1. Page 1 of 5

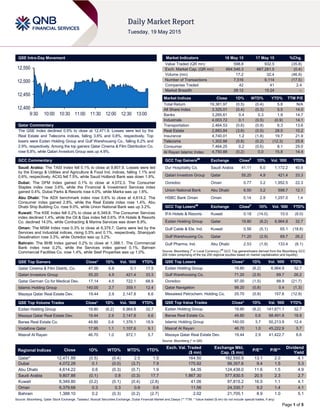

QSE Intra-Day Movement

Qatar Commentary

The QSE Index declined 0.5% to close at 12,471.9. Losses were led by the

Real Estate and Telecoms indices, falling 3.6% and 0.8%, respectively. Top

losers were Ezdan Holding Group and Gulf Warehousing Co., falling 6.2% and

2.9%, respectively. Among the top gainers Qatar Cinema & Film Distribution Co.

rose 6.8%, while Qatari Investors Group was up 4.9%.

GCC Commentary

Saudi Arabia: The TASI Index fell 0.1% to close at 9,807.9. Losses were led

by the Energy & Utilities and Agriculture & Food Ind. indices, falling 1.1% and

0.6%, respectively. ACIG fell 7.5%, while Saudi Hollandi Bank was down 1.9%.

Dubai: The DFM Index gained 0.1% to close at 4,072.3. The Consumer

Staples index rose 3.6%, while the Financial & Investment Services index

gained 0.4%. Dubai Parks & Resorts rose 4.0%, while Marka was up 1.6%.

Abu Dhabi: The ADX benchmark index rose 0.6% to close at 4,614.2. The

Consumer index gained 2.8%, while the Real Estate index rose 1.4%. Abu

Dhabi Ship Building Co. rose 9.0%, while Union National Bank was up 3.2%.

Kuwait: The KSE Index fell 0.2% to close at 6,349.8. The Consumer Services

index declined 1.4%, while the Oil & Gas index fell 0.6%. IFA Hotels & Resorts

Co. declined 14.0%, while Contracting & Marine Services was down 8.9%.

Oman: The MSM Index rose 0.3% to close at 6,379.7. Gains were led by the

Services and Industrial indices, rising 0.5% and 0.1%, respectively. Sharqiyah

Desalination rose 3.3%, while Ooredoo was up 3.2%.

Bahrain: The BHB Index gained 0.2% to close at 1,388.1. The Commercial

Bank index rose 0.2%, while the Services index gained 0.1%. Bahrain

Commercial Facilities Co. rose 1.4%, while Seef Properties was up 1.0%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Cinema & Film Distrib. Co. 47.00 6.8 0.1 17.5

Qatari Investors Group 55.20 4.9 421.4 33.3

Qatar German Co for Medical Dev. 17.14 4.5 722.1 68.9

Islamic Holding Group 140.00 3.7 359.1 12.4

Mazaya Qatar Real Estate Dev. 19.44 2.9 2,147.8 6.6

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 19.80 (6.2) 6,964.8 32.7

Mazaya Qatar Real Estate Dev. 19.44 2.9 2,147.8 6.6

Barwa Real Estate Co. 49.80 0.6 1,376.1 18.9

Vodafone Qatar 17.95 1.1 1,107.6 9.1

Masraf Al Rayan 46.70 1.0 972.1 5.7

Market Indicators 18 May 15 17 May 15 %Chg.

Value Traded (QR mn) 598.8 932.5 (35.8)

Exch. Market Cap. (QR mn) 664,546.3 667,281.5 (0.4)

Volume (mn) 17.2 32.4 (46.9)

Number of Transactions 7,516 9,114 (17.5)

Companies Traded 42 41 2.4

Market Breadth 28:12 15:24 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,381.97 (0.5) (0.4) 5.8 N/A

