122Chapter 6 Supplementing the Chosen Competitive Strategy— O

1. 122Chapter 6 Supplementing the Chosen Competitive

Strategy— Other Important Strategy Choices 122

Strategy: Core Concepts and Analytical Approaches

Arthur A. Thompson, The University of Alabama 6th

Edition, 2020-2021

An e-book published by McGraw-Hill Education

122

chapter 6

Supplementing the Chosen

Competitive Strategy—

Other Important Strategy Choices

Winners in business play rough and don’t apologize for it. The

nicest part of playing hardball is watching your

competitors squirm.

—George Stalk, Jr. and Rob Lachenauer

Whenever you look at any potential merger or acquisi tion, you

look at the potential to create value for your

shareholders.

—Dilip Shanghvi, Founder and managing director of Sun

Pharmaceuticals

Don’t form an alliance to correct a weakness and don’t ally with

a partner that is trying to correct a weakness

of its own. The only result from a marriage of weaknesses is the

creation of even more weaknesses.

—Michel Robert

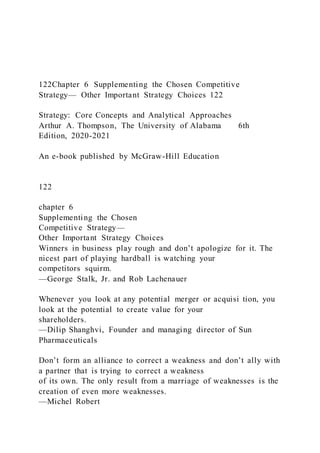

4. Differentiation?

Focused

Low Cost?

Focused

Differentiation?

Best-Cost

Provider?

Complementary Strategy Options

(A company’s second set of strategic choices)

Initiate offensive

strategic moves?

What type of website

strategy to employ?

Employ backward or forward

vertical integration strategies?

Employ defensive

strategic moves?

Whether to outsource selected

value chain activities?

Enter into strategic alliances

and partnerships?

Use merger and acquisition strategies

to strengthen competitiveness?

Functional Area Strategies to Support the Above Strategic

6. sense for a company to go on the offensive to improve its

market position and business performance. Strategic

offensives are called for when a company sees opportunities

to gain profitable market share at rivals’ expense, when a

company should strive to whittle away at a strong rival’s

competitive advantage, and when a company opts to

pursue newly emerging market opportunities. Companies

like Google, Amazon, Apple, and Facebook play hardball,

aggressively pursuing competitive advantage and trying

to reap the benefits a competitive edge offers—a leading

market share, excellent profit margins, rapid growth (as

compared to rivals), and the reputational rewards of being

known as a company on the move.1 The best offensives tend

to incorporate several behaviors and principles: (1) focusing

relentlessly on building competitive advantage and

then striving to convert competitive advantage into decisive

advantage, (2) employing the element of surprise

as opposed to doing what rivals expect and are prepared for, (3)

utilizing some of the company's competitively

potent resources and capabilities to attack rivals where they are

least able to defend themselves, and (4) being

impatient with the status quo and displaying a strong bias for

swift and decisive actions to overwhelm rivals.2

CORE CONCEPT

Sometimes a company’s best strategic option

is to seize the initiative, go on the attack, and

launch a strategic offensive to improve its

market position. It takes successful offensive

strategies to build competitive advantage, widen

an existing advantage, or narrow the advantage

held by a strong competitor.

Choosing the Basis for Competitive Attack

As a rule, challenging rivals on competitive grounds where they

are strong is an uphill struggle.3

7. Offensive initiatives that exploit competitor weaknesses stand a

better chance of succeeding than do those

that challenge competitor strengths, especially if the

weaknesses represent important vulnerabilities and

weak rivals can be caught by surprise with no ready defense.4

A company’s strategic offensives should be powered by

competitively powerful resources and capabilities—

such as a better-known brand name, lower production and/or

distribution costs, better technological

capability, or a core or distinctive competence in designing and

producing

superior performing products. Designing a strategic

offensive spearheaded by relatively weak company

resources and capabilities is like marching into battle with a

popgun—the prospects for success are dim. For instance, it

is foolish for a company with relatively high costs to employ

a price-cutting offensive. Price-cutting offensives are best

left to financially strong companies whose costs are relatively

low in comparison to those of the companies being

attacked. Likewise, it is ill-advised to pursue a product

innovation offensive without proven expertise in R&D,

new product development, and speeding new or improved

products to market.

CORE CONCEPT

The best offensives use a company’s most

potent resources and capabilities to attack

rivals where they are competitively weakest.

The principal offensive strategy options include the following:

n Offering an equally good or better product at a lower price.

Lower prices can produce market share

gains if competitors don’t respond with price cuts of their ow n

and if the challenger convinces buyers

9. market share away from rivals with

comparatively weak product innovation capabilities. Ongoing

introductions of new/improved products

can put rivals with deficient product innovation capabilities

under tremendous competitive pressure. But

such offensives can be sustained only if a company can keep its

product development pipeline full of

new and improved products that spark buyer enthusiasm.6

n Pursuing disruptive product innovation to create new markets.

While this strategy can be riskier and

more costly than continuous product innovation, “big bang”

disruptive product innovation can be a

game changer if successful.7 Disruptive innovation involves

perfecting a new product with a few trial

users, then quickly rolling it out to the whole market in an

attempt to get many buyers to embrace an

altogether new and better value proposition quickly. Examples

include online degree programs, self-

driving capabilities for motor vehicles, Apple Music, and

Amazon’s Kindle (which undercut the sales of

hardcopy fiction and non-fiction books).

n Adopting and improving on the good ideas of other companies

(rivals or otherwise).8 The idea of

warehouse home improvement centers did not originate with

The Home Depot cofounders Arthur Blank

and Bernie Marcus. They got the “big box” concept from their

former employer Handy Dan Home

Improvement. But they were quick to improve on Handy Dan’s

business model and strategy and take

The Home Depot to the next plateau in terms of product line

breadth and customer service. Offense-

minded companies are often quick to adopt any good idea (not

nailed down by a patent or other legal

protection) in an effort to create competitive advantage for

10. themselves.9

n Deliberately attacking those market segments where a key

rival makes big profits.10 Long a dominant

force in small automobiles, Toyota launched a hardball attack

on General Motors, Ford, and Chrysler

in the U.S. market for light trucks and SUVs, the very market

segments where the Detroit automakers

historically earned big profits (roughly $10,000 to $15,000 per

vehicle). Toyota now offers equivalent

vehicles, earns handsome profits of its own in these two market

segments, and has stolen sales and

market share from its U.S.-based rivals. Dell opted to introduce

its own brand of printers and printing

supplies in the 1990s because its principal rival in desktop and

laptop computers was Hewlett-Packard,

which made its biggest profits in printing and printing supplies;

by attacking H-P in the market for

printers, Dell sought to force H-P to devote management

attention and resources to defending its printing

business and distract its attention away from trying to wrest

market leadership away from Dell in the PC

market.

n Attacking the competitive weaknesses of rivals. Such

offensives present many options. One is to go

after the customers of those rivals whose products lag on

quality, features, or product performance. If

a company has especially good customer service capabilities, it

can make special sales pitches to the

customers of those rivals who provide subpar customer service.

