across the industry in

2014 after making over $180bn between them in the magazine’s

annual rankings of profits and capital strength. Industrial and

Commercial Bank of China's (ICBC) $59.1bn profit in 2014

topped the rankings, ahead of China Construction Bank,

Agricultural Bank of China (Agbank) and Bank of China. The US

bank, Wells Fargo, ranked fifth with a $33.8bn profit followed by

JPMorgan and HSBC. ICBC also topped the ranking of the

strongest banks in the world for the third year, which is based on

the amount of capital held, in amount rather than as a ratio of

assets. China had four names in the top six strongest banks.

There were four US banks in the top 10 - JPMorgan was the

third and Bank of America was the fifth – including a British and

a Japanese bank. The best returns on capital were made by

banks in South America at an average of 26% followed by 24%

for African banks, 19% in Asia and 15.5% in North America.

Italian and Greek banks made the biggest losses in 2014.

(Reuters)

Regional

Al-Khodari wins two projects worth SR147mn – Abdullah A.

M. Al-Khodari Sons Company (Al-Khodari) has received two

letters of award from the Ministry of Transport to carry out

projects at a total value of SR147.3mn. The first project worth

4. Page 4 of 6

SR92.4mn will connect the Najran/ Sharura/ Wadia road within

24 months, while the second project worth SR54.9mn will

connect Assfan to Axial road in Jouf within 24 months. The

relevant financial impacts are expected to be seen in 3Q2015.

Meanwhile, Al-Khodari has informed its shareholders that it is

still in the process of preparing the application to approve the

capital increase through a rights issue in order to be submitted

to the Capital Market Authority (CMA) with its financial adviser

GIB Capital. The mentioned file is expected to be submitted to

the CMA within July 2015. (Tadawul)

Almarai reaches final settlement with Arabian Shield –

Almarai Company has reached a full and final settlement with

Arabian Shield Cooperative Insurance Company (ASICO)

regarding its property damage and business interruption claims

pertaining to the fire damage to Western Bakeries Plant 1 and 3

in Jeddah on October 9, 2014. The amount finally agreed

reached SR790mn, net of the policy excesses. The payment on

account of SR250mn received by Almarai on March 25, 2015,

will be offset against this final payment. This settlement will have

a neutral effect on the income statement at the end of June 30,

2015, as the net proceeds will be used to offset various partial

assets write-off and goodwill amortization. (Tadawul)

Mobily 2014 loss to rise by SR830mn after accounting

change – Etihad Etisalat Company (Mobily) said its 2014 loss

will increase by around SR830mn to SR1.745bn after revising

accounting policies following a probe. Mobily will change the

accounting for some of its contracts in response to a review by a

team appointed by the Capital Market Authority (CMA). Mobily

said it would reissue its financial statements for the year 2014

and 1Q2015 before releasing its 2Q2015 results. The company

said that in addition to increasing its 2014 loss, the changes

were expected to reduce its 1Q2015 loss by around SR207mn,

leading to a profit of SR8mn for the quarter. Separately,

Emirates Telecommunications Corporation, which owns 27.45%

of Mobily, said the operator’s revisions and provisions will cost it

about SR820mn. (GulfBase.com)

Saudi Ceramic updates on second sanitary ware plant

project – Saudi Ceramic Company announced that the second

sanitary ware plant project’s progress rate achieved is 95%, and

is expected to be completed by December 31, 2015. (Tadawul)

Saudi CMA updates on Alinma rights issue offering

applications – The Saudi Capital Market Authority (CMA)

clarified that Alinma Tokio Marine Company's application to

increase its share capital through rights issue will be presented

to the CMA’s board within two weeks from the date of

announcement. As of now, the CMA does not have any filed

capital increase applications through rights issue offering except

for the above mentioned application. (Tadawul)