All Share Index 3,325.01 (0.4) (0.3) 5.5 14.0

Banks 3,265.61 0.4 0.3 1.9 14.7

Industrials 4,003.72 0.1 (0.5) (0.9) 14.1

Transportation 2,464.53 (0.6) (0.9) 6.3 13.6

Real Estate 2,883.84 (3.6) (0.5) 28.5 10.2

Insurance 4,740.01 1.2 (1.8) 19.7 21.9

Telecoms 1,302.88 (0.8) (0.2) (12.3) 25.8

Consumer 7,464.25 0.2 (0.6) 8.1 29.0

Al Rayan Islamic Index 4,750.88 (0.2) 0.0 15.8 14.4

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Dur Hospitality Co. Saudi Arabia 41.11 6.0 1,172.2 40.8

Qatari Investors Group Qatar 55.20 4.9 421.4 33.3

Ooredoo Oman 0.77 3.2 1,952.5 22.3

Union National Bank Abu Dhabi 6.50 3.2 598.7 12.1

HSBC Bank Oman Oman 0.14 2.9 1,257.0 1.4

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

IFA Hotels & Resorts Kuwait 0.18 (14.0) 10.0 (8.0)

Ezdan Holding Group Qatar 19.80 (6.2) 6,964.8 32.7

Gulf Cable & Ele. Ind. Kuwait 0.56 (5.1) 65.1 (18.8)

Gulf Warehousing Co. Qatar 71.20 (2.9) 69.7 26.2

Gulf Pharma. Ind. Abu Dhabi 2.53 (1.9) 133.4 (8.1)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 19.80 (6.2) 6,964.8 32.7

Gulf Warehousing Co. 71.20 (2.9) 69.7 26.2

Ooredoo 97.00 (1.5) 88.9 (21.7)

Qatar Navigation 98.20 (0.8) 0.4 (1.3)

Mesaieed Petrochem. Holding Co. 25.70 (0.8) 157.6 (12.9)

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Ezdan Holding Group 19.80 (6.2) 141,671.1 32.7

Barwa Real Estate Co. 49.80 0.6 68,491.8 18.9

Islamic Holding Group 140.00 3.7 50,213.9 12.4

Masraf Al Rayan 46.70 1.0 45,222.9 5.7

Mazaya Qatar Real Estate Dev. 19.44 2.9 41,422.7 6.6

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,471.89 (0.5) (0.4) 2.5 1.5 164.50 182,550.9 13.1 2.0 4.1

Dubai 4,072.28 0.1 (0.0) (3.7) 7.9 175.92 99,357.6 9.4 1.5 5.3

Abu Dhabi 4,614.22 0.6 (0.3) (0.7) 1.9 64.35 124,438.0 11.6 1.5 4.9

Saudi Arabia 9,807.88 (0.1) 0.8 (0.3) 17.7 1,867.30 577,830.5 20.5 2.3 2.7

Kuwait 6,349.80 (0.2) (0.1) (0.4) (2.8) 41.06 97,815.2 16.5 1.1 4.1

Oman 6,379.68 0.3 0.3 0.9 0.6 11.56 24,330.7 9.2 1.4 4.1

Bahrain 1,388.10 0.2 (0.3) (0.2) (2.7) 2.02 21,705.1 8.9 1.0 5.1

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,400

12,450

12,500

12,550

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 5

Qatar Market Commentary

The QSE Index declined 0.5% to close at 12,471.9. The Real

Estate and Telecoms indices led the losses. The index fell on the

back of selling pressure from Qatari and GCC shareholders

despite buying support from non-Qatari shareholders.

Ezdan Holding Group and Gulf Warehousing Co. were the top

losers, falling 6.2% and 2.9%, respectively. Among the top

gainers Qatar Cinema & Film Distribution Co. rose 6.8%, while

Qatari Investors Group was up 4.9%.