Aggressors with a recognized brand

name and strong marketing skills can launch efforts to win

customers away from rivals with weak brand

recognition. There is considerable appeal in emphasizing sales

to buyers in geographic regions where

12. occasional low-balling on price (to win

a big order or steal a key account from a rival); surprising key

rivals with sporadic but intense bursts

of promotional activity (offering a 20 percent discount for one

week to draw customers away from

rival brands); or undertaking special campaigns to attract buyers

away from rivals plagued with a

strike or problems in meeting buyer demand.11 Guerrilla

offensives are particularly well suited to small

challengers who have neither the resources nor the market

visibility to mount a full-fledged attack on

industry leaders.

n Launching a preemptive strike to secure an advantageous

position that rivals are prevented or

discouraged from duplicating.12 What makes a move

preemptive is its one-of-a-kind nature—

whoever strikes first stands to acquire competitive assets that

rivals can’t readily match. Examples of

preemptive moves include (1) securing the best distributors in a

particular geographic region or country;

(2) obtaining the most favorable site along a heavily traveled

thoroughfare, at a new interchange or

intersection, in a new shopping mall, in a natural beauty spot,

close to cheap transportation or raw

material supplies or market outlets, and so on; (3) tying up the

most reliable, high-quality suppliers via

exclusive partnerships, long-term contracts, or even acquisition;

and (4) moving swiftly to acquire the

assets of distressed rivals at bargain prices. To be successful, a

preemptive move doesn’t have to totally

block rivals from following or copying; it merely needs to give

a firm a prime position that is not easily

circumvented.

How long it takes for an offensive to yield good results varies

13. with the competitive circumstances.13 It can be

short if buyers respond immediately (as can occur with a

dramatic price cut, an imaginative ad campaign, or

an especially appealing new product). Securing a competitive

edge can take much longer if winning consumer

acceptance of the company’s product will take some time or if

the firm may need several years to debug a new

technology or put new production capacity in place. But how

long it takes for an offensive move to improve a

company’s market standing—and whether the move will prove

successful—depends in part on whether and how

quickly rivals recognize the threat and begin a counter-

response. And any responses on the part of rivals hinge

on whether (1) they have effective countermoves in their arsenal

of strategic options and (2) they believe that a

counterattack is worth the expense and the distraction.14

Blue Ocean Strategy—A Special Kind of Offensive

A blue ocean strategy seeks to gain a dramatic and durable

competitive advantage by abandoning efforts to

beat out competitors in existing markets and, instead, inventing

a new industry or distinctive market segment

that renders existing competitors largely irrelevant and allows a

company to create and capture altogether new

demand.14 This strategy views the business universe as

consisting of two distinct types of market space. One is

where industry boundaries are defined and accepted, the

competitive rules of the game are well understood and

accepted by all industry members, and companies use their

resources and capabilities to compete against rivals

and achieve satisfactory or better performance. In such markets,

lively competition constrains a company’s

prospects for rapid growth and superior profitability since rivals

move quickly to either imitate or counter the

successes of competitors. The second type of market space is a

“blue ocean” where the industry does not really

15. than the price of a conventional circus ticket to have an

“entertainment experience” featuring sophisticated

clowns and star-quality acrobatic acts in a comfortable

atmosphere.

Choosing Which Rivals to Attack

Offensive-minded firms need to analyze which of their rivals to

challenge as well as how to mount that challenge.

The following are the best targets for offensive attacks:15

n Market leaders that are vulnerable. Offensive attacks make

good sense when a company that leads

in size and market share is not a true leader in serving the

market well. Signs of leader vulnerability

include unhappy buyers, an inferior product line, a weak

competitive strategy with regard to low-cost

leadership or differentiation, strong emotional commitment to

an aging technology the leader has

pioneered, outdated plants and equipment, a preoccupation with

diversification into other industries,

and mediocre or declining profitability. Offensives to erode the

positions of market leaders have real

promise when the challenger is able to revamp its value chain or

innovate to gain a fresh cost-based or

differentiation-based competitive advantage.16 To be judged

successful, attacks on leaders don’t have to

result in making the aggressor the new leader; a challenger may

“win” by simply becoming a stronger

runner-up. Caution is well advised in challenging strong market

leaders—there is a significant risk of

squandering valuable resources in a futile effort or precipitating

a fierce and profitless industry-wide

battle for market share.

n Runner-up firms with weaknesses in areas where the

challenger is strong. Runner-up firms are an

17. strategies are to lower the risk of being attacked,

weaken the impact of any attack that occurs, and induce

challengers to aim their offensive initiatives at other rivals.

While defensive strategies usually don’t enhance a firm’s

competitive advantage, they can definitely help fortify its

competitive position, protect its most valuable resources

and capabilities from imitation, and defend whatever

competitive advantage it might have. Defensive strategies can

take either of two forms: actions to block

challengers and actions to signal the likelihood of strong

retaliation.

CORE CONCEPT

Good defensive strategies can help protect

competitive advantage but rarely are the basis

for creating it.

Blocking the Avenues Open to Challengers The most frequently

employed approach to defending a

company’s present position involves actions that restrict a

challenger’s options for initiating competitive

attack. There are any number of obstacles that can be put in the

path of would-be challengers.17 A defender

can participate in alternative technologies as a hedge

against rivals attacking with a new or better technology. A

defender can introduce new features, add new models, or

broaden its product line to close off gaps and vacant niches

to opportunity-seeking challengers. It can thwart rivals’ efforts

to attack with a lower price by maintaining

a lineup of product selections that includes economy-priced

options for price-sensitive buyers. It can try to

discourage buyers from trying competitors’ brands by

lengthening warranties, offering free training and support

18. services, developing the capability to deliver spare parts to

users faster than rivals can, providing coupons and

sample giveaways to buyers most prone to experiment, and

making early announcements about impending new

products or probable price cuts to induce potential buyers to

postpone switching. It can challenge the quality or

safety of rivals’ products. Finally, a defender can grant volume

discounts or better financing terms to dealers and

distributors to discourage them from experimenting with other

suppliers, or it can convince them to handle its

product line exclusively and force competitors to use other

distribution outlets.

