TDS 194Q vs TCS 206C(1H)

•

0 likes•884 views

COMPARISON BETWEEN TDS 194Q VS. TCS 206C(1H) UNDER THE INCOME TAX ACT, 1961. ARE YOU A SELLER OR BUYER.. WHICH ONE IS APPLICABLE ON YOU ?

![TDS u/s 194Q = 0.1%* of [Total

Purchases (Minus) ₹ 50 Lakhs]

* In non-PAN/ Aadhaar cases, the

rate shall be 5%.

TCS u/s 206(1H) = 0.1% of [Total

Sale Receipt (Minus) ₹ 50 Lakhs]

*In non-PAN/ Aadhaar cases, the rate

shall be 1%

Presented By CA AMITOZ SINGH](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recommended

More Related Content

What's hot

What's hot (20)

Similar to TDS 194Q vs TCS 206C(1H)

Similar to TDS 194Q vs TCS 206C(1H) (20)

Recently uploaded

Recently uploaded (20)

TDS 194Q vs TCS 206C(1H)

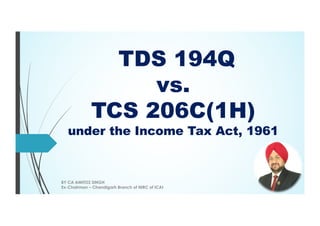

- 1. TDS 194Q vs. TCS 206C(1H) under the Income Tax Act, 1961 BY CA AMITOZ SINGH Ex-Chairman – Chandigarh Branch of NIRC of ICAI

- 2. TDS u/s 194Q = 0.1%* of [Total Purchases (Minus) ₹ 50 Lakhs] * In non-PAN/ Aadhaar cases, the rate shall be 5%. TCS u/s 206(1H) = 0.1% of [Total Sale Receipt (Minus) ₹ 50 Lakhs] *In non-PAN/ Aadhaar cases, the rate shall be 1% Presented By CA AMITOZ SINGH

- 3. Which Section is applicable on you ? TDS 194Q or TCS 206C(1H) ? To know that we need to know who are you – Purchaser or Seller ? Presented By CA AMITOZ SINGH

- 4. Are you a Purchaser ? - YES Presented By CA AMITOZ SINGH Was your turnover more than Rs. 10 Crores in preceding year - YES Do you have purchases more than Rs. 50 lakhs from Single Seller - YES Purchaser Saheb, Go Ahead – DEDUCT TDS u/s 194Q @ 0.1%*

- 5. Are you a Purchaser ? - YES Presented By CA AMITOZ SINGH Was your turnover more than Rs. 10 Crores in preceding year - YES Do you have purchases more than Rs. 50 lakhs from Single Seller - NO Purchaser Saheb, Chill and Relax NO TDS and No TCS

- 6. Are you a Seller ? - YES Presented By CA AMITOZ SINGH Was your turnover more than Rs. 10 Crores in preceding year - YES Do you have collection of more than Rs. 50 lakhs from Single purchaser - YES Seller Saheb, no TCS to be collected Your Purchaser will DEDUCT TDS u/s 194Q @ 0.1% Is your purchaser having turnover of more than Rs. 10 Crores in preceding year - YES

- 7. Are you a Seller ? - YES Presented By CA AMITOZ SINGH Was your turnover more than Rs. 10 Crores in preceding year - YES Do you have collection of more than Rs. 50 lakhs from Single purchaser - YES Seller Saheb, collect TCS u/s 206C(1H) @ 0.1% Your Purchaser will NOT DEDUCT TDS Is your purchaser having turnover of more than Rs. 10 Crores in preceding year - NO

- 8. Are you a Seller ? - YES Presented By CA AMITOZ SINGH Was your turnover more than Rs. 10 Crores in preceding year - YES Do you have collection of more than Rs. 50 lakhs from Single purchaser - NO Seller Saheb, Chill and Relax NO TDS and No TCS

- 9. Who will win in case of fight between 194Q and 206C(1H) ? Presented By CA AMITOZ SINGH It has been specified under second proviso to Section 206C(1H) that if TDS u/s 194Q is applicable then TCS u/s 206C(1H) will not be applicable. So, TDS u/s 194Q will win the fight.

- 10. Process to be followed ? Presented By CA AMITOZ SINGH As a eligible buyer: – It will be your responsibility. So deduct TDS u/s 194Q. As a eligible seller: Take a declaration from your buyers that they will deduct TDS u/s 194Q and comply the same, else you need to charge TCS if buyers are not eligible or no such declaration is received or no such treatment is given by your buyers.

- 11. Presented By CA AMITOZ SINGH Effective date ? Under Section 194Q - 01/07/2021 Under Section 206C(1H) - Already Applicable from 01/10/2020 Both the Provisions will apply only in the case where Buyer and Seller both are Resident, if one of them is Non-Resident then these Provisions will not Apply.

- 12. Presented By CA AMITOZ SINGH Effects on Advance Payments ? Under Section 194Q - TDS to be Deducted on Advance Payments made for the purchase of Goods Under Section 206C(1H) - If the buyer is deducting TDS, then TCS is not required to collect.

- 13. Presented By CA AMITOZ SINGH Is TDS u/s 194Q applicable on purchase of capital goods? “Goods” as per CGST Act 2017 means any kind of movable property other than services. Thus TDS u/s 194Q is applicable on purchase of capital goods.