Volume of shares traded on Monday fell by 46.9% to 17.2mn

from 32.4mn on Sunday. However, as compared to the 30-day

moving average of 11.3mn, volume for the day was 51.5%

higher. Ezdan Holding Group and Mazaya Qatar Real Estate

Development were the most active stocks, contributing 40.5%

and 12.5% to the total volume, respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Global Economic Data

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

05/18 US NAHB NAHB Housing Market Index May 54.0 57.0 56.0

05/18 UK Rightmove Rightmove House Prices MoM May -0.10% – 1.60%

05/18 UK Rightmove Rightmove House Prices YoY May 2.50% – 4.70%

05/18 Italy ISTAT Trade Balance Total March 4,060M – 3,536M

05/18 Italy ISTAT Trade Balance EU March 487M – 689M

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QIBK to boost capital via bond sales; QIB-UK to offer

investment solutions for London properties – Qatar Islamic

Bank’s (QIBK) CFO, Gourang Hemani said that the bank

expects to issue a Tier 1 capital-boosting bond between 2Q2015

and 3Q2015 to help boost core capital and comply with Basel III

banking standards. The bond will have a perpetual tenor. The

issue will most likely be through a private placement within

Qatar. The bank had received shareholder’s approval to issue

up to QR5.0bn to increase its core capital in February 2015.

Meanwhile, QIBK’s wholly-owned subsidiary, QIB-UK is looking

to develop suitable financial solutions for Qatari nationals, which

meets their investment and financing needs in the UK as

London is increasingly becoming a favorite destination for

business, investment, educational or personal purposes. QIB-

UK is well positioned to support interested customers throughout

the process of identifying real estate opportunities, getting

access to exclusive deals, obtaining the required financing and

concluding the deal in an efficient manner. (GulfBase.com,

Peninsula Qatar)

QATI to issue insurance for up to three years for new cars –

Qatar Insurance Company (QATI) will support the latest

amendment to the Traffic Law by issuing insurance for up to two

or three years for newly-registered cars. QATI’s new facility is

applicable for both the Comprehensive and Third Party Liability

covers and would be valid for up to two or three years from the

date of registration of the new car. The initiative is aligned to the

latest amendment to Traffic Law No. 19 of 2007, which

stipulates that new cars can now be registered for three years.

(Gulf-Times.com)

MCCS BoD to review operations – Mannai Corporation’s

(MCCS) board of directors will hold a meeting on June 9, 2015

to review the operations of the company. (QSE)

New law to speed up clearance at ports – The Advisory

Council has approved a draft legislation seeking to reduce the

time period after which goods lying unclaimed or uncared for at

the ports are auctioned. According to amendments being made

to the existing law, the current time period for auctioning

unclaimed goods is likely to be reduced from six months to two

months. The rule would apply to both, goods that are imported

and lie unclaimed in the precincts of the ports or goods that are

meant for export/re-export but are not shipped within the

specified time. The draft legislation also suggests that

perishable goods that lie unclaimed or unshipped at the ports for

long periods and can become stale or can damage other goods

at the ports can also be auctioned after thorough inspections.

Moreover, the present law authorizes the Cabinet to waive

certain fee levied on ships or importers. In the amended law this

authority is being vested with the Minister of Transport &

Communications. (Peninsula Qatar)

Al Ruwais port to be opened in 3 months – According to

officials from the Ministry of Environment’s Fisheries

Department, the Al Ruwais port will be opened within three

months after finalizing the development works. The officials

stated that the work is underway to open the port, which will

include storehouses of different sizes for fishermen, a

restaurant, toilets and a yard to prepare fishing gear. Meanwhile,

talks are continuing between the Fisheries Department and

Public Works Authority (Ashghal) to expand and develop the

ports at Al Wakrah and Al Khor and equip them with the required

infrastructure. (Gulf-Times.com)

S&P upgrades ratings of DBAC, outlook stable – Standard &

Poor’s Ratings Services has raised its long-term counterparty

credit and insurer financial strength ratings of Doha Bank

Assurance Company (DBAC) to ‘BBB+’ from ‘BBB’. The outlook

is stable. According to S&P, the upgrade reflects DBAC’s

progress in improving its risk management framework while its

enterprise risk management is appraised to be adequate now as

Overall Activity Buy %* Sell %* Net (QR)

Qatari 52.51% 66.52% (83,844,191.34)

GCC 3.94% 5.13% (7,163,167.24)