There are many ways to throw obstacles in the

path of would-be challengers.

Signaling Challengers that Retaliation Is Likely The goal of

signaling challengers that strong retaliation

is likely in the event of an attack is either to dissuade

challengers from attacking at all or to divert them to less-

threatening options. Either goal can be achieved by letting

challengers know the battle will cost more than it is

worth. Would-be challengers can be signaled by:18

n Publicly announcing management’s commitment to maintain

the firm’s present market share.

n Publicly committing the company to a policy of matching

competitors’ prices and terms of sale.

n Maintaining a war chest of cash and marketable securities.

n Making an occasional strong counter-response to the moves of

weak competitors to enhance the firm’s

image as a tough defender.

20. Product Information–Only Strategies—Avoiding Channel

Conflict

Operating a website that contains extensive product information

but relies on click-throughs to the websites of

distribution channel partners for sales transactions (or that

informs site visitors where nearby retail stores are

located) is an attractive option for manufacturers and/or

wholesalers that have invested heavily in building and

cultivating retail dealer networks to access end users. A

company vigorously pursuing online sales to consumers

at the same time it is also heavily promoting sales to consumers

through its network of wholesalers and retailers is

competing directly against its distribution allies. Such actions

constitute channel conflict and are a tricky road to

negotiate. A company actively trying to grow online sales is

signaling a weak strategic commitment to its dealers

and a willingness to cannibalize dealers’ sales and growth

potential. The likely result is angry dealers and loss

of dealer goodwill. Some or many of the company’s dealers may

opt to put more effort into marketing the brands

of rival manufacturers who don’t sell online or whose online

sales effort is passive and nonthreatening. Quite

possibly, a company may lose more sales by offending its

dealers than it gains from its own online sales effort.

Consequently, in industries where the strong support and

goodwill of dealer networks is essential, companies

may conclude that it is important to avoid channel conflict and

their website should be designed to partner with

dealers rather than compete with them.

Website Sales as a Minor Distribution Channel

A second strategic option is to use online sales as a relatively

minor distribution channel for achieving incremental

sales, gaining online sales experience, and doing marketing

research. If channel conflict poses a big obstacle to

22. n When profit margins from online sales are bigger than those

earned from selling to wholesale/retail

customers.

n When encouraging buyers to visit the company’s website

helps educate them about the ease and

convenience of purchasing online and, over time, prompts more

and more buyers to purchase online

(where company profit margins are greater)—which makes

incurring channel conflict in the short term

and competing against traditional distribution allies potentially

worthwhile.

n When selling directly to end users allows a manufacturer to

make greater use of build-to-order

manufacturing and assembly, which if met with growing buyer

approval would increase the rate at

which sales migrate from distribution allies to the company’s

website; such migration could lead to

streamlining the company’s value chain and boosting its profit

margins.

Brick-and-Click Strategies

Some companies employ brick-and-click strategies, whereby

they sell to consumers both at their own websites

and at their own company-owned retail stores (or the stores of

independent retailers). Brick-and-click strategies

have two big appeals: They are an economic means of

expanding a company’s geographic reach, and they give

both existing and potential customers another choice of how to

communicate with the company, shop for product

information, make purchases, or resolve customer service

problems. Software developers, for example, have

come to rely on the Internet as a highly effective distribution

channel to complement sales at brick-and-mortar

23. retailers. Allowing end users to make an online purchase and

download it immediately has the big advantage

of eliminating the costs of producing and packaging CDs and

cutting out the costs and margins of software

wholesalers and retailers (often 35 to 50 percent of the retail

price). Chain retailers like Walmart and Best Buy

operate online stores for their products primarily as a

convenience to customers who prefer to buy online and

have the items shipped or available for pickup at nearby stores.

Many brick-and-mortar retailers can enter online retailing at

relatively low cost—all they need is a web store for

displaying products, accepting customer orders, and systems for

filling and delivering orders. Brick-and-mortar

retailers (as well as manufacturers with company-owned retail

stores) can use personnel at their distribution

centers and/or retail stores to fill and ship the orders of online

buyers, and they can allow online buyers to pick

up their orders at the nearest local retail store. Walgreens, a

leading drugstore chain, lets customers order a

prescription online and then pick it up at the drive-through

window or inside counter of a local store—allowing

customers to order online and then pick up their orders at local

stores has become a popular strategy for many

retailers because it enables them to better compete with

Amazon. In banking, a brick-and-click strategy allows

customers to use local branches and ATMs for depositing

checks and getting cash while using online systems to

pay bills, monitor account balances, and transfer funds. Bed

Bath & Beyond uses its web store to display and sell

the items stocked in its stores but also to display and sell a

wider number of brands, colors, and selections in the

same product categories that, for reasons of limited shelf space,

are not available in its stores—such a strategy

gives customers a much wider selection and boosts its online

sales.

25. n Whether it will have a broad or a narrow product offering. A

one-stop shopping strategy like that

employed by Amazon.com (which offers “Earth’s Biggest

Selection” of items for sale at 13 international

websites) has the appealing economics of helping spread fixed

operating costs over a wide number of

items and a large customer base. Online sellers like Quicken

Loans (the largest online provider of home

mortgages), and Hotels.com have adopted classic focus

strategies and cater to a sharply defined target

audience shopping for a particular product or product category.

n Whether to outsource order fulfillment activities or perform

them internally. Most online sellers find

it more economical to outsource order fulfillment activities to

specialists who make a business of

providing warehouse space, stocking inventories, and installing

the capabilities to pick, pack, and ship

orders cost-efficiently for a number of different online retailers.

Only very high-volume online retailers

can develop and install the capabilities to perform order

fulfillment activities internally at costs below

those of outside specialists. Buy.com, an online superstore with

some 30,000 items, obtains products

from name brand manufacturers and uses outsiders to stock and

ship those products—thus, its focus is

not on manufacturing or order fulfillment but rather on online

sales.

n How it will draw traffic to its website and then convert page

views into revenues. Websites must be

cleverly marketed. Unless web surfers hear about the site, like

what they see on their first visit (and

perhaps make a purchase), and are intrigued enough to return

again and again to both view information

27. products but they outsource all fabric manufacture and garment-

making activities to contract manufacturers in

low-wage countries. Starbucks finds purchasing coffee beans

from independent growers in most of the world’s

coffee-growing regions far more advantageous than having its

own coffee-growing operation.

