QNBFS Daily Technical Trader Qatar - September 07, 2023 التحليل الفني اليومي ...

5 February Daily market report

1. Page 1 of 7

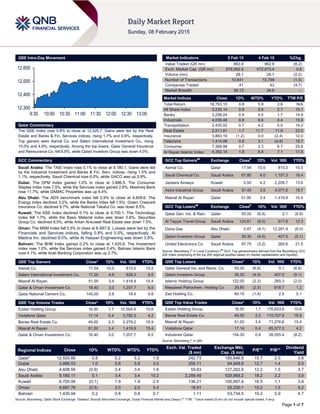

QSE Intra-Day Movement

Qatar Commentary

The QSE Index rose 0.8% to close at 12,520.7. Gains were led by the Real

Estate and Banks & Fin. Services indices, rising 1.7% and 0.9%, respectively.

Top gainers were Aamal Co. and Salam International Investment Co., rising

10.0% and 4.9%, respectively. Among the top losers, Qatar General Insurance

and Reinsurance Co. fell 6.8%, while Qatari Investors Group was down 4.0%.

GCC Commentary

Saudi Arabia: The TASI Index rose 0.1% to close at 9,180.1. Gains were led

by the Industrial Investment and Banks & Fin. Serv. indices, rising 1.5% and

1.1%, respectively. Saudi Chemical rose 6.0%, while GACO was up 5.9%.

Dubai: The DFM Index gained 1.0% to close at 3,886.5. The Consumer

Staples index rose 7.5%, while the Services index gained 2.8%. Mashreq Bank

rose 11.7%, while DAMAC Properties was up 9.4%.

Abu Dhabi: The ADX benchmark index fell 0.9% to close at 4,608.6. The

Energy index declined 3.2%, while the Banks index fell 1.5%. Green Crescent

Insurance Co. declined 9.7%, while National Takaful Co. was down 8.5%.

Kuwait: The KSE Index declined 0.1% to close at 6,700.1. The Technology

index fell 1.7%, while the Basic Material index was down 0.6%. Securities

Group Co. declined 8.5%, while Arkan Al-kuwait Real Estate was down 7.5%.

Oman: The MSM Index fell 0.5% to close at 6,687.8. Losses were led by the

Financials and Services indices, falling 0.8% and 0.5%, respectively. Al

Madina Inv. declined 8.0%, while Al Hassan Engineering was down 3.8%.

Bahrain: The BHB Index gained 0.2% to close at 1,435.9. The Investment

index rose 1.0%, while the Services index gained 0.4%. Bahrain Islamic Bank

rose 4.1%, while Arab Banking Corporation was up 2.7%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Aamal Co. 17.54 10.0 815.0 15.5

Salam International Investment Co. 17.20 4.9 928.3 8.5

Masraf Al Rayan 51.00 3.4 1,419.9 15.4

Qatar & Oman Investment Co. 16.40 3.0 1,207.7 6.5

Qatar National Cement Co. 145.00 2.8 18.4 9.8

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 16.50 1.7 10,504.4 10.6

Vodafone Qatar 17.14 0.4 3,782.3 4.2

Barwa Real Estate Co. 49.00 2.3 2,279.2 16.9

Masraf Al Rayan 51.00 3.4 1,419.9 15.4

Qatar & Oman Investment Co. 16.40 3.0 1,207.7 6.5

Market Indicators 5 Feb 15 4 Feb 15 %Chg.

Value Traded (QR mn) 883.9 962.6 (8.2)

Exch. Market Cap. (QR mn) 676,062.5 672,073.4 0.6

Volume (mn) 28.1 28.7 (2.2)

Number of Transactions 10,641 10,798 (1.5)

Companies Traded 41 43 (4.7)

Market Breadth 26:13 34:6 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,793.10 0.8 5.9 2.6 N/A

All Share Index 3,235.14 0.9 5.6 2.7 15.1

Banks 3,258.24 0.9 4.5 1.7 14.9

Industrials 4,055.48 0.8 6.6 0.4 13.8

Transportation 2,435.02 0.7 4.2 5.0 14.2

Real Estate 2,511.81 1.7 11.7 11.9 22.0

Insurance 3,863.19 (1.2) 0.0 (2.4) 12.0

Telecoms 1,414.06 0.8 3.1 (4.8) 18.7

Consumer 7,368.98 0.7 3.3 6.7 29.6

Al Rayan Islamic Index 4,392.14 1.8 8.8 7.1 17.8

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Aamal Co. Qatar 17.54 10.0 815.0 15.5