Non-Qatari 43.55% 28.36% 91,007,358.58

3. Page 3 of 5

the company has successfully embedded sufficient underwriting

controls. Also, S&P assessed DBAC’s business risk profile as

fair, constrained by its modest size and market share within the

Qatari market. DBAC sources roughly half of its gross premiums

from its parent Doha Bank (DHBK). S&P expects that the

premium income sourced through DHBK will increase over the

medium-term, but that the overall premium growth will remain

modest, at around 2% in 2015. DBAC’s market share was below

2% in terms of gross written premium in 2014. (Peninsula Qatar)

International

NAHB: US home builder sentiment slips in May – The

National Association of Home Builders (NAHB) said that the US

homebuilder sentiment fell in May but still showed that more

builders view the market conditions as favorable. The

NAHB/Wells Fargo Housing Market Index fell to 54 from 56 in

April. Readings above 50 indicate more builders view the market

conditions as favorable than poor. The index has not been

below 50 since June 2014. (Reuters)

FM: Greece nears debt deal in May – Greek Finance Minister

(FM), Yanis Varoufakis said that Greece is near a cash-for-

reforms deal with its eurozone partners and the International

Monetary Fund (IMF) that would help it meet debt repayments in

June 2015, as worries persist over a possible bankruptcy.

Greece faces payments of about €1.5bn to the IMF in June and

€6.7bn to redeem government bonds that are held by the

European Central Bank and mature in July and August. Athens

wants a deal to include a debt restructuring, a lower target for

the primary surplus to take in more than it spends apart from

debt interest payments, and a pledge to make no further cuts to

pensions or wages. (Reuters)

Brazil prepares new tax hikes to meet fiscal goal – According

to sources, the Brazilian government plans a new round of tax

hikes to meet its fiscal goal in 2015 despite the recent efforts to

limit public expenditures. President Dilma Rousseff has agreed

to increase the PIS and Cofins taxes after the administration

announces a spending freeze of up to $26.58bn later this week.

The PIS is a mandatory employer contribution to a savings fund,

while the Cofins is a levy that helps finance the social security

system. The government is also considering raising the so-

called CSLL tax on Brazilian banks to make up for the loss in

revenues resulting from Congress' recent decision to water

down austerity measures. The CSLL is a levy on the profits of

companies to contribute to the social security system. (Reuters)

China releases guidelines for economic reform priorities in

2015 – China's cabinet has announced guidelines on Monday

for reform priorities in 2015, ranging from streamlining

administrative procedures to boosting the yuan's global role, as

Beijing steps up efforts to open up the country's capital markets.

The State Council approved the guidelines drafted by the

National Development & Reform Commission (NDRC) for this

year's action plan, calling 2015 "a crucial year for deepening

reform." The specific areas targeted for reforms included state

enterprises, taxation, the Shenzhen Hong Kong stock connect,

deposit rates, the initial public offering system, and boosting the

global status of the yuan among others. Meanwhile, NDRC said

that it has approved around yuan 250bn of railway and subway

projects, in a bid to bolster the slowing economy. (Reuters)

UNCTAD: Developing Asia becomes main driver of global

FDI – According to a survey conducted by the United Nations

(UN) trade and economic thinktank UNCTAD, developing

countries in Asia became the world's largest source of foreign

direct investment (FDI) in 2014, overtaking the US which

remained the biggest single investor country. Developing Asian

countries had invested $440bn abroad in 2014, eclipsing North

American outward investment of $390bn and $286bn coming

from Europe. Global FDI outflows were estimated at $1.341tn in

2014, reflecting an increase of 6.2% from 2013. Most of the FDI

coming from developing countries went into mergers and

acquisitions, whereas 81% of the FDI from developed countries

consisted of earnings reinvested in existing investments. US

firms had invested $337bn in 2014, 3% more than in 2013. Hong

Kong and China were the second and third largest investors,

spending $150bn and $116bn respectively. (Reuters)