- 14. Presented By CA AMITOZ SINGH Is TDS u/s 194Q applicable on Import Purchases as well? No, Since the provision of section 194Q, are applicable when a Buyer is responsible for paying any sum to any resident seller for purchase of any goods. TDS u/s 194Q is not to be deducted from Import purchases.

- 15. Presented By CA AMITOZ SINGH What if buyer fails to deduct TDS u/s 194Q? As per Section 40a(ia) – If buyer fails to deduct and deposit TDS, purchase expenditure to the extent of 30% will be disallowed and shall be subject to Income Tax at applicable tax rate.

- 16. Presented By CA AMITOZ SINGH CBDT vide Circular No. 17 of 2020, clarified that provisions of Section 206C(1H) shall not be applicable in relation to transactions in securities (and commodities) which are traded through recognised stock exchanges or cleared and settled by the recognised clearing corporation, including recognised stock exchanges or recognised clearing corporations located in International Financial Service Centre (IFSC). Applying the rationale behind such clarification, it is inferred that the CBDT may allow a similar exemption from TDS under Section 194Q as well.

- 17. Presented By CA AMITOZ SINGH Particulars 194Q 206C(1H) Purpose Tax to be DEDUCTED Tax to be COLLECTED Applicable To Buyer / Purchaser Seller With Effect from 1st July 2021 1st October, 2020 When Deducted or Collected Payment or credit, whichever is earlier At the time of Receipt Advances TDS shall be deducted on advance payments made TCS shall be collected on advance receipts Rate of TDS/TCS 0.1% 0.1% (0.075% for FY 2020-21 PAN Not Available 5% 1% Comparison of Sec 194Q and 206C(1H) of Income Tax Act, 1961

- 18. Presented By CA AMITOZ SINGH Particulars 194Q 206C(1H) Triggering Point Turnover / Gross Receipts / Sales from the business of BUYER should exceed Rs.10 crore during previous year (Excluding GST) Purchase of goods of aggregate value exceeding Rs. 50 Lakhs in P.Y. (The value of goods includes GST) Turnover / Gross Receipts / Sales from the business of SELLER should exceed Rs.10 crore during previous year (Excluding GST) Sale consideration received exceeds Rs.50 Lakhs in P.Y. (The value of goods includes GST) Comparison of Sec 194Q and 206C(1H) of Income Tax Act, 1961

- 19. Presented By CA AMITOZ SINGH Particulars 194Q 206C(1H) Exclusions Yet to be notified by government If Buyer is- Importer of goods Central/State Government, Local Authority An embassy, High Commission, legation, commission, consulate and trade representation of a foreign state. Comparison of Sec 194Q and 206C(1H) of Income Tax Act, 1961

- 20. Presented By CA AMITOZ SINGH Particulars 194Q 206C(1H) When to Deposit / Collect Tax so deducted shall be deposited with government by 7th day of subsequent month Tax so collected shall be deposited with government by 7th day of subsequent month Quarterly Statement to be filed 26Q 27EQ Certificate to be issued to Seller / Buyer Form 16A Form 27D Comparison of Sec 194Q and 206C(1H) of Income Tax Act, 1961

- 21. Presented By CA AMITOZ SINGH ILLUSTRATIONS: Turnover of Seller (in Crores) 11 11 9 Turnover of Buyer (in Crores) 9 9 11 Amt. recd. or paid for sales or purchase of Goods in previous year (in Lakhs) 55 55 55 Taxable Amount 5 5 5 Whether PAN Available Buyer PAN Available Buyer PAN Not Available Seller PAN Available TDS or TCS TCS @ 0.1% TCS @ 1% TDS @ 0.1% Liable Person Seller Seller Buyer Applicable Section 206C(1H) 206C(1H) 194Q Excluded Section 194Q 194Q 206C(1H) Explanation Buyer Turnover < Rs. 10 Cr. Buyer Turnover < than Rs. 10 Cr. Seller Turnover < Rs. 10 Cr.

- 22. Presented By CA AMITOZ SINGH ILLUSTRATIONS: Turnover of Seller (in Crores) 9 11 11 Turnover of Buyer (in Crores) 11 11 11 Amt. recd. or paid for sales or purchase of Goods in previous year (in Lakhs) 55 55 55 Taxable Amount 5 5 5 Whether PAN Available Seller PAN Not Available Seller PAN Available Seller PAN Not Available TDS or TCS TDS @ 5% TDS @ 0.1% TDS @ 5% Liable Person Buyer Buyer Buyer Applicable Section 194Q & 206AA 194Q 194Q & 206AA Excluded Section 206C(1H) 206C(1H) 206C(1H) Explanation Seller Turnover < Rs. 10 Cr. Exclusion u/s 206C(1H) Exclusion u/s 206C(1H)

- 23. THANK YOU CA Amitoz Singh Kamboj Partner APT & Co LLP , Chartered Accountants Plot no. 1632, Sector 82 – JLPL Industrial Area, Mohali Plot No. 181/33, Indl Area 1, Chandigarh Ex-Chairman (2020-21) Chandigarh Branch (NIRC) of The Institute of Chartered Accountants of India |M| +91 987 202 7526, +91 936 900 0007 |E| ca.amitozsingh@gmail.com |W| www.aptllp.com Disclaimer: Though full efforts have been made to state the interpretations of law correctly, this write up is not intended to be a professional advice to anyone, therefore neither the Author nor the Organization accepts any responsibility whatsoever and hence no liability can arise for any losses, claims or due to the contents of this write up.