Saudi Chemical Co. Saudi Arabia 67.80 6.0 1,107.3 18.4

Jazeera Airways Kuwait 0.50 4.2 2,209.7 13.6

Astra Industrial Group Saudi Arabia 37.43 3.5 4,077.6 18.7

Masraf Al Rayan Qatar 51.00 3.4 1,419.9 15.4

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Qatar Gen. Ins. & Rein. Qatar 55.00 (6.8) 0.1 (6.8)

Al Tayyar Travel Group Saudi Arabia 133.61 (6.0) 917.9 12.3

Dana Gas Abu Dhabi 0.47 (4.1) 12,291.9 (6.0)

Qatari Investors Group Qatar 39.30 (4.0) 407.5 (5.1)

United Electronics Co. Saudi Arabia 97.75 (3.2) 260.6 21.5

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar General Ins. and Reins. Co. 55.00 (6.8) 0.1 (6.8)

Qatari Investors Group 39.30 (4.0) 407.5 (5.1)

Islamic Holding Group 122.00 (2.3) 265.3 (2.0)

Mesaieed Petrochem. Holding Co. 29.85 (2.0) 818.7 1.2

Zad Holding Co. 84.10 (1.4) 2.5 0.1

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Ezdan Holding Group 16.50 1.7 176,653.6 10.6

Barwa Real Estate Co. 49.00 2.3 110,707.8 16.9

Masraf Al Rayan 51.00 3.4 71,276.6 15.4

Vodafone Qatar 17.14 0.4 65,077.3 4.2

Industries Qatar 154.30 0.8 39,055.4 (8.2)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,520.66 0.8 5.2 5.2 1.9 242.73 185,646.8 15.7 2.0 3.8

Dubai 3,886.53 1.0 5.8 5.8 3.0 255.11 94,949.9 12.7 1.4 5.0

Abu Dhabi 4,608.56 (0.9) 3.4 3.4 1.8 59.83 127,262.9 12.2 1.5 3.7

Saudi Arabia 9,180.11 0.1 3.4 3.4 10.2 2,289.45 528,968.2 18.2 2.2 3.0

Kuwait 6,700.06 (0.1) 1.9 1.9 2.5 136.21 100,897.4 16.5 1.1 3.8

Oman 6,687.76 (0.5) 2.0 2.0 5.4 18.91 25,230.1 10.2 1.5 4.2

Bahrain 1,435.94 0.2 0.8 0.8 0.7 1.11 53,734.5 10.2 0.9 4.7

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,300

12,400

12,500

12,600

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 7

Qatar Market Commentary

The QSE Index rose 0.8% to close at 12,520.7. The Real Estate

and Banks & Financial Services indices led the gains. The index

rose on the back of buying support from non-Qatari shareholders

despite selling pressure from Qatari shareholders.

Aamal Co. and Salam International Investment Co. were the top

gainers, rising 10.0% and 4.9%, respectively. Among the top

losers, Qatar General Insurance and Reinsurance Co. fell 6.8%,

while Qatari Investors Group was down 4.0%.

Volume of shares traded on Thursday fell by 2.2% to 28.1mn

from 28.7mn on Wednesday. However, as compared to the 30-

day moving average of 13.8mn, volume for the day was 102.5%

higher. Ezdan Holding Group and Vodafone Qatar were the most

active stocks, contributing 37.4% and 13.5% to the total volume

respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn) 4Q2014

% Change

YoY

Operating Profit

(mn) 4Q2014

% Change

YoY

Net Profit (mn)

4Q2014

% Change

YoY

Abdullah A. M. Al-Khodari

Sons Co. (ALKHODARI)*

Saudi Arabia SR – – 64.0 -34.3% 101.2 57.3%

Jarir Marketing Co. (JMC)* Saudi Arabia SR – – 726.8 12.2% 745.4 14.1%

Aramex Dubai AED 959.0 12.8% – – 89.4 17.0%

National General Insurance

Co. (NIC)*

Dubai AED 317.6 3.9% 20.1 -47.7% 79.6 -36.3%

Insurance House (IH)* Abu Dhabi AED 85.0 1.8% -9.1 NA -20.9 NA

Dana Gas* Abu Dhabi AED 2,504.0 4.8% – – 457.0 -20.0%

Emirates Insurance Co.