Outsourcing certain value chain activities can be strategically

advantageous whenever:

n An activity can be performed better or more cheaply by

outside specialists. A company should generally

not perform any value chain activity internally that outsiders

can perform more efficiently or effectively.

The chief exception is when a particular activity is strategically

crucial and internal control over that

activity is deemed essential. Dolce and Gabbana, for example,

outsources manufacture of its brand of

sunglasses to Luxottica—a company considered to be the

world’s best producer of top-quality fashion

sunglasses and high-tech prescription eyewear, known for its

Ray-Ban, Oakley, and Oliver Peoples

brands.

n The activity is not crucial to the firm’s ability to achieve

sustainable competitive advantage.

Outsourcing of maintenance services, data processing and data

storage, fringe benefit management,

website operations, call center operations, and similar

administrative support activities to specialists

is commonplace. Colgate has reduced its information systems

costs by more than 10 percent annually

through an outsourcing agreement with IBM.

n It streamlines company operations in ways that improve

organizational flexibility or speeds the time to

28. get new products to market. Outsourcing gives a company the

flexibility to switch suppliers in the event

one or more of its present suppliers fall behind competing

suppliers. To the extent that its suppliers can

speedily get next-generation parts and components into

production, a company can get its own next-

generation product offerings into the marketplace quicker.

Moreover, seeking new suppliers with the

needed capabilities already in place is frequently quicker,

easier, less risky, and cheaper—firms that

internally produce the parts and components they need are

periodically confronted with sometimes

formidable costs to update obsolete parts-making capabilities or

to install and master new parts-making

technologies.

n It reduces the company’s risk exposure to changing

technology or shifting buyer preferences. When

a company outsources certain parts, components, and services,

its suppliers must bear the burden of

incorporating state-of-the-art technologies and/or undertaking

redesigns and upgrades to accommodate

a company’s plans to introduce next-generation products. If

what a supplier provides is designed out of

next-generation products or rendered unnecessary by

technological change, it is the supplier’s business

that suffers rather than the company’s.

n It improves a company’s ability to innovate. Collaborative

partnerships with world-class suppliers who

have cutting-edge intellectual capital and are early adopters of

the latest technology give a company

access to ever better parts and components —such supplier-

driven innovations, when incorporated into

a company’s own product offering, fuel a company’s ability to

introduce its own new and improved

30. outsiders and contracted to repurchase the output from the new

owners.

The Big Risk of Outsourcing Value Chain Activities

The biggest danger of outsourcing is that a company will farm

out too many or the wrong types of activities, thereby

unduly narrowing the scope of its capabilities in ways that

unwittingly reduce its long-term competitiveness.21

For example, in recent years, companies anxious to reduce

operating costs have opted to outsource such strategically

important activities as product development, engineering

design, and sophisticated manufacturing tasks—the very

capabilities that underpin a company’s ability to lead

sustained product innovation. While these companies have

apparently been able to lower their operating costs by

outsourcing these functions to outsiders, their ability to

lead the development of innovative new products is weakened

because so many of the cutting-edge ideas and

technologies for next-generation products come from outsiders.

For example, most U.S. brands of laptops and cell

phones are now not only manufactured but also designed in

Asia.22 It is strategically dangerous for a company to

be dependent on outsiders to provide it with the skills,

knowledge, and capabilities that over the long run heavily

influence its competitiveness and market success. Companies

like Cisco are alert to the danger of farming out the

performance of strategy-critical value chain activities and take

actions to protect against being held hostage by

outside suppliers. Cisco guards against loss of control and

protects its manufacturing expertise by designing the

production methods its contract manufacturers must use. Cisco

keeps the source code for its designs proprietary,

thereby controlling the initiation of all improvements and

safeguarding its innovations from imitation. Further,

Cisco has developed online systems to monitor the factory

operations of contract manufacturers around the

31. clock, so that it knows immediately when problems arise and

can decide whether to get involved.

A company must guard against outsourcing

activities that can unwittingly degrade its

capabilities to be a master of its own destiny.

Vertical Integration Strategies: Operating Across More Stages

of the Industry Value Chain

Vertical integration extends a firm’s competitive and operating

scope within the same industry. It involves

expanding the firm’s range of activities backward into sources

of supply and/or forward toward end users. Thus,

if a manufacturer invests in facilities to produce certain

component parts that it formerly purchased from outside

suppliers, it has engaged in backward vertical integration

and extended its competitive scope backward into the

production of component parts, but its business remains

in the same industry as before. The only change is that it

has operations in two stages of the industry value chain.

Similarly, if a paint manufacturer—Sherwin-Williams, for

example—elects to integrate forward by opening 500

retail stores to market its paint products directly to consumers,

its entire business is still in the paint industry even

though its competitive scope extends from manufacturing to

retailing.

CORE CONCEPT

A vertically integrated firm is one whose business

activities extend across several portions or stages

of an industry’s overall value chain.

A firm can pursue vertical integration by starting its own

operations in other stages in the industry’s activity

chain or by acquiring a company already performing the

33. drop-off in quality. Neither outcome is a slam dunk. To

begin with, a company’s in-house requirements are often

too small to reach the optimum size for low-cost operation—for

instance, if it takes a minimum production

volume of one million units to achieve mass production

economies and a company’s in-house requirements

are just 250,000 units, then it falls way short of being able to

capture the scale economies of outside suppliers

(who may readily find buyers for one million or more units).

Furthermore, matching the production efficiency

of suppliers is fraught with problems when suppliers have high-

caliber production capabilities of their own,

when the technology they employ has elements that are hard to

master, and/or when substantial R&D expertise

is required to develop next-version parts and components, or

keep pace with advances in parts/components

manufacturing processes.

CORE CONCEPT

Backward vertical integration involves entry

into activities performed by suppliers or other

enterprises positioned in earlier stages of an

industry’s overall value chain.

That said, occasions still arise when a company can improve its

cost position and competitiveness by performing

a broader range of value chain activities internally rather than

having some of these activities performed by

outside suppliers. The best potential for being able to reduce

costs via a backward integration strategy exists in

situations where a company must deal with a few suppliers with

substantial bargaining power, where suppliers

have outsized profit margins, where the item being supplied is a

major cost component, and where the requisite

technological/production capabilities are easily mastered or can

be gained by acquiring a supplier with most or

34. all of the needed capabilities. Situations also arise when

integrating backward can enable a company to reduce

costs by facilitating the coordination of production flows from

one stage to the next and avoiding bottlenecks

and delays that disrupt production schedules. Furthermore, if a

company has proprietary know-how that it wants

to keep from rivals, then in-house performance of value chain

activities related to this know-how is beneficial

even if outsiders can perform such activities. Backward

integration also spares a company the risk of being

heavily dependent on suppliers for crucial components or

support services and reduces exposure to supplier

price increases.