Regional

Gartner: MEA IT infrastructure spending to reach $3.48bn in

2015 – According to Gartner, IT infrastructure spending in the

Middle East & Africa (MEA) is forecasted to reach $3.48bn in

2015, reflecting an increase of 0.9% YoY. Gartner’s Research

Vice President, Mary Mesaglio, said that due to the continued

low oil prices globally, the macroeconomic situation in the Gulf

countries is creating increased economic pressure; this may

negatively impact IT spending, including infrastructure projects

in 2015. (GulfBase.com)

Al-Khodari renews SR290.13mn Islamic credit facility

agreement with GIB – Abdullah A. M. Al-Khodari Sons

Company (Al-Khodari) has renewed its Islamic credit facilities

amounting to SR290.13mn with the Gulf International Bank

(GIB). These credit facilities are to provide bonding

commitments and fund the working capital and capital

expenditure requirements of the projects. Moreover, 36% of the

facilities are funded under Murabaha modes of financing,

whereas 64% limits are for multi-purpose bonds and

documentary credits. The credit limits’ tenure ranges from 6-48

months, depending upon the purpose of their utilization. The

Murabaha facilities are to be liquidated in quarterly and semi-

annual installments of various values. They are secured by

promissory notes and assignment of the contract proceeds of

the financed projects. (Tadawul)

AATSC AGM approves SR3.67bn contracts with SATORP –

Arabian Aramco Total Services Company’s (AATSC) ordinary

general assembly meeting (AGM) has approved the contracts

(Sukuk) with a current amount of SR3.67bn between the AATSC

and Saudi Aramco Total Refining and Petrochemical Company

(SATORP), and their renewal for 2016. (Tadawul)

SABB appoints new COO – The Saudi British Bank (SABB)

has appointed Saad Abdulaziz Alkhalb as its Chief Operating

Officer (COO) effective May 1, 2015. (GulfBase.com)

PetroRabigh restarts vacuum distillation unit – Rabigh

Refining & Petrochemical Company (PetroRabigh) has restarted

the vacuum distillation unit (VDU) after unscheduled

maintenance at its oil refinery that produces 400,000 barrels per

day. The maintenance will cost the company around SR100mn,

which will be reflected in its 2Q2015 financial results.

(GulfBase.com)

JODI: KSA oil exports hit highest level since 2003 –

According to Joint Organisations Data Initiative (JODI), Saudi

Arabia increased its oil exports in March 2015 to the highest

level since 2003. The Kingdom’s oil exports were 7.9mn barrels

per day in (b/d) March 2015, reflecting an increase of 10% YoY,

despite rising domestic demand. The output hit 10.3mn b/d, the

highest level reported by JODI since the records began in 2002.

However, the overall exports in 1Q2015, including the large

spike in March 2015, were up by only 1.5% YoY.

(GulfBase.com)

Al Othaim agrees to reduce stake in Mueen to 68% –

Abdullah Al Othaim Markets Company (Al Othaim) has agreed,

with the founding shareholders of Mueen Recruitment Company

4. Page 4 of 5

(Mueen), to reduce its stake to 68%, whereas the remaining

shares will be allocated to the other founding shareholders.

Mueen will be engaged in manpower recruitment activities and

providing household workers to the public and private sectors. Al

Othaim had signed an agreement with other shareholders to co-

found Mueen as a Saudi closed joint stock company (under

establishment) with SR100mn share capital. (Tadawul)

Amlak Finance launches 'Istithmari' property finance –

Dubai-based Amlak Finance has launched its ‘Istithmari’ finance

product. Istithmari caters to investors in ready residential and

commercial properties. It comes with a built-in property

management services package and advisory assistance.

Moreover, Istithmari is the first-of-its-kind ‘Property Finance’

product in the region. (Zawya)

Ajman Bank begins transacting on Nasdaq Dubai Islamic

platform – Ajman Bank has begun transacting on the Nasdaq

Dubai Murabaha platform, which facilitates the provision of

streamlined Shari'ah-compliant financing services. The Nasdaq

Dubai Murabaha platform has brought significant enhancements

to the retail and institutional Murabaha financing since its official

launch in April 2014. It has completed over AED46.5bn worth of

transactions till date. (GulfBase.com)

EMCAP closes $235mn term loan facility for FirstRand

Bank, ENBD lists $951mn of bonds on Nasdaq Dubai –

Emirates NBD Capital Limited (EMCAP) has announced the

successful closure and signing of a $235mn term loan facility for

FirstRand Bank Limited (FRB). Launched at $125mn, the two-

year facility was oversubscribed to close at $235mn with the

participation of nine institutions from the GCC region.