(EIC)*

Abu Dhabi AED 798.7 14.9% 51.6 -14.9% 103.4 20.6%

Ras Al Khaimah Poultry &

Feeding Co. (RAPCO)*

Abu Dhabi AED 52,178.0 209.3% – – – –

Raysut Cement* Oman OMR 94.3 1.1% – – 27.4 -0.4%

Source: Company data, DFM, ADX, MSM (* FY2014 results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

02/05 US Challenger, Gray & Chr. Challenger Job Cuts YoY January 17.60% – 6.60%

02/05 US IPSOS Public Affairs RBC Consumer Outlook Index February 54.7 – 53.3

02/06 US Bureau of Labor Stat. Unemployment Rate January 5.70% 5.60% 5.60%

02/05 EU Markit Eurozone Retail PMI January 46.6 – 47.6

02/05 France Markit France Retail PMI January 44.0 – 46.5

02/05 Germany Deutsche Bundesbank Factory Orders MoM December 4.20% 1.50% -2.40%

02/05 Germany Markit Germany Construction PMI January 49.5 – 50.5

02/05 Germany Markit Germany Retail PMI January 52.3 – 51.7

02/06 Germany Deutsche Bundesbank Industrial Production SA MoM December 0.10% 0.40% 0.10%

02/06 Germany BMWi Industrial Production WDA YoY December -0.70% -0.30% -0.30%

02/05 UK Lloyds TSB Halifax House Prices MoM January 2.00% 0.00% 1.10%

02/05 UK Lloyds TSB Halifax House Price 3Mths/Year January 8.50% 7.70% 7.80%

02/06 UK ONS Visible Trade Balance GBP/Mn December -£10,154 -£9,100 -£9,283

02/06 UK ONS Trade Balance Non EU GBP/Mn December -£3,796 -£3,000 -£2,778

02/06 UK ONS Trade Balance December -£2,895 -£1,700 -£1,841

02/06 Spain INE Industrial Output NSA YoY December 2.10% – -0.50%

02/06 Spain INE Industrial Output SA YoY December -0.90% 0.30% -0.30%

02/05 Italy Markit Italy Retail PMI January 41.2 – 42.8

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 63.29% 63.51% (1,910,119.22)

Non-Qatari 36.71% 36.49% 1,910,119.22

3. Page 3 of 7

News

Qatar

QGRI reports QR919.7mn net profit in FY2014 – Qatar

General Insurance & Reinsurance Company (QGRI) reported a

net profit of QR919.7mn in FY2014 versus QR2.1bn in FY2013.

EPS amounted to QR13.30 in FY2014 as compared to QR30.80

in FY2013. Meanwhile, the company’s board of directors

recommended a distribution of 20% cash dividend

(QR2.00/share) and a distribution of 15% bonus shares of the

share capital. QGRI’s General Assembly will be held on March

15, 2015, whereas the alternative meeting will be held on March

22, 2015. (QSE)

Qatar’s money supply rebounds in December 2014 – The

total money supply (M1) in Qatar rebounded by QR124bn in

December 2014. The country’s average movement in money

supply (M2) grew by QR504bn in December 2014. M1

measures the most liquid components of the money supply,

while M2 includes savings deposits, money market mutual funds

and other time deposits, which are less liquid. (Peninsula Qatar)

CBQK, KCBK extend QR1.26bn financing for Rayyan Road

project – The Commercial Bank of Qatar (CBQK) and Al Khalij

Commercial Bank (KCBK) have concluded a combined financing

arrangement of QR1.26bn. The contract financing facility is for

the construction and development of the Al Rayyan Road

project, which is awarded to the joint venture between Dogus

Construction and Onur Taahhut Taşımacılık ve Ticaret Ltd.

CBQK and KCBK are financing the QR3.43bn project on a

mutual basis, in which both banks are the joint mandate lead

arrangers, while CBQK is acting as the facility and security

agent. (QSE)

QNB Group asset management wins ‘Qatar Equity Fund of

the Year’ award – QNB Group’s (QNBK) asset management

services has won the “Qatar Equity Fund of the Year” award in

recognition of its Al-Watani Fund during the MENA Fund

Manager Performance Awards Ceremony held recently in

Dubai. The award reflects the excellence achieved by QNBK’s

asset management services across its domestic and

international network of operations. (Gulf-Times.com)

QIBK to hold AGM on February 22 – Qatar Islamic Bank

(QIBK) has scheduled its Ordinary General Assembly Meeting

(AGM) to be held on February 22, 2015 and has announced the

agenda for it. QIBK’s AGM will discuss the board of directors’

recommendation to distribute 42.5% cash dividends (QR4.25

per share). The AGM will also discuss and approve the

company’s balance sheet and profit & loss for the year ended

December 31, 2014 as well as QIBK’s future plan. (QSE)

