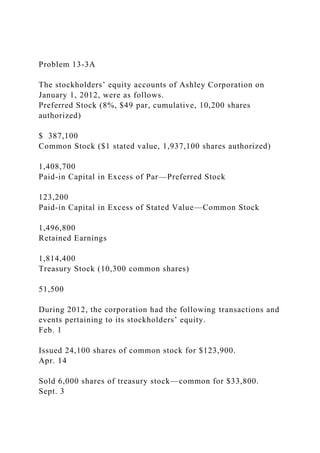

Problem 13-3A

The stockholders’ equity accounts of Ashley Corporation on January 1, 2012, were as follows.

Preferred Stock (8%, $49 par, cumulative, 10,200 shares authorized)

$ 387,100

Common Stock ($1 stated value, 1,937,100 shares authorized)

1,408,700

Paid-in Capital in Excess of Par—Preferred Stock

123,200

Paid-in Capital in Excess of Stated Value—Common Stock

1,496,800

Retained Earnings

1,814,400

Treasury Stock (10,300 common shares)

51,500

During 2012, the corporation had the following transactions and events pertaining to its stockholders’ equity.

Feb. 1

Issued 24,100 shares of common stock for $123,900.

Apr. 14

Sold 6,000 shares of treasury stock—common for $33,800.

Sept. 3

Issued 5,100 shares of common stock for a patent valued at $35,700.

Nov. 10

Purchased 1,100 shares of common stock for the treasury at a cost of $5,700.

Dec. 31

Determined that net income for the year was $456,600.

No dividends were declared during the year.

(a)

Journalize the transactions and the closing entry for net income. (Credit account titles are automatically indented when amount is entered. Do not indent manually.)

Date

Account Titles and Explanation

Debit

Credit

Feb. 1

Apr. 14

Sept. 3

Nov. 10

Dec. 31

Click if you would like to Show Work for this question:

Open Show Work

LINK TO TEXT

LINK TO TEXT

LINK TO TEXT

LINK TO TEXT

LINK TO TEXT

.

Problem 13-3AThe stockholders’ equity accounts of Ashley Corpo.docx

1. Problem 13-3A

The stockholders’ equity accounts of Ashley Corporation on

January 1, 2012, were as follows.

Preferred Stock (8%, $49 par, cumulative, 10,200 shares

authorized)

$ 387,100

Common Stock ($1 stated value, 1,937,100 shares authorized)

1,408,700

Paid-in Capital in Excess of Par—Preferred Stock

123,200

Paid-in Capital in Excess of Stated Value—Common Stock

1,496,800

Retained Earnings

1,814,400

Treasury Stock (10,300 common shares)

51,500

During 2012, the corporation had the following transactions and

events pertaining to its stockholders’ equity.

Feb. 1

Issued 24,100 shares of common stock for $123,900.

Apr. 14

Sold 6,000 shares of treasury stock—common for $33,800.

Sept. 3

2. Issued 5,100 shares of common stock for a patent valued at

$35,700.

Nov. 10

Purchased 1,100 shares of common stock for the treasury at a

cost of $5,700.

Dec. 31

Determined that net income for the year was $456,600.

No dividends were declared during the year.

(a)

Journalize the transactions and the closing entry for net

income. (Credit account titles are automatically indented when

amount is entered. Do not indent manually.)

Date

Account Titles and Explanation

Debit

Credit

Feb. 1