Apple decided to backward into the production of chips and

other electronic components and hardware used in

its iPhone and computers because they were major cost

components, suppliers had bargaining power, and in-

house production would help coordinate design tasks and

protect Apple’s proprietary technology. International

Paper Company backward integrated into pulp mills and located

them adjacent to its paper plants to reap the

benefits of coordinated production flows, reduced energy usage,

and negligible costs of transporting freshly-

produced paper pulp directly to the production line in its paper

plants.

Backward vertical integration can produce a differentiation-

based competitive advantage when a company, by

performing activities internally, ends up with a better-quality or

better-performing product, improved customer

service capabilities, or in other ways is able to deliver added

value to customers. On occasion, integrating into

more stages along the industry value chain can add to a

company’s differentiation capabilities by allowing it to

36. Consequently, insurers like State Farm and Allstate have

integrated forward and set up local sales offices with

local agents to exclusively market and service their insurance

policies. Likewise, it can be advantageous for a

manufacturer to integrate forward into wholesaling or retailing

via company-owned distributorships or a chain of

retail stores rather than depend on the marketing and sales

efforts of independent distributors/retailers that stock

multiple brands and steer customers to those brands earning

them the highest profits. To avoid dependence on

distributors/dealers with divided loyalties, Goodyear has

integrated forward into company-owned and franchised

retail tire stores. Consumer-goods companies like Coach, Under

Armour, Nike, Tommy Hilfiger, Pepperidge

Farm, Samsonite, Ann Taylor, and Polo Ralph Lauren have

integrated forward and operate company-operated

retail stores as well as their own branded stores in factory outlet

malls that enable them to move overstocked

items, slow-selling items, and seconds. Growing numbers of

producers have integrated forward and begun

selling directly to end-users at company websites, thus reducing

dependence on traditional wholesale and retail

channels.

CORE CONCEPT

Forward vertical integration involves entering

into the performance of industry value chain

activities located closer to end users.

The Disadvantages of a Vertical Integration Strategy

Vertical integration has some important drawbacks, however.

The biggest of these include the following:24

37. n Vertical integration boosts a firm’s capital investment in the

industry, thereby increasing business risk

(what if industry growth and profitability unexpectedly go

sour?).

n Integrating backward or forward creates a vested interest for a

firm to continue performing the integrated

system of value chain activities it has invested money and effort

into establishing (even if internal

performance of certain of these value chain activities later

becomes suboptimal). Why? Because there

are barriers to quickly or easily exiting the performance of

value chain activities spanning two or more

stages of the industry’s value chain, including facilities

shutdowns, costly write-offs of undepreciated

assets, employee layoffs, and disrupted performance of related

value chain activities. However, a

company that obtains parts and components from outside

suppliers can always shop the market for

the newest, best, or cheapest parts and components. A company

that does not have its own network of

company-owned distributorships and retail stores can switch

distributors and/or distribution channel

emphasis whenever it is advantageous to do so.

n Some vertically integrated companies are slow to adopt new

technologies or production methods because

of reluctance to write off undepreciated assets or because they

assign higher priority to spending capital

for other company projects or because they see benefits in

sticking with the present technology or

Chapter 6 • Supplementing the Chosen Competitive Strategy—

Other Important Strategy Choices 136

39. n Vertical integration poses all kinds of capacity-matching

problems. In motor vehicle manufacturing,

for example, the most efficient scale of operation for making

axles is different from the most economic

volume for radiators, and different yet again for both engines

and transmissions. Building the capacity to

produce just the right number of axles, radiators, engines, and

transmissions in-house—and doing so at

the lowest unit costs for each—poses significant challenges in

cost-effectively producing each different

part/component.

n Integrating forward or backward typically requires new or

different skills and business capabilities.

Parts and components manufacturing, assembly operations,

wholesale distribution, retailing, and

direct sales via the Internet involve using different know -how,

resources, and capabilities to master the

performance of different value chain activities. A manufacturer

that integrates backward into parts and

components production has to become proficient in different

technologies and production methods and

very likely source needed materials from different suppliers. A

manufacturing company contemplating

forward integration needs to consider carefully whether it

makes good business sense to invest time

and money in developing the expertise and merchandising skills

to be successful in wholesaling and/

or retailing. Many manufacturers learn the hard way that

company-owned wholesale/retail networks

present many headaches, fit poorly with what they do best, and

don’t always add the kind of value to

their core business as originally planned. Selling to customers

via the Internet poses still another set of

problems when aiming to achieve proficient performance of

strikingly different value chain activities.

40. In today’s world of close working relationships with suppliers

and efficient supply chain management systems,

relatively few companies can make a strong economic case for

integrating backward into the business of suppliers.

The best materials and components suppliers stay abreast of

advancing technology and best practices and are

adept in making good quality items, delivering them on time,

and keeping their costs and prices competitive.

Weighing the Pros and Cons of Vertical Integration All in all,

therefore, a strategy of vertical integration

can have both important strengths and weaknesses. The tip of

the scales depends on (1) the difficulties and costs

of acquiring or developing the resources and capabilities needed

to operate in another stage of the industry value

chain, (2) the size of the benefits vertical integration offers in

terms of lowering costs or enhancing differentiation

and the value delivered to customers; (3) the impact of vertical

integration on investment costs, flexibility,

and response times, (4) the administrative costs of coordinating

operations across more value chain activities;

and (5) whether the integration substantially enhances a

company’s competitiveness and profitability. Vertical

integration strategies have merit according to which capabilities

and value chain activities truly need to be

performed in-house and which can be performed better or

cheaper by outsiders. Absent solid benefits in relation

to the associated costs and risks, integrating forward or

backward is not likely to be an attractive strategy option.

Chapter 6 • Supplementing the Chosen Competitive Strategy—

Other Important Strategy Choices 137

42. expenses, and profits (losses) of the venture according to their

ownership percentages. In many joint ventures,

it is formally agreed that one of the owners (typically a majority

owner) will exercise operating control over the

venture. Because a joint venture involves mutual ownership, it

tends to be more durable than an alliance where a

partner can just abruptly decide to abandon the alliance. A joint

venture owner who wants out of the venture must

negotiate arrangements to be bought out or else get the other

owners to agree to dissolve the venture.