DOHI to hold AGM, EGM on March 3 – Doha Insurance

Company (DOHI) has scheduled its Ordinary and Extraordinary

General Assembly Meeting (AGM and EGM) to be held on

March 3, 2015 and has announced the agenda for it. The AGM

will discuss and approve bank’s balance sheet and profit & loss

for the year ended December 31, 2014 as well as the board of

directors’ proposal to distribute cash dividends of 10% (QR1 per

share). Meanwhile, the agenda of the EGM is to amend the

paragraph (1) article (66) of the Article of Association of the

Company, allowing the company to allocate at least 10% of its

annual net profit to increase the legal reserve to 100% of the

paid-up capital. The legal reserve is not available for distribution.

However, it is allowed, after obtaining approval from Qatar

Central Bank, to distribute up to 5% as dividends from the

balance of the reserve that are more than 100% of the paid-up

capital, in the years that the company did not achieve sufficient

profit. (QSE)

Al Sharq: 266 non-energy projects to create 12,000 jobs – Al

Sharq reported that Qatar’s Ministry of Energy & Industry (MoEI)

has issued 266 licenses for non-hydrocarbon manufacturing

projects in 2014, giving a big boost to the country’s economic

diversification efforts. These projects are expected to create

around 12,000 jobs. Al Balagh Trading & Contracting

Company’s Chairman, Sherida Al Ka’abi said that non-energy

industries have been growing and hold a share of over 10% in

the nation’s GDP. Total investment in the non-oil industrial

sector in 2014 reached QR17.3bn, including new projects. He

said non-hydrocarbon industries are being given more emphasis

to transform the country into a diversified and more sustainable

economy. Al Ka’abi said while Qatar’s economy is steadily

moving toward diversification, the oil & gas sector remains the

key driver of the economy. (Peninsula Qatar)

Amwal plans QR100mn private equity fund – Doha-based

Amwal’s CEO, Fahmi Alghussein said that the company is

planning to raise as much as QR100mn for a private equity fund,

as it diversifies beyond stock selection. The firm will target its

new fund at companies with QR20-50mn in annual revenue that

are based in Qatar and Saudi Arabia. Amwal’s fund will focus on

education, healthcare, insurance and consumer-related

industries. (Bloomberg)

Hyundai Glovis signs $100mn shipping contract with QPM –

Hyundai Glovis, Hyundai Motor Group's transportation arm, has

signed a long-term marine shipping contract worth $100mn with

Qatar Primary Materials Company (QPM) to ship construction

aggregate. Under the agreement’s terms, Hyundai Glovis will

carry 12mn tons of aggregates from Fujairah to Mesaieed in

south Qatar for the next two years. The shipments will be used

to build FIFA World Cup stadiums and its associated

infrastructure. (Bloomberg)

International

Strong US job, wage growth open door to mid-year rate

hike; Budget deficit grows slightly – Job growth in the US

rose solidly in January 2015 and wages rebounded, indicating

an economic strength that could persuade the Federal Reserve

to carry out a mid-year interest rate increase. The US Labor

Department said non-farm payrolls increased 257,000 in

January, outstripping forecasts. Meanwhile, data for November

and December was revised to show 147,000 more jobs were

created than previously reported, bolstering views that

consumers will have enough muscle to carry the economy

through rough seas. At 423,000, November's gain was the

largest for any month since May 2010, when employment was

boosted by government hiring for a national census. Meanwhile,

The Congressional Budget Office (CBO) has forecast a $195bn

US budget deficit for the first four months of the current fiscal

year, up from $183bn YoY. The CBO said the $12bn increase in

the budget gap for the October-January period was largely

driven by lower payments to the US Treasury this year from

government-controlled mortgage finance groups, Fannie Mae

and Freddie Mac. (Reuters)

Canada: World cannot rely on US to lead global economy –

Canadian Finance Minister Joe Oliver said the US is carrying

the world economy at the moment, but that is not sustainable,

and other major nations must shoulder more of the load. Oliver

said that the world economy is off to a rough start in 2015 and

that kick-starting the global growth will be the top agenda at the

upcoming Group of 20 meeting of finance ministers and central

bank chiefs in Turkey. The G20 came into its own during the

2007-09 financial crisis, when it put together a global stimulus

package, but it is now facing the more delicate challenge of

4. Page 4 of 7

arriving at coordinated action when economies are running at

different speeds. (Reuters)

