Download as PDF, PPTX

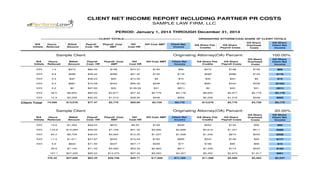

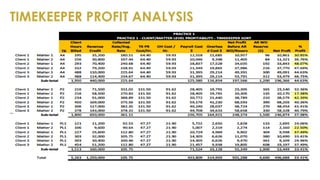

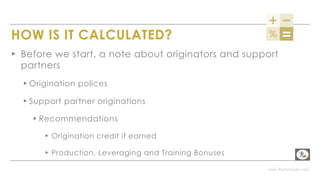

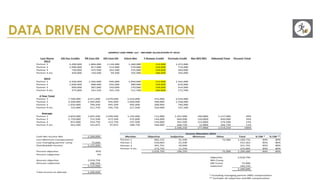

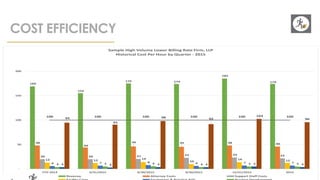

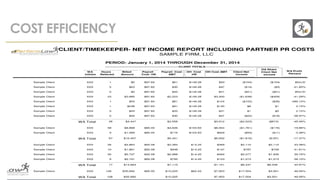

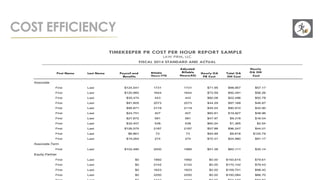

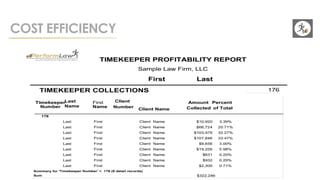

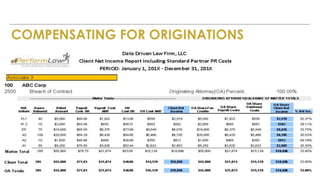

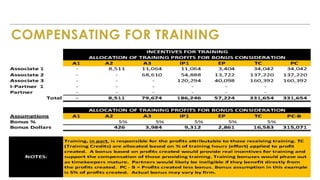

The document provides an in-depth analysis of client profitability, covering reliable methods for calculating profitability, the use of data for pricing, staffing efficiency, and overhead control. It discusses strategies for compensation linked to profitability, including different methodologies for client pricing, and highlights the importance of understanding the cost structures and implications for law firms. Additionally, it addresses challenges and considerations in implementing profitability-focused practices within legal management.