Horizon Investment Solutions- News letter for March 2013

1. March 2013 — Over the Horizon Market Commentary by David Offer

During March the Australian share market finally retraced some ground with the All Ordinaries Index falling 2.7% for the

month to close at 4,980. At the time of writing, this weakness has continued into April with the market off a further

1%. Resource and gold shares have incurred the brunt of the fall. With concerns over Cyprus and Southern European

countries, North Korean tensions and weaker than expected Chinese and US growth, it is perhaps surprising we have not

incurred more market weakness of late.

According to our research house Morningstar, our market is trading at fair value at the current time and we agree with

this assessment. However, within our market, there does appear to be a wide contrast in valuations, with some shares

now appearing to offer good value versus the majority of shares still appearing expensive. In our opinion, two household

names that typify this are Commonwealth Bank (being expensive), now Australia’s largest company by market valuation,

and BHP Billiton (being cheap), the world’s largest resource company.

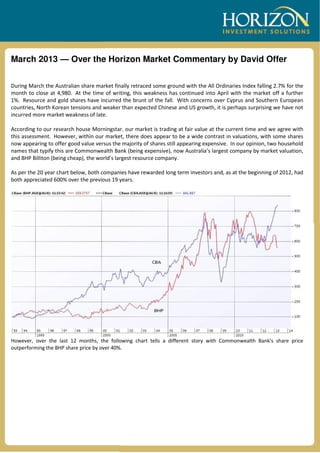

As per the 20 year chart below, both companies have rewarded long term investors and, as at the beginning of 2012, had

both appreciated 600% over the previous 19 years.

However, over the last 12 months, the following chart tells a different story with Commonwealth Bank’s share price

outperforming the BHP share price by over 40%.

2. For both Commonwealth Bank (CBA) and BHP Billiton (BHP), it has been largely business as usual. External market

influences have had the majority of impact on respective share prices, particularly for this calendar year to date.

For CBA, the current global Central Bank money printing program is depressing global interest rates and has forced

investors into more ‘risky’ share market assets in the search for yield. Australian bank shares have been a major

beneficiary of this investor rotation. With bank balance sheets in pristine condition the mainstream view is that the

banks are a safe place for conservative investors to generate the yield they need from their investments. However, we

question the safety in buying any asset once it has become expensive and feel that, as an example, CBA is entering

expensive territory.

CBA is now trading on a forecast 2014 Price Earnings (PE) ratio of 14 times and will need to pay out 80% of forecast

profits to provide it’s expected 2014 dividend yield of 5.5%. In a tight and competitive lending environment, CBA’s

earnings growth is expected to only average 5% for the next three financial years. Limited earnings growth and a high

payout ratio will result in limited opportunity for CBA to materially raise its dividend into the future and any future

tightening of interest rates (granted this is probably at least 18 months away) will take the shine of high yielding

investments very quickly. To this end we support Morningstar’s fair value of $63.00 and believe there will be future

opportunities to buy CBA (and other bank shares) at lower prices.

The share market’s view of BHP (and other resource shares) contrasts sharply and is presently largely due to fears about

a potential oversupply of iron ore to China. A recent Financial Review article provided some interesting insights. The

article stated that China’s urbanisation level is presently approximately 50% of the population and China’s urbanisation

will continue for at least the next decade. As it does, steel demand will remain elevated and is expected to grow at an

undemanding 3% to 4% per annum. China currently produces 720 million tonnes of steel (the majority of which is for

domestic consumption) and this requires approximately 1,100 million tonnes of iron ore. Australia supplies around half

of this requirement with Rio Tinto producing 260 million tonnes, BHP at 200 million tonnes and Fortescue at 100 million

tonnes. Brazil’s Vale produces 300 million tonnes. The remaining 240 million tonnes come from Chinese producers, India

(though the 100 million tonnes India was exporting is now being redirected to its domestic market) and smaller

producers including from Australia.