Oil import surge widens UK trade gap, but exports grow –

Britain's trade in goods deficit widened sharply in December due

to a surge in oil imports, making the trade gap for 2014 the

biggest since 2010. There were signs of a shift in trade balance

in 4Q2014, when the goods deficit narrowed by the largest

amount in three years as export volumes rose at their fastest

clip since 2Q2013. However, the overall picture indicates that

the UK economy is heavily reliant on domestic demand. The

Conservative-led government's hopes of exports playing a

greater role in the economy have been frustrated by persistent

weakness in the Eurozone, Britain's largest export market. That

seems unlikely to change before the UK’s national election on

May 7. However, there are signs that exporters are being helped

by the fall in the pound’s value in 2H2014. The Office for

National Statistics said export volumes jumped 2.4% in

December. A recent survey showed the British manufacturing

export order growth reached a five-month high in January.

(Reuters)

Banks slash forex leverage for clients after Swiss franc rout

– International banks are cutting back on the credit they offer to

leveraged investors in foreign exchange (forex), after an

eruption in Swiss franc volatility last month forced changes in

risk-management models. In the aftermath of the Swiss franc's

surge on January 15 – as much as 40% – and the losses that

resulted, the US authorities imposed a 50 times cap on the

leverage that retail currency brokers like FXCM can offer their

clients. That means by putting $1 on a currency swing, the client

actually bets up to $50. The rest is effectively provided on credit

by the broker or the broker's banking partners. No such limits

are put on retail forex trading in Europe, or on the wholesale

market, where the stakes are far higher for banks and funds

betting trillions daily on currency moves. Several sources with

forex trading operations said the impact of the volatility caused

by the Swiss franc meant that banks have to cut the leverage

they offer even to their most trusted clients. (Reuters)

Moody's puts Greek rating on review for downgrade;

Greece wants no more bailout strings – Rating agency

Moody's said that it was placing the Greek government bond

rating of Caa1 on review for downgrade, warning that there was

great uncertainty regarding the result of talks between the

country and its creditors. Leftist Prime Minister Alexis Tsipras

was elected barely two weeks ago on a pledge to renegotiate

the terms of a €240bn bailout, including a promise to write off a

chunk of the country's debt and scrap austerity measures.

Meanwhile, Standard & Poor's cut Greece's long-term sovereign

credit rating to B- from B, warning that liquidity restraints on

Greek banks would limit the time the new government has to

clinch a deal with its creditors. Meanwhile, Greece's new

government, despite isolation in the Eurozone and under

pressure from the European Central Bank (ECB), said it wanted

no more bailout money with strings attached from the European

Union and International Monetary Fund. A government official

said Greece wants permission from the Eurozone to issue more

short-term debt, and to receive profits that the ECB and other

central banks have gained from holding Greek bonds. (Reuters)

China vows to maintain export growth, stabilize imports in

2015 – The Chinese Ministry of Commerce said China's trade

outlook for 2015 is complicated and grim, since the country

needs to work hard to maintain growth in exports and imports

stable. The remarks came ahead of the release of its trade data

for January, when the Chinese export growth is forecast to

soften and imports are predicted to shrink in value. The ministry

said to help the sector, authorities would stabilize China's

imports of raw materials and encourage purchases of consumer

goods and high-tech equipment parts. New business models for

trade companies will be developed and cross-border e-

commerce will be promoted. The export sector, the mainstay

driver of the world's second-largest economy, has floundered in

recent years due to unsteady foreign demand and rising labor

costs that have depressed profit margins. However, the trade

ministry said exports on average still contributed about 18% of

China's overall economic growth and employed 180mn people.

(Reuters)

Regional

IATA: Mideast airlines post 13% traffic growth in 2014 –

According to the International Air Transport Association (IATA),

Middle Eastern carriers had the strongest annual traffic growth

of 13% during 2014, more than double the global average.

Capacity rose 11.9% and the load factor climbed to 78.1%. In

comparison, the international passenger traffic rose just 6.1%

YoY in 2014; capacity rose 6.4% and the load factor slipped to

79.2%. IATA’s Director General & CEO, Tony Tyler said the

demand for the passenger business did well in 2014. With a

5.9% expansion of demand, the industry outperformed the 10-

year average growth rate. Carriers in the Middle East posted

double-digit growth, while results from Africa were barely above

previous-year levels. (Gulftimes.com)

F&S: GCC food retailing to cross AED560bn by 2018 –

According to a recent report by Frost & Sullivan (F&S), the food

retailing market in the GCC region is estimated to be worth

around AED560bn by 2018. Scanty food production, because of

limited water resources and climatic conditions, make GCC

countries dependent on imports for its food requirements.