Meanwhile, Emirates NBD (ENBD) has listed $951mn of bonds

on Nasdaq Dubai, reflecting the bank’s ongoing expansion as a

leading regional financial institution. (GulfBase.com)

ICBC Dubai branch narrows price guidance for benchmark

5-yr bond issue – Industrial & Commercial Bank of China

(ICBC) has revised the price guidance for a benchmark five-year

debut bond from its Dubai branch, which is expected to price

later on May 18, 2015. The bank has set the final price guidance

at 120 basis points over the US Treasuries. The deal, rated A1

by Moody's, has attracted orders totaling to more than $3.5bn

from investors, till date. ICBC has picked Citigroup, Emirates

NBD, National Bank of Abu Dhabi, alongside itself, to arrange

the transaction. (Reuters)

DIB picks arrangers for potential dollar Sukuk – Dubai

Islamic Bank (DIB) has picked six banks to arrange fixed income

investor meetings from May 21, 2015 for a potential benchmark

size, US dollar-denominated senior Sukuk issue. DIB has

mandated that First Gulf Bank, HSBC, Maybank, National Bank

of Abu Dhabi, Standard Chartered Bank, along with itself, would

arrange the meetings in Asia and Europe. The offer will be

under DIB’s $2.5bn Sukuk program, and is subject to market

conditions. (GulfBase.com)

Falling oil prices not to impact FGB consumer business –

First Gulf Bank’s (FGB) Executive Vice President, Girish Advani

said that falling oil prices are not expected to impact the

consumer banking sector at FGB, with the bank set to see

continued growth. He added that the continued economic growth

in the UAE meant that fluctuating prices were not causing much

of an impact on the consumer side. (GulfBase.com)

KFH may sell properties, plans to cut jobs – Kuwait Finance

House (KFH) may sell some of its properties in 2015. The bank

may auction the properties or offer them to be run by other

operators, depending on the market conditions. Further, KFH

also plans to cut jobs as part of its restructuring plan, which

would eliminate some positions. The bank is restructuring

activities ahead of a planned divestment by its largest

shareholder, the Kuwait Investment Authority. (Reuters)

Kuwait OPEC Governor: Global crude oil prices not

expected to fall in 2H2015 – Kuwait’s OPEC Governor, Nawal

Al-Fuzaia said that global crude oil prices are not expected to

fall in 2H2015, unless there was a sudden development in the

market like supply disruption or an unexpected growth in the

supplies from other producers outside OPEC. He said that

OPEC production had not increased by more than 200,000 to

400,000 barrels per day above its 30mn barrels per day cap

since 2011. (Reuters)

Bank Nizwa drops UFC merger plan – Bank Nizwa has

withdrawn its proposal for a merger with United Finance

Company (UFC), after the latter received rival offers and invited

all suitors to enter a formal bidding process. (MSM)

NCSI: Oman’s crude exports up 10.2% YoY in 1Q2015 –

According to the National Centre for Statistics & Information

(NCSI), Oman's crude oil exports surged by 10.2% YoY to

78.39mn barrels in 1Q2015. However, the average price of

Oman crude in the international market dipped by 41.5% YoY to

$61.99 per barrel in 1Q2015. Meanwhile, the country's total

crude oil and condensate production grew marginally by 1.8%

YoY to 86.86mn barrels (or 965,000 barrels per day) in 1Q2015.

Oman's ability to increase spending by 4.5% in 2015 would

depend on growth in crude oil prices. In its 2015 budget plan,

revenues were projected at OMR11.6bn, leaving a budget deficit

of OMR2.5bn – Oman's largest fiscal gap since at least 1990.

