Download as PDF, PPTX

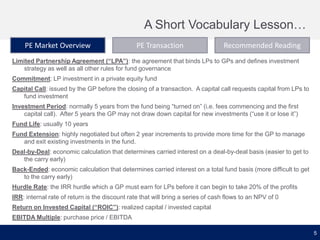

Justin Shuman's document provides an overview of private equity markets and transactions. It includes an introduction to Shuman's background and contact information. The document then covers private equity definitions and the value chain between investors, funds, and portfolio companies. It also outlines typical private equity deal processes, including sourcing deals, valuation, due diligence, and financing. Recommended reading materials on private equity, valuation, and mergers and acquisitions are listed at the end.