Around 80% of food products in the GCC are imported; cereals

account for more than a half of the region’s total imports.

Imported foods are locally processed for consumption and re-

exports. According to Ebrahim Mohammad Al Janahi, Deputy

CEO of Jebel Ali Free Zone (JAFZA), this scenario provides

huge opportunities not only for multinationals dealing in variety

of food products, but also for local dealers in food processing

machinery, packaging and logistics. (GulfBase.com)

Ace Arabia gets SAMA’s approval for insurance products –

Ace Arabia Cooperative Insurance Co. (Ace Arabia) has

received the Saudi Arabian Monetary Agency’s (SAMA)

temporary approval for the use of its insurance products for six

months, started from February 4, 2015. (Tadawul)

Saudia signs MoU with SAP – Saudi Arabian Airlines (Saudia)

has signed a MoU with global enterprise software leader SAP to

boost the Kingdom’s economy and employment opportunities.

Saudia will deploy SAP’s Enterprise Resource Planning (ERP)

solutions to small & medium-sized enterprises (SMEs) to cater

to SMEs’ need for boosting their productivity and for the

Kingdom’s workforce to be trained in the latest technology.

(GulfBase.com)

Guidance arranges SR188mn Islamic credit facilities for Al-

Khodari – Guidance Capital Markets Ltd (DIFC) has arranged

SR188mn worth of off-shore, Islamic credit facilities for Abdullah

A. M. Al-Khodari Sons Company (Al-Khodari) from an Abu

Dhabi-based bank. Guidance acted as the sole arranger and

Shari’ah structuring advisor to the company for arranging the

Murabaha facilities, which carry a three-year term, and will be

used for issuance of performance bonds and meeting capex

requirements of one of Al Khodari’s construction projects.

(GulfBase.com)

Abraaj, TPG Capital to acquire majority stake in Kudu –

According to sources, private equity firms Abraaj Group and

5. Page 5 of 7

TPG Capital have signed a deal to purchase a majority stake in

Saudi Arabian fast-food chain, Kudu. Reportedly, the signing

has taken place, paving the way for the formal closing of the

transaction, which still requires regulatory formalities. Kudu has

more than 200 restaurants across the Kingdom and is estimated

to be worth around $400mn. (GulfBase.com)

Jarir Marketing recommends SR166.5mn dividend for

4Q2014 – Jarir Marketing Company’s board of directors has

recommended the distribution of 18.5% dividend (SR1.85 per

share), amounting to SR166.5mn for 4Q2014. Shareholders,

who are registered in the registers of the Securities Depository

Center (Tadawul) on February 17, 2015, will be eligible to

receive the dividend. The dividend will be distributed on

February 26, 2015. (Tadawul)

Jordan sign 5 deals worth $176mn with SFD – The Jordanian

government has signed five financing agreements (grants) with

the Saudi Fund for Development (SFD) worth $176mn as a part

of the Saudi’s $1.25bn commitment under the GCC $5bn grant

to finance development projects in Jordan. (GulfBase.com)

FGB to meet investors for potential bond issue – According

to sources, First Gulf Bank (FGB) is planning to meet fixed

income investors from February 9, 2015 onward for a potential

international bond issue. The bank would issue a bond during

2015, subject to market conditions. The lender has mandated

Deutsche Bank and ING Bank to arrange for the investor

meetings. (Reuters)

EBS signs MoU with CoreBrace for steel braces – Emirates

Building Systems (EBS), a subsidiary of Dubai Investments (DI),

has announced launching a first-of-its-kind steel brace system in

the Middle East. EBS has signed MoU with US-based

CoreBrace to formalize the cooperation on testing and

installation of Buckling-Restrained Braces (BRBs) across the

region, which offer resistance to buildings against seismic risks

and other demanding loads. The demand for this technology is

expected to grow 50% YoY over the next five years. The BRBs

will be initially sourced from CoreBrace’s facility in the US, and

later will be produced at EBS’ high-end manufacturing unit in

Dubai Investments Park (DIP) starting 2Q2015. (DFM)

NGIC proposes 25% cash dividend – National General

Insurance Company’s (NGIC) board of directors has proposed

the distribution of 25% cash dividend. (DFM)

Ajman Bank reports AED71.4mn net profit in FY2014 –

Ajman Bank posted net profit of AED71.4mn in FY2014 versus

AED10.6mn in FY2013. The bank’s net operating income for

FY2014 was amounted to AED357.18mn as compared to

AED251.37mn in FY2013. The bank’s total assets stood at

AED11.23bn at the end of December 2014 as against AED7.1bn

at the end of December 2013. EPS stood at AED0.071 in

FY2014 as compared to AED0.011 in FY2013. Customer

deposits stood at AED8.51bn at the end of December 31, 2014.