WTC: Tourism contributed AED126.7bn to UAE GDP in 2014

– According to a report released by the World Travel Council

(WTC), the direct and indirect contribution of the tourism sector

to the UAE’s GDP amounted to AED126.7bn in 2014. The

sector’s contribution to the country’s GDP is projected to grow

by 5.1% in 2015 to AED133.12bn. As per the report, the sector’s

direct contribution to the GDP stood at AED61bn or 4.1% in

2014 and is set to grow to 4.9% in 2015. The report emphasizes

that the tourism industry has a more powerful impact than other

domains such as education, the chemicals industry and

agriculture. Furthermore, the data reveals that the tourism

sector’s contribution to the national GDP will grow by 2.7%

annually in the next ten years. In 2014, the number of direct jobs

in the travel and tourism sector hit 307,000, comprising 5.4% of

the total number of jobs in the country. They are expected to

grow by 5.4% in 2015 and at an annual rate of 2.6% to reach

420,000 jobs by 2025. (GulfBase.com)

Damac Properties launches Paramount Residences in

Dubai – Damac Properties has announced its latest hospitality

project in collaboration with Paramount Hotels & Resorts. The

company has launched Paramount Residences at the

Paramount Tower Hotel and Residences, an 826-key luxury

hotel and hotel residences tower on Sheikh Zayed Road. The

64-storey project has a private Paramount Pictures screening

room, a rooftop infinity pool, while each unit will have access to

a film library of more than 3,000 titles. The hotel residences,

situated on floors 38 to 64, will start at AED1,800 per square

foot. Units are available in one, two and three bedroom options,

plus there are two penthouses. The construction work on the

project is already underway, with completion scheduled for

Q32019. (DFM, GulfBase.com)

Dubai Holding announces promotion of top executives –

Dubai Holding has promoted Ahmad Bin Byat to Vice-Chairman

(VC) and Managing Director (MD) of the Group. Fadel Al Ali will

assume the role of Chief Executive Officer (CEO).

(GulfBase.com)

ADIA received record 1.87mn passengers in May 2015 – Abu

Dhabi International Airport (ADIA) has registered solid growth

across all key sectors in May 2015 with its passenger traffic

hitting 1.87mn, up 14.9% as compared to May 2014. The cargo

traffic also showed growth with a 9.8% increase in overall

tonnage to 73,476 as compared to 66,944 in May 2014. The

number of passengers to and from Italy has grown by 166.5%

as compared to May 2014 to over 50,000 passengers, as

Alitalia’s newly opened routes to Milan and Venice started to

take effect. In addition, passengers flying to and from the US

also registered similar increase with more than 106,000

passengers in May 2015, translating into 49% growth in traffic

as compared to May 2014. In terms of passenger numbers,

India topped the list in May 2015 with over 305,000 passengers

entering the UAE capital, up 58.6% as compared to May 2014.

(GulfBase.com)

ADS Securities, Anoa Capital acting as lead managers for

RNTS Media’s €150mn bond – Abu Dhabi’s ADS Securities

and Anoa Capital are acting as joint lead managers and

bookrunners for Germany-based RNTS Media’s €150mn senior,

unsecured convertible bond offering. The bonds will be listed on

the Open Market (Freiverkehr) of the Frankfurt Stock Exchange.

(GulfBase.com)

MCDC deposits unclaimed dividend of Al Batinah, Al

Suwadi – Al Batinah Power Company and Al Suwadi Power

Company have informed their respective shareholders that

Muscat Clearing & Depository Company SAOC (MCDC) has

deposited the unclaimed dividends, whose cutoff date was

December 1, 2014 with the Capital Market Authority (investors’

trust funds). Shareholders of both the company who have still

not claimed their dividends, are requested to approach MCDC.