An alliance or joint venture becomes “strategic”—as opposed to

just a useful collaborative arrangement—when

it serves any of the following purposes or intended outcomes:25

n It facilitates achievement of an important business objective

(like reducing risk to a company’s business,

lowering costs, or delivering more value to customers in the

form of better quality, extra features, and

greater durability).

n It helps build or strengthen a company’s competitively

valuable resources and capabilities.

n It helps remedy an important resource deficiency or

competitive weakness.

n It speeds the development of competitively important new

technologies and/or product innovations.

n It facilitates entry into new geographic markets or pursuit of

important market opportunities.

n It helps block or defend against a competitive threat or

mitigate a significant risk to a company’s

business.

44. The most common reasons why companies enter into strategic

alliances are to expedite the development of

promising new technologies or products, to overcome deficits in

their own expertise and capabilities, to bring

together the personnel and expertise needed to create desirable

new skill sets and capabilities, to improve supply

chain efficiency, to gain economies of scale in production

and/or marketing, and to acquire or improve market access

through joint marketing agreements.26 When a company

needs to correct particular resource/capability gaps or

deficiencies, it may be faster and cheaper to partner with

other enterprises that have the missing resources and

capabilities. Moreover, partnering offers greater flexibil ity

should a company’s competitive requirements later change.

Manufacturers frequently pursue alliances with parts

and components suppliers to wring cost savings out of supply

chain activities, to improve the quality of parts and

components, to better assure reliable supplies and on-time

deliveries, and to speed new products to market. In

industries where technology is advancing rapidly, alliances are

all about fast cycles of learning, staying abreast of

the latest developments, and gaining quick access to the latest

round of technological know-how and capability.

In bringing together firms with different skills and intellectual

capital, alliances open up learning opportunities

that help partner firms strengthen their own portfolios of

resources, core competences, and capabilities and

thereby become more competitive.27

The best strategic alliances are highly selective,

45. focusing on particular value chain activities and on

obtaining a specific competitive benefit. They tend

to enable a firm to build on its strengths and learn.

Companies find strategic alliances particularly valuable in

several other instances. A company racing for global

market leadership needs alliances to:28

n Get into critical country markets quickly and accelerate the

process of building a potent global market

presence.

n Gain inside knowledge from local partners about unfamiliar

markets and cultures. For example, U.S.,

European, and Japanese companies wanting to build market

footholds in China and other fast-growing

Asian markets have pursued local partnership arrangements to

help guide them through the maze of

government regulations, to supply knowledge of local markets,

to provide guidance on adapting their

products to better match local buying preferences, to set up

local manufacturing capabilities, and/or to

assist in distribution, marketing, and promotional activities.

n Access valuable skills and competences that are concentrated

in particular geographic locations

(such as software design competences in the United States,

fashion design skills in Italy, and efficient

manufacturing skills in Japan, Taiwan, China, and other

Southeast Asian countries).

A company that is racing to stake out a strong position in an

industry of the future needs alliances to:29

n Establish a stronger beachhead for participating in the target

industry.

47. redirect the collaborative effort.30

Many Alliances Are Short-Lived or Break Apart Most alliances

that aim at technology-sharing or

providing market access turn out to be temporary, fulfilling

their purpose after a few years because the benefits

of mutual learning have occurred and because both partners’

businesses have developed to the point where

they are ready to go their own ways. The likelihood that such

alliances will be temporary makes it important

for each partner to learn thoroughly and rapidly about the other

partner’s technology, business practices, and

organizational capabilities and then promptly transfer valuable

ideas and practices into its own value chain

activities. Alliances tend to be longer lasting when (1) they

involve collaboration with suppliers or distribution

allies, (2) each party’s contribution involves activities in

different portions of the industry value chain, or (3) both

parties conclude that continued collaboration is in their mutual

interest.

Most alliance partners don’t hesitate to terminate their

collaboration when the payoffs run out or when alliance

members conclude the expected benefits are unlikely to

materialize. A 1999 study by Accenture, a global

business consulting organization, revealed that 61 percent of

alliances were either outright failures or “limping

along.” In 2004, McKinsey & Company estimated that the

overall success rate of alliances was around 50

percent, based on whether the alliance achieved the stated

objectives.31 A 2007 study found that, even though

the number of strategic alliances was increasing about

25 percent annually, the failure rate of alliances hovered

between 60 to 70 percent.32 The high “divorce rate” among

strategic allies has several causes—an inability to work

well together, tendencies among alliance members to share

48. only limited information about their valuable skills and

expertise (which prevented other members from learning

much of value), changing conditions that render the purpose of

the alliance obsolete, growing disagreement

among alliance members about the purpose, priorities, and/or

targeted benefits of the alliance, the emergence

of more attractive paths to capture the intended benefits, and

emerging marketplace rivalry between certain

alliance members.33 Experience indicates that alliances stand a

reasonable chance of helping a company reduce

competitive disadvantage but rarely can entering into an

alliance enable a company to boost the competitive

power of its resources and capabilities by enough to outcompete

rivals or gain a competitive advantage.

Large numbers of strategic alliances fail to live

up to expectations and are dissolved after a

few years.

The Strategic Dangers of Relying Heavily on Alliances and

Cooperative Partnerships. The

Achilles heel of alliances and strategic cooperation is becoming

dependent on other companies for essential

expertise and capabilities. To be a market leader (and perhaps

even a serious market contender), a company

must ultimately develop its own capabilities in areas where

internal strategic control is pivotal to protecting its

competitiveness and building competitive advantage. Moreover,

some alliances and cooperative arrangements

hold only limited potential when a partner maintains full control

over its most valuable skills and expertise and

is unwilling to give other alliance members much access to

these capabilities. As a consequence, acquiring or

merging with a company possessing the needed resources and

capabilities is a better solution.

50. usually has a different name. An acquisition

is a combination in which one company, the

acquirer, purchases and absorbs the operations

of another, the acquired.