Ajman Bank’s board of directors has proposed distribution of 5%

bonus shares equal to the bank’s capital. (DFM)

ASBB net profit surges 25.7% in FY2014, recommends 5 fils

per share cash dividend – Al Salam Bank-Bahrain (ASBB)

reported a net profit of BHD15.55mn in FY2014 as compared to

BHD12.37mn in FY2013. Total operating income grew to

BHD46.1mn in FY2014 against BHD26.1mn in FY2013. EPS

retreated to 8 fils in FY2014 against 8.3 fils during FY2013.

ASBB’s total assets stood at AED1.96bn at the end of

December 2014 as against AED1.09bn at the end of December

2013. Customer’ current accounts stood at BHD226.65mn at the

end of December 31, 2014. Meanwhile, ASBB’s board of

directors has proposed distribution of cash dividend equaling 5

fils per share. (DFM)

Aramex targets 3 acquisitions in 2015 – Aramex company’s

CEO, Hussein Hachem said the company is expecting a 10%

increase in its profits by 2015-end. As part of its expansion

plans, Aramex is also eyeing three new takeovers in 2015 after

completing two acquisitions in 2014 in the Middle East, North

Africa, sub-Saharan Africa and Asia. The company is taking a

ticket of $150mn which can be taken from a consortium of local

banks probably in the next week or 10 days. The company’s

CFO, Bashar Obeid said that banks have showed appetite to

lend Aramex up to $300-$400mn. (GulfBase.com)

Sobha Group to start Phase II of $4bn Dubai project – Sobha

Group has announced that it will break ground on Phase II of its

$4bn mega project in 2Q2015. The company said that tenders

for roads and utilities have already been floated and bids from

contractors have been received for its Sobha Hartland project.

The site will include 282 four, five and six-bed villas, 18 low-rise,

three mid-rise and nine high-rise apartment blocks, along with a

150,000 square meter community center, three hotels, a spa,

two mixed-use towers, two schools, three mosques and a

clubhouse. (Bloomberg)

Dubai World’s unit seeks $1.2bn loan – According to sources,

Port & Free Zone World FZE, a Dubai government-owned ports

group, is raising a $1.2bn loan that will be partly used to help its

parent Dubai World repay its creditors. Reportedly, the loan will

be repaid over five years, with syndication due to start in

2Q2015. Dubai World has to pay $2.92bn to creditors in 2015 as

part of a restructuring deal reached in 2011. More than 70% of

its lenders have agreed to a new plan that includes an extension

of liabilities due in 2018 to 2022. HSBC Holdings, Citigroup and

Emirates NBD are arranging the deal. (Bloomberg)

NBAD expects boost for international Sukuk mandates –

The National Bank of Abu Dhabi’s (NBAD) Global Head of Debt,

Andy Cairns said that the bank expects to handle more

international Sukuk issuance for clients in 2015 amid overall

growth in the sector. NBAD was the bookrunner for 13

international Sukuk in 2014, raising $9.8bn and representing

43% of total supply, and hopes to close around 20 deals in

2015. (GulfBase.com)

ADIA considers investment in Deutsche Bank Triangle site

– The Abu Dhabi Investment Authority (ADIA) may invest more

than $1.1bn in a property development in Frankfurt, Germany.

ADIA, which owns stakes in construction projects in London, UK

and Lucerne, Switzerland, is examining the site known as the

Deutsche Bank Triangle, spanning over 215,000 square feet.

(GulfBase.com)

ADNOC to set up 125 more filling stations by 2015-end –

ADNOC Distribution’s CEO, Abdulla Salem Al Dhaheri said that

the company is planning to build 125 new petrol stations, out of

which 34 are under construction and 15 in the tendering

process. The cost on an average is between AED15-30mn per

station, and will be built across Abu Dhabi and the northern

emirates by the end of 2015 to address a 6% annual

consumption increase. The UAE’s Minister of Energy, Suhail Al

Mazrouei said that ADNOC Distribution is also planning to

expand into Saudi Arabia by 2016 as part of its plans to reduce

losses from subsided petrol sales, which reached AED6.4bn in

2014. (GulfBase.com)