(MSM)

Meezan Bank to acquire HBO’s Pakistan operations –

Meezan Bank has signed an agreement to acquire Pakistan

operations of HSBC Bank Oman (HBO). HBO’s operations in

Pakistan consist of one branch and gross assets of Pakistan

rupees 4.1bn at the end of 1Q2015. The acquisition is expected

to materialize in 2H2015, subject to regulatory approvals. HBO,

which was formed after merging Oman International Bank with

HSBC’s Oman operations, had decided in 2012 to sell off its

India and Pakistan operations. (GulfBase.com)

5. Page 5 of 6

Investcorp appoints CFO – Bahrain-based Investcorp has

appointed Tony Robinson as its Chief Financial Officer (CFO),

with effect from July 1, 2015. The current CFO Rishi Kapoor will

assume responsibility as Co-Chief Executive Officer (CEO) of

Investcorp on July 1, 2015, together with Mohammed Al-

Shroogi, who is currently President, GulfBusiness. The pair is

replacing Nemir Kirdar, who led Investcorp for more than 30

years but will retire from his positions as Executive Chairman

and CEO on June 30, 2015. (Bahrain Bourse)

GFH Financial partners with Adani for Mumbai Economic

Zone – GFH Financial Group has entered into an agreement

with India’s Adani Group for developing an economic

development zone in Mumbai. Under the terms of the

agreement, GFH’s unit Energy City Navi Mumbai (ECNM) and

Adani Group will work together in creating the master plan for

the lands of Phases II and III of the project, which will offer world

class business infrastructure for local and international services,

IT and energy companies. GFH’s ECNM and Mumbai IT and

Telecom City (MITTC) - are two core components of the Mumbai

Economic Development Zone (MEDZ). Following the requisite

approval of the master plan, Adani Group will develop the core

infrastructure on these lands and will also commence the pre-

sales and construction works on the site. Investors will receive a

15% revenue share from sales made by Adani Group on the

development on these lands and less local taxes. Around

$45mn has been received as part of the exit payments from the

developer, where GFH owns more than 6% of the total equity in

ECNM.(Bloomberg)

6. Contacts

Saugata Sarkar Sahbi Kasraoui QNB Financial Services SPC

Head of Research Head of HNI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 PO Box 24025

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

May-11 May-12 May-13 May-14 May-15

QSE Index S&P Pan Arab S&P GCC

(1.7%)

(0.4%)

(0.2%) (0.2%) (0.1%)

(0.9%)

(2.2%)

(4.0%)

(3.0%)

(2.0%)

(1.0%)

0.0%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,175.55 0.2 (2.1) (0.8) MSCI World Index 1,776.22 (0.3) 0.1 3.9

Silver/Ounce 15.80 (0.4) (1.9) 0.6 DJ Industrial 17,946.68 0.3 (0.4) 0.7

Crude Oil (Brent)/Barrel (FM

Future)

63.26 0.1 0.4 10.3 S&P 500 2,101.49 (0.0) (0.4) 2.1

Crude Oil (WTI)/Barrel (FM

Future)

59.63 (0.1) 0.0 11.9 NASDAQ 100 5,080.51 (0.6) (0.7) 7.3

Natural Gas (Henry

Hub)/MMBtu

2.77 (0.8) (1.5) (7.6) STOXX 600 396.85 (0.3) 1.2 6.8

LPG Propane (Arab Gulf)/Ton 41.12 1.8 17.5 (16.1) DAX 11,492.43 (0.3) 2.4 7.6

LPG Butane (Arab Gulf)/Ton 56.25 3.2 19.4 (14.1) FTSE 100 6,753.70 (0.8) (0.2) 3.9

Euro 1.12 (0.3) (1.6) (7.7) CAC 40 5,059.17 (0.1) 3.3 9.2

Yen 123.85 0.2 0.9 3.4 Nikkei 20,706.15 (0.5) 1.6 14.4

GBP 1.57 (0.0) (0.9) 1.1 MSCI EM 980.63 (0.8) 0.6 2.5

CHF 1.07 0.4 (1.6) 6.6 SHANGHAI SE Composite 4,192.87 (7.4) (6.4) 29.6

AUD 0.77 (1.1) (1.5) (6.4) HANG SENG 26,663.87 (1.8) (0.4) 13.0

USD Index 95.47 0.3 1.5 5.8 BSE SENSEX 27,811.84 (0.4) 1.6 0.6

RUB 54.81 0.2 1.4 (9.8) Bovespa 54,016.97 1.3 (0.9) (8.5)

BRL 0.32 (0.0) (1.0) (15.3) RTS 943.01 0.2 (2.5) 19.3

141.5

119.6

116.1