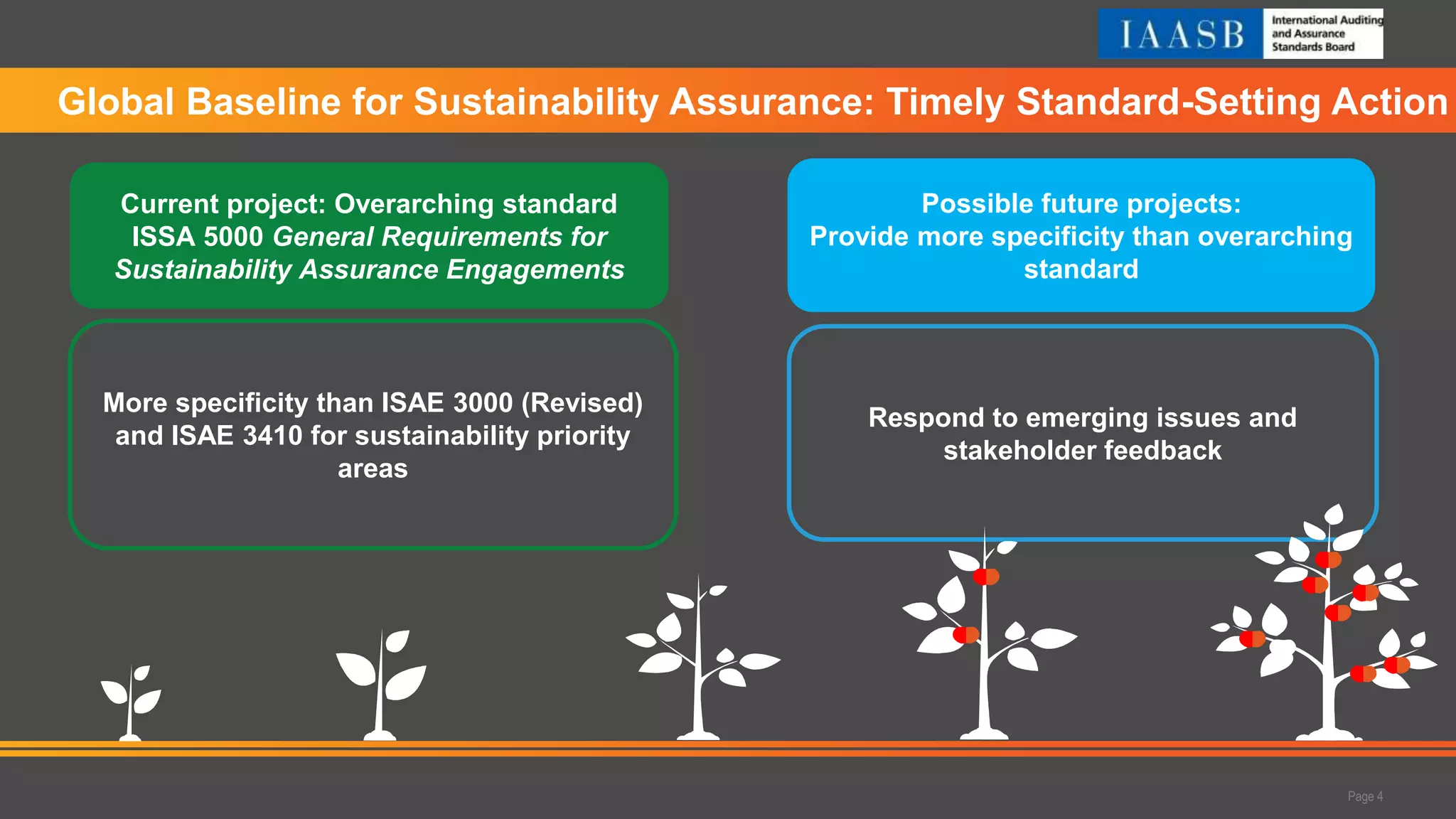

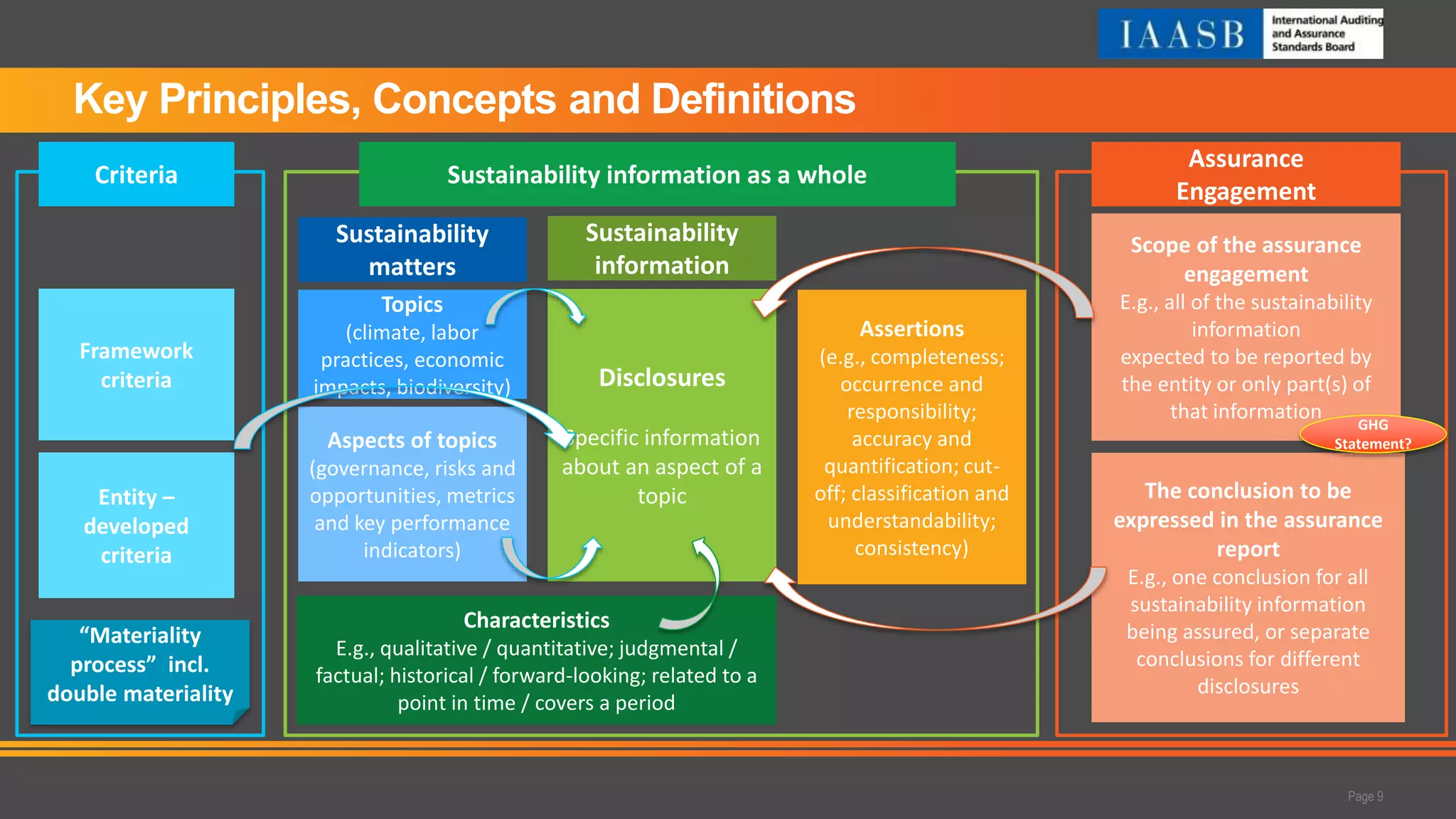

The IAASB webinar held on September 6, 2023, discussed key principles and definitions for sustainability assurance, emphasizing the development of the overarching standard ISSA 5000. The session covered topics such as materiality processes, risk assessment, and the importance of communication in reporting material misstatements. Outreach efforts to gather feedback from stakeholders were also highlighted, aiming to enhance global engagement and awareness in sustainability assurance practices.