(GulfBase.com)

GFH denies incurring material operating losses by ECNM &

MITTIC – Gulf Finance house (GFH) has denied that its units

Energy City Navi Mumbai (ECNM) and Mumbai IT & Telecom

Technology Investment Company (MITTIC) have suffered any

material operating losses. GFH stated that any losses incurred

by ECNM and MITTIC are limited to changes in fair market

value and foreign exchange rate for local currency. Meanwhile,

GFH said that it did not receive any notices from any official

authorities inside or outside of Kuwait concerning lawsuits filed

against the group. GFH’s current shareholding in both projects

exceeds 6%, which is above its initial investment when the

projects were launched in 2007. The previous news reports

claimed that a number of Kuwaiti investors have filed lawsuits

against a Kuwaiti investment company and GFH regarding

ECNM and MITTIC. (Bahrain Bourse)

Cluttons: Weak oil prices may hurt Bahrain real estate

market – Property consultant Cluttons, in its 'Spring 2015

Bahrain Property Market Outlook', said that the Bahrain

residential market is at high risk of losing its growth momentum

over weak oil prices. The market is likely to see declines toward

the end of 2015 as demand starts to wane. Cluttons said rents

and values across the residential market are yet to see a

notable impact, but low oil prices are expected to further

undermine the economic growth, which slowed to 4% in 2014,

from 4.9% in 2013. The report said, unlike the residential lettings

market, the outlook for the sales market is stable as a result of

the recent policy announcements designed to bolster residential

investor sentiment over the short to medium-term.

(GulfBase.com)

5. Contacts

Saugata Sarkar Sahbi Kasraoui QNB Financial Services SPC

Head of Research Head of HNI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 PO Box 24025

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Apr-11 Apr-12 Apr-13 Apr-14 Apr-15

QSE Index S&P Pan Arab S&P GCC

(0.1%)

(0.5%)

(0.2%)

0.2%

0.3%

0.6%

0.1%

(0.8%)

(0.4%)

0.0%

0.4%

0.8%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,225.52 0.1 0.1 3.4 MSCI World Index 1,808.73 0.1 0.1 5.8

Silver/Ounce 17.73 1.3 1.3 12.9 DJ Industrial 18,298.88 0.1 0.1 2.7

Crude Oil (Brent)/Barrel (FM

Future)

66.27 (0.8) (0.8) 15.6 S&P 500 2,129.20 0.3 0.3 3.4

Crude Oil (WTI)/Barrel (FM

Future)

59.43 (0.4) (0.4) 11.6 NASDAQ 100 5,078.44 0.6 0.6 7.2

Natural Gas (Henry

Hub)/MMBtu

3.01 1.7 1.7 0.5 STOXX 600 398.09 (0.3) (0.3) 9.0

LPG Propane (Arab Gulf)/Ton 47.00 (2.1) (2.1) (4.1) DAX 11,594.28 0.6 0.6 10.4

LPG Butane (Arab Gulf)/Ton 55.50 (3.9) (3.9) (11.6) FTSE 100 6,968.87 (0.4) (0.4) 6.8

Euro 1.13 (1.2) (1.2) (6.5) CAC 40 5,012.31 (0.3) (0.3) 10.0

Yen 119.99 0.6 0.6 0.2 Nikkei 19,890.27 0.4 0.4 13.6

GBP 1.57 (0.5) (0.5) 0.5 MSCI EM 1,040.95 (0.2) (0.2) 8.9

CHF 1.08 (1.1) (1.1) 7.3 SHANGHAI SE Composite 4,283.49 (0.6) (0.6) 32.5

AUD 0.80 (0.5) (0.5) (2.3) HANG SENG 27,591.25 (0.8) (0.8) 16.9

USD Index 94.22 1.2 1.2 4.4 BSE SENSEX 27,687.30 0.8 0.8 (0.0)

RUB 49.10 (0.9) (0.9) (19.2) Bovespa 56,204.23 (2.6) (2.6) (1.2)

BRL 0.33 (0.3) (0.3) (11.8) RTS 1,075.47 0.1 0.1 36.0

179.2

144.5

130.6