Downloaded 215 times

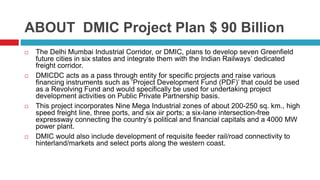

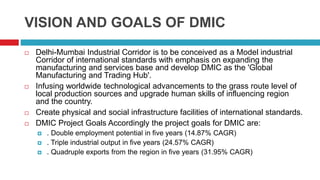

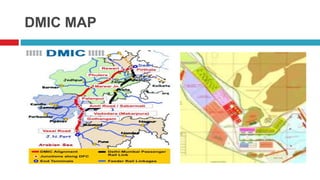

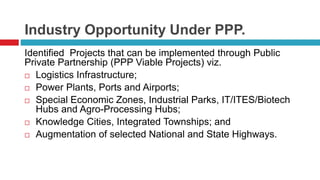

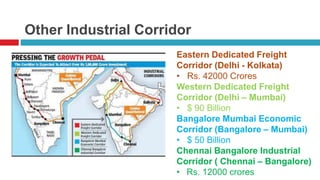

The Delhi-Mumbai Industrial Corridor (DMIC) is a $90 billion project aimed at creating seven greenfield cities, integrating advanced infrastructure such as ports, airports, and a dedicated freight corridor to enhance India's manufacturing and trading potential. DMICDC oversees the project's development and aims to double employment, triple industrial output, and quadruple exports within five years. The project is structured for extensive public-private partnerships (PPP) to leverage investment and expertise in infrastructure development across various sectors.