Eagle Hills plans two UAE hotel developments – Abu Dhabi-

based developer Eagle Hills is planning to build two hotel

developments in Dubai and Fujairah. The company will

construct two towers connected by a sky bridge in Dubai’s

6. Page 6 of 7

Jumeirah Beach Residence neighborhood that will include

hundreds of serviced apartments in first tower and a five-star

hotel in the second tower. A resort designed to include more

than 150 hotel rooms and more than 100 villas is planned in

Fujairah. (Bloomberg)

NBO expects 10-12% lending growth in 2015 – The National

Bank of Oman’s (NBO) CEO, Ahmed al-Musalmi said that the

bank is expecting to increase lending by around 10-12% in

2015. Lending growth would be sustained by higher spending on

infrastructure projects thanks to the government's proposal to

boost funding for development, as well as an increasingly

vibrant consumer credit market. In spite of reduced oil revenue

because of the drop in the price of crude, the January 2015

state budget predicted a 4.5% rise in government spending this

year to OMR14.1bn. (Reuters)

GIB appoints MD, CEO for GIB UK – Bahrain-based Gulf

International Bank (GIB) announced the appointment of Mark

Watts, as the Managing Director (MD) and CEO of GIB UK, its

London-based subsidiary providing asset management and

treasury services. The appointment is part of GIB's committed

focus on expanding its asset management business through

GIB UK. (GulfBase.com)

KHCB reports BHD3.05mn net profit in FY2014, not to

distribute dividends – Khaleeji Commercial Bank (KHCB)

reported a net profit of BHD3.05mn in FY2014 as compared to

net loss of BHD19.21mn reported in FY2013. Total net income

grew to BHD14.58mn in FY2014 against BHD7.01mn in

FY2013. EPS amounted to 2.71 fils in FY2014 as against loss

per share of 17.11 fils in FY2013. The bank’s total assets stood

at AED591.92mn at the end of December 2014 as against

AED542.24mn at the end of December 2013. Customer’ current

accounts stood at BHD47.83mn at the end of December 31,

2014. Meanwhile, KHCB‘s board of directors has decided not to

distribute dividends to its shareholders for the financial year

ended December 31, 2014. (Bahrain Bourse)

7. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only.

It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this

report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make

any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

QSE Index S&P Pan Arab S&P GCC

0.1%

0.8%

(0.1%)

0.2%

(0.5%)

(0.9%)

1.0%

(1.2%)

(0.6%)

0.0%

0.6%

1.2%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,233.92 (2.4) (3.9) 4.1 MSCI World Index 1,720.55 (0.4) 2.6 0.6

Silver/Ounce 16.71 (3.2) (3.1) 6.4 DJ Industrial 17,824.29 (0.3) 3.8 0.0

Crude Oil (Brent)/Barrel (FM

Future)

57.80 2.2 9.1 0.8 S&P 500 2,055.47 (0.3) 3.0 (0.2)

Crude Oil (WTI)/Barrel (FM

Future)

51.69 2.4 7.2 (3.0) NASDAQ 100 4,744.40 (0.4) 2.4 0.2

Natural Gas (Henry

Hub)/MMBtu

2.55 (3.0) (4.7) (14.7) STOXX 600 373.31 (0.9) 2.0 2.0

LPG Propane (Arab Gulf)/Ton 54.75 4.0 10.1 11.7 DAX 10,846.39 (1.7) 1.7 3.0

LPG Butane (Arab Gulf)/Ton 69.25 3.6 0.7 5.7 FTSE 100 6,853.44 (0.6) 3.0 2.1

Euro 1.13 (1.4) 0.2 (6.5) CAC 40 4,691.03 (1.4) 2.2 2.7

Yen 119.12 1.4 1.4 (0.6) Nikkei 17,648.50 (0.8) (1.6) 1.4

GBP 1.52 (0.6) 1.2 (2.1) MSCI EM 978.57 (0.4) 1.8 2.3

CHF 1.08 (0.6) (0.7) 7.3 SHANGHAI SE Composite 3,075.91 (1.8) (4.1) (5.5)

AUD 0.78 (0.0) 0.4 (4.6) HANG SENG 24,679.39 (0.4) 0.7 4.6

USD Index 94.70 1.2 (0.1) 4.9 BSE SENSEX 28,717.91 (1.0) (1.5) 6.5

RUB 66.86 0.4 (3.8) 10.1 Bovespa 48,792.27 (2.2) 0.7 (6.9)

BRL 0.36 (1.3) (3.5) (4.6) RTS 826.40 2.7 12.1 4.5

179.9

139.8

128.1