The main impetus for merger and acquisition strategies is to

fundamentally alter a company’s trajectory and

improve its business outlook. Such strategies typically aim at

achieving any of four objectives:35

1. Creating a more cost-efficient operation out of the combined

companies. Many mergers and acquisitions

are undertaken with the objective of transforming two or more

otherwise high-cost companies into one

lean competitor with average or below-average costs. When a

company acquires another company in

the same industry, there’s usually enough overlap

in operations that certain inefficient plants can be

closed or distribution activities partly combined and

downsized (when nearby centers serve some of the

same geographic areas) or sales force and marketing

activities can be combined and downsized (when

each company has salespeople calling on the same

customer). The combined companies may also be

able to reduce supply chain costs because of buying

in greater volume from common suppliers and from

closer collaboration with supply chain partners. Likewise, it is

usually feasible to squeeze out cost savings

in administrative activities, again by combining and downsizing

such administrative activities as finance

and accounting, information technology, human resources, and

so on.

Combining the operations of two companies, via

merger or acquisition, is an attractive strategic

option for fundamentally altering a company’s

51. trajectory—achieving operating economies,

strengthening the resulting company’s

resources, capabilities, and competitiveness in

important ways, and opening up avenues of new

market opportunity.

2. Strengthening the resulting company’s resources,

capabilities, and competitiveness in important ways.

Combining the operations of two or more companies, via merger

and/or acquisition, is often aimed

at significantly bolstering the competitive power of the

resulting company’s resources, know-how,

skills and expertise—and doing so quickly (as compared to

undertaking a time-consuming and perhaps

expensive internal effort to accomplish the same result). From

2000 through February 2019, Cisco

Systems purchased 128 companies to give it more technological

reach and product breadth, thereby

enhancing its standing as the world’s biggest provider of

hardware, software, and services for building

and operating Internet networks.

3. Expanding a company’s geographic coverage. One of the best

and quickest ways to expand a company’s

geographic coverage is to acquire rivals with operations in the

desired locations. And if there is some

geographic overlap, then a side benefit is being able to reduce

costs by eliminating duplicate facilities in

those geographic areas where undesirable overlap exists. Banks

like Wells Fargo and Bank of America

have pursued geographic expansion by making a series of

acquisitions over the years, enabling them to

establish a market presence in an ever-growing number of states

and localities. Food products companies

53. beverage lineup by introducing its own new products (like

Powerade and Dasani), it has also expanded

its lineup by acquiring Minute Maid (juices and juice drinks),

Odwalla (juices), Hi-C (ready-to-drink

fruit beverages), and dozens of other brands of beverages.

Going into 2019, Coca-Cola had a portfolio

of over 500 brands and 3,900 choices of beverage products,

some internally developed and most the

result of an active and longstanding acquisition program.

Many companies have used mergers and acquisitions to catapult

themselves from the ranks of the unknown into

positions of market prominence. Clear Channel Communications

began operations as a single radio station in

Texas; after acquiring assorted media assets over four decades,

in 2019 Clear Channel (renamed iHeart Media in

2014) was operating 858 broadcast radio stations in the United

States with some 250 million monthly listeners,

plus it was one of the world’s largest outdoor advertising

companies with close to one million displays in over

30 countries.

Many Mergers and Acquisitions Are Not Successful Mergers

and acquisitions often do not result in the

hoped-for outcomes. The failure rate of mergers and

acquisitions is between 70 and 90 percent.37 The reasons are

numerous.38 The anticipated revenue growth may not occur.

Cost savings may prove smaller than expected. Gains

in competitive capabilities may take substantially longer to

realize, or worse, never materialize at all. Efforts

to mesh the cultures can be defeated by formidable resistance

from organizational members. Key employees

at the acquired company can become disenchanted with newly

instituted changes and leave. Differences in

management styles and operating procedures can prove hard to

resolve. Personnel at the acquired company may

54. stonewall changes, arguing forcefully for doing certain things

the way they were done prior to the acquisition.

Unsuccessful mergers and acquisitions can be costly. Ford

reportedly lost over $10 billion trying to make successes

of its $2.5 billion acquisition of Jaguar (1989) and $2.7 billion

acquisition of Land Rover (2000); frustrated by

poor results, Ford sold the operations of both brands to India’s

Tata Motors in 2008 for $2.3 billion.39 Bank of

America’s supposedly bargain-priced $2.5 billion acquisition of

ethically challenged and financially troubled

Countrywide Financial in January 2008 was, according to a

prominent banking and finance professor, “the worst

deal in the history of American finance. Hands down.”40

Countrywide, a big originator of questionable subprime

and adjustable-rate mortgages that helped trigger the Fall 2008

collapse of the housing market, cost Bank of

America almost $57 billion in real estate losses, settlements

with federal and state agencies for selling toxic

mortgage loans that were falsely represented as quality

investments, and payments for legal fees.41 Google’s

$12.5 billion acquisition of struggling smartphone manufacturer

Motorola Mobility in 2012 turned out to be

minimally beneficial in helping to “supercharge Google’s

Android ecosystem” (Google’s stated reason for

making the acquisition). When Google’s efforts to rejuvenate

Motorola’s smartphone business by spending over

$1.3 billion on new product R&D and revamping Motorola’s

product line resulted in disappointing sales and

huge operating losses, Google sold Motorola Mobility to China-

based PC maker, Lenovo, for $2.9 billion in

2014 (however, Google retained ownership of Motorola’s

extensive patent portfolio).

56. needs a production strategy geared to top-notch

quality and product performance, and a marketing strategy

aimed at touting differentiating features and using

advertising and a trusted brand name to “pull” sales through the

chosen distribution channels.

Beyond general prescriptions, it is difficult to say just what the

content of the different functional-area strategies

should be without first knowing what higher-level strategic

choices a company has made, the industry environment

in which it operates, the valuable resources and capabilities that

can be leveraged, and so on. Suffice it to say here

that lower-ranking company personnel who have strategy-

making responsibilities must be clear about which

higher-level strategies top executives have chosen and then

must tailor the company’s functional-area strategies

accordingly.

Timing a Company’s Strategic Moves

When to make a strategic move is often as crucial as what move

to make. Timing is especially important when

first-mover advantages or disadvantages exist.42 Being first to

initiate a strategic move can have a high payoff

when:

n Pioneering helps build a firm’s image and reputation with

buyers and creates strong brand loyalty.

n An early lead enables a first mover to move down

the learning curve ahead of rivals and gain an

absolute cost advantage over rivals because

of greater experience in working with new

technologies or because it captures economies

of scale sooner and enjoys volume-based cost

advantages.