The market’s concern is that an expected increase in production will flood the market. These fears may be

overstated. While the Australian majors do have major expansion plans for a combined additional annual increase of 180

million tonnes of iron ore production, this will take several years to completely come on stream. Away from the

Australian majors, it is very difficult for new iron ore producers to enter the market for various reasons including

prohibitive construction costs and a scarcity of project funding. Surprisingly, at the current time, Australia appears to be

the only country in an expansion phase in iron ore production. As mentioned, India is curbing exports, while Vale is

struggling to maintain production and African exporters are not coming on stream as expected. China, as a high cost

producer, appears to have finite iron ore reserves that are only expected to last another 15 years.

3. producer, appears to have finite iron ore reserves that are only expected to last another 15 years.

Accordingly, while there will be short term gyrations in the iron ore price, the longer term outlook may not be as dire as

expected. In any event, with Rio Tinto and BHP the lowest cost global producers of iron ore, they are well positioned to

ride out any downturns in the iron ore price and ultimately prosper as higher cost producers (particularly Chinese

producers) fold. The industry view is that for Chinese iron ore suppliers to remain viable, the iron ore price needs to

remain above $120 a tonne.

It is hard to reconcile the current market pessimism and BHP’s $32.00 share price with the current iron ore price at a

respectable $142 a tonne. The last time BHP traded at these levels, the iron ore price was under $90 a tonne.

It is worth mentioning that BHP is a genuinely diversified company. In broad terms, BHP’s revenue breaks down more or

less equally three ways: iron ore, other metals, and petroleum and coal. Geographically, China is the largest market,

supplying close to 30% of BHP’s revenue, but the remaining 70% comes from elsewhere. Accordingly, while the share

market focuses on the iron ore division, it ignores the rest of the BHP business. Importantly, BHP is a major player in the

shale gas revolution occurring in America at the current time.

At $31.80, BHP is presently trading on a prospective 2014 fully franked yield of 4.15% (a 5.9% grossed up yield) and an

undemanding forecast PE ratio of approximately 10 times. While we consider Morningstar’s fair value of $50.00 as

somewhat optimistic, we think that a 12 month price target of $40.00 is not unrealistic and, if achieved, would result in a

total return of 31%.

Accordingly, while out of favour, we are comfortable buying BHP at current prices.

On a different topic, in the face of mounting speculation and negative press, last week senior Federal Government

ministers locked themselves in a room for a couple of hours to work out the future of Australia’s superannuation system,

a summary of which is enclosed. As Parliament is unlikely to consider proposed changes until after the Federal election

in September there is a high probability the proposed changes will not see the light of day. We hope the next

government will provide a little more strategic thought to the Nation’s retirement savings.

If you would like to discuss the contents of this correspondence, the upcoming Westpac hybrid issue or your investment

portfolio in general, please do not hesitate to contact our office. We would welcome your call.

David Offer

AUTHORISED REPRESENTATIVE 259188

DIRECTOR

HORIZON INVESTMENT SOLUTIONS PTY LTD

SUITE 1, POST OFFICE PLAZA, 153 VICTORIA STREET, BUNBURY WA 6230

T. 08 9791 9188 F. 08 9791 9187

E.david.offer@horizonis.com.au www.horizoninvestmentsolutions.com.au

This email was sent by Horizon Investment Solutions Pty Ltd, ACN 083 142 438, ABN 79 668 035 212, AFSL 405897

GENERAL ADVICE WARNING:

Please note that any advice provided in this email is GENERAL advice only, as the information or advice given does not take into account your particular

objectives, financial situation or needs. Opinions, conclusions and other information expressed in this email are not given or endorsed by Horizon, unless

otherwise indicated. Therefore, before you act on any of the information provided in this email, you must consider the appropriateness of the information

having regard to your particular objectives, financial situation and needs and if necessary, seek appropriate professional advice.

This email is confidential. If you are not the intended recipient, you must not view, disseminate, distribute or copy this email without our consent. Horizon

does not accept any liability in connection with any computer virus, data corruption, incompleteness, or unauthorised amendment of this email.