58. pioneer may be able to reap temporary monopoly

benefits—such as faster recovery of its initial investment and

good profits—until rivals are able to enter the same

market space. The bigger the first-mover advantages, the more

attractive making the first move becomes and the

more difficult it becomes for later movers to dislodge the

advantages.43

To sustain any advantage that may initially accrue to a pioneer,

a first mover must be a fast learner and continue

to move aggressively to capitalize on any initial pioneering

advantage. It helps immensely if the first mover

has deep financial pockets, important competences and

competitive capabilities, and astute managers. If a first-

mover’s skills, know-how, and actions are easily copied or even

surpassed, then followers and even late movers

can catch or overtake the first mover in a relatively short

period. What makes being a first mover strategically

important is not being the first company to do something but

rather being the first competitor to put together

the precise combination of features, customer value, and sound

revenue/cost/profit economics that gives it an

edge over rivals in battling for market leadership.44 If the

marketplace quickly takes to a first mover’s innovative

product offering, a first mover must have large-scale

production, marketing, and distribution capabilities if it is to

stave off fast followers who possess competitively valuable

resources and capabilities. In cases where technology

advances at a torrid pace, a first mover cannot hope to sustain

an early lead without having strong capabilities in

R&D, design, and new product development, along with the

financial strength to fund these activities.

Sometimes, though, markets are slow to accept the innovative

product offering of a first mover, in which case

a fast follower with substantial resources and marketing muscle

59. can overtake a first mover (as Fox News has

done in competing against CNN to become the leading cable

news network). Sometimes furious technological

change or product innovation makes a first mover vulnerable to

quickly appearing next-generation technology

or products. For instance, former market leaders in cell phones

Nokia and BlackBerry have been victimized

by Apple’s far more innovative iPhone models and new

Samsung smart phones based on Google’s Android

operating system. Hence, there are no guarantees that a first

mover can sustain an early competitive advantage.45

The Potential for Late-Mover Advantages or First-Mover

Disadvantages

There are times, however, when being an adept follower rather

than a first mover actually has its advantages.

Such late-mover advantages (or first-mover disadvantages) arise

in five instances:

n When pioneering leadership is more costly than imitating

followership, and only negligible experience

or learning-curve benefits accrue to the leader—a condition that

allows imitative followers to (1) quickly

catch up to a first mover by learning from its experience and

avoiding its mistakes and (2) achieve lower

costs than the first mover.

n When an innovator’s products are somewhat primitive and do

not live up to buyer expectations, thus

allowing a clever follower with better-performing “next-

generation” products to win disenchanted

buyers away from the leader.

n When buyers are skeptical about the benefits of a new

technology or product being pioneered by a first

mover, thus allowing late movers to wait until the needs of

61. the-world markets are almost never the pioneers

that gave birth to brand-new markets—first-mover advantages

are fleeting and there is time for resourceful fast

followers and sometimes even late movers to overtake the early

leaders.46

The first lesson here is that there is a market-penetration curve

for every emerging opportunity; typically, the

curve has an inflection point at which all pieces of the business

model fall into place, buyer demand explodes,

and the market takes off. The inflection point can come early on

a fast-rising curve (like use of e-mail and

watching movies streamed over the Internet) or further on up a

slow-rising curve (as with battery-powered motor

vehicles, solar and wind power, and digital textbooks for

college students). The second lesson is that the timing

of strategic moves matters, which makes it important for

company strategists to be aware of the nature of first-

mover advantages and disadvantages and the conditions

favoring each type of move.

Key Points

Once a company has selected which of the five basic

competitive strategies to employ in its quest for competitive

advantage, it must decide whether and how to supplement its

choice of a basic competitive strategy approach,

as shown in Figure 6.1.

Companies have a number of offensive strategy options for

improving their market positions and trying to

secure a competitive advantage: offering an equal or better

product at a lower price, leapfrogging competitors by

being the first to adopt next-generation technologies or the first

to introduce next-generation products, pursuing

sustained product innovation, attacking competitors’

63. company’s exclusive channel for accessing customers.

Outsourcing pieces of the value chain formerly performed in-

house can enhance a company’s competitiveness

whenever (1) an activity can be performed better or more

cheaply by outside specialists; (2) the activity is not

crucial to the firm’s ability to achieve sustainable competitive

advantage and won’t weaken its ability to be a

master of its own destiny by hollowing out the competitive

power of its internal resources and capabilities;

(3) it reduces the company’s risk exposure to changing

technology and/or changing buyer preferences; (4) it

streamlines company operations in ways that improve

organizational flexibility, cut cycle time, speed decision

making, and reduce coordination costs; and/or (5) it allows a

company to concentrate on its core business and

do what it does best.

Vertically integrating forward or backward makes strategic

sense only if it strengthens a company’s position via

either cost reduction or creation of a value-enhancing,

differentiation-based advantage. Otherwise, the drawbacks

of vertical integration (increased investment, greater business

risk, increased vulnerability to technological

changes, and less flexibility in making product changes in

response to shifting buyer preferences) are likely to

outweigh any advantages.

Many companies are using strategic alliances, collaborative

partnerships, and joint ventures to help them in

the race to build a global market presence or be a leader in the

industries of the future. These forms of strategic

cooperation with other companies can be an attractive, flexible,

and often cost-effective means by which

companies can gain access to missing technology, expertise, and

business capabilities.

64. Mergers and acquisitions are another attractive strategic option

for strengthening a firm’s competitiveness. When

the operations of two companies are combined via merger or

acquisition, the new company’s competitiveness

can be enhanced in any of several ways: lower costs; stronger

technological skills; more or better competitive

capabilities; a more attractive lineup of products and services;

wider geographic coverage; and/or greater

financial resources with which to invest in R&D, add capacity,

or expand into new areas.

Once all the higher-level strategic choices have been made,

company managers can turn to the task of crafting

functional and operating-level strategies to flesh out the details

of the company’s overall business and competitive

strategy.

The timing of strategic moves also has relevance in the quest

for competitive advantage. Company managers are

obligated to carefully consider the advantages or disadvantages

that attach to being a first mover versus a fast

follower versus a wait-and-see late mover.

chapter 6Supplementing the Chosen Competitive Strategy—

Other Important Strategy ChoicesGoing on the Offensive—

Strategic Options to Improve a Company’s Market

PositionCORE CONCEPTChoosing the Basis for Competitive

AttackCORE CONCEPTBlue Ocean Strategy—A Special Kind

of OffensiveChoosing Which Rivals to AttackDefensive

Strategies—Protecting Market Position and Competitive

AdvantageCORE CONCEPTWebsite StrategiesProduct

Information–Only Strategies—Avoiding Channel

ConflictWebsite Sales as a Minor Distribution ChannelBrick-

and-Click StrategiesStrategies for Online

EnterprisesOutsourcing StrategiesCORE CONCEPTThe Big

Risk of Outsourcing Value Chain ActivitiesVertical Integration