VVIP Pune Call Girls Katraj (7001035870) Pune Escorts Nearby with Complete Sa...

21 November Daily Market Report

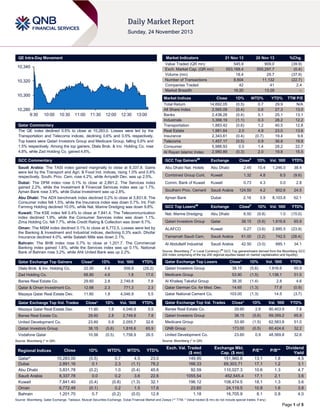

1. QE Intra-Day Movement

Market Indicators

10,340

10,320

10,300

10,280

9:30

21 Nov 13

20 Nov 13

%Chg.

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

545.9

553,188.4

18.4

8,604

42

16:20

909.0

555,297.7

29.7

11,132

41

13:28

(39.9)

(0.4)

(37.9)

(22.7)

2.4

–

Market Indices

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index declined 0.5% to close at 10,283.0. Losses were led by the

Transportation and Telecoms indices, declining 0.6% and 0.5% respectively.

Top losers were Qatari Investors Group and Medicare Group, falling 5.6% and

1.5% respectively. Among the top gainers, Dlala Brok. & Inv. Holding Co. rose

4.8%, while Zad Holding Co. gained 4.6%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

14,692.05

2,565.09

2,438.28

3,368.19

1,883.42

1,981.64

2,343.61

1,457.17

5,988.93

2,980.89

(0.5)

(0.4)

(0.4)

(1.1)

(0.6)

2.0

(0.4)

(0.5)

0.5

(0.3)

0.7

0.6

0.1

0.3

1.2

4.9

(0.7)

0.9

1.4

2.0

29.9

27.3

25.1

28.2

40.5

23.0

19.4

36.8

28.2

19.8

N/A

13.0

13.1

12.2

12.8

13.6

9.6

19.8

22.7

15.5

GCC Commentary

GCC Top Gainers##

Exchange

Close#

1D%

Vol. ‘000

Saudi Arabia: The TASI index gained marginally to close at 8,337.8. Gains

were led by the Transport and Agri. & Food Ind. indices, rising 1.0% and 0.8%

respectively. South. Prov. Cem. rose 4.2%, while Arriyadh Dev. was up 2.5%.

Abu Dhabi Nat. Hotels

Abu Dhabi

2.45

10.4

1,246.0

38.4

Combined Group Cont.

Kuwait

1.32

4.8

6.5

(9.6)

Dubai: The DFM index rose 0.1% to close at 2,891.2. The Services index

gained 2.2%, while the Investment & Financial Services index was up 1.7%.

Ajman Bank rose 3.9%, while Dubai Investment was up 2.8%.

Comm. Bank of Kuwait

Kuwait

Southern Prov. Cement

Saudi Arabia

Abu Dhabi: The ADX benchmark index declined 0.2% to close at 3,831.8. The

Consumer index fell 1.5%, while the Insurance index was down 0.7%. Int. Fish

Farming Holding declined 10.0%, while Nat. Marine Dredging was down 9.8%.

Ajman Bank

Dubai

GCC Top Losers

Exchange

Kuwait: The KSE index fell 0.4% to close at 7,841.4. The Telecommunication

index declined 1.9%, while the Consumer Services index was down 1.1%.

Zima Holding Co. fell 7.7%, while Credit Rating & Collection was down 6.7%.

Nat. Marine Dredging

Abu Dhabi

Qatari Investors Group

Qatar

Oman: The MSM index declined 0.1% to close at 6,772.5. Losses were led by

the Banking & Investment and Industrial indices, declining 0.3% each. Dhofar

Insurance declined 4.0%, while Salalah Mills was down 2.1%.

ALAFCO

Kuwait

Yamamah Saudi Cem.

Saudi Arabia

Al Abdullatif Industrial

Saudi Arabia

42.50

Bahrain: The BHB index rose 0.7% to close at 1,201.7. The Commercial

Banking index gained 1.6%, while the Services index was up 0.1%. National

Bank of Bahrain rose 3.2%, while Ahli United Bank was up 2.2%.

Qatar Exchange Top Gainers

Dlala Brok. & Inv. Holding Co.

##

YTD%

0.73

4.3

0.0

2.8

124.50

4.2

602.6

24.5

2.16

3.9

8,103.8

52.1

#

1D% Vol. ‘000

YTD%

8.50

(9.8)

1.0

(15.0)

38.15

(5.6)

1,816.6

65.9

0.27

(3.6)

2,885.5

(23.9)

61.00

(3.2)

742.5

(28.4)

(3.0)

685.1

34.1

Close

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Close*

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Losers

Close*

1D%

Vol. ‘000

YTD%

22.00

4.8

558.8

(29.2)

Qatari Investors Group

38.15

(5.6)

1,816.6

65.9

Medicare Group

53.90

(1.5)

1,138.1

51.0

Zad Holding Co.

68.80

4.6

1.8

17.0

Barwa Real Estate Co.

29.60

2.8

2,749.8

7.8

Al Khaleej Takaful Group

38.35

(1.4)

2.8

4.6

Qatar & Oman Investment Co.

12.68

2.3

771.3

2.3

Qatar German Co. for Med. Dev.

14.65

(1.3)

77.8

(0.9)

Mazaya Qatar Real Estate Dev.

11.60

1.8

4,046.9

5.5

Qatar National Cement Co.

103.00

(1.3)

14.5

(3.7)

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Val. ‘000

Mazaya Qatar Real Estate Dev.

11.60

1.8

4,046.9

5.5

Barwa Real Estate Co.

29.60

2.8

80,403.9

7.8

Barwa Real Estate Co.

29.60

2.8

2,749.8

7.8

Qatari Investors Group

38.15

(5.6)

69,359.2

65.9

United Development Co.

23.60

0.9

2,055.7

32.6

Medicare Group

Qatari Investors Group

38.15

(5.6)

1,816.6

65.9

QNB Group

Vodafone Qatar

10.56

(0.5)

1,758.9

26.5

United Development Co.

Qatar Exchange Top Vol. Trades

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

YTD%

53.90

(1.5)

62,583.8

51.0

173.00

(0.5)

60,424.6

32.2

23.60

0.9

48,569.8

32.6

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar Exchange Top Val. Trades

Close

1D%

WTD%

MTD%

YTD%

10,283.00

2,891.16

3,831.78

8,337.78

7,841.40

6,772.48

1,201.70

(0.5)

0.1

(0.2)

0.0

(0.4)

(0.1)

0.7

0.7

2.3

1.0

0.2

(0.8)

0.2

(0.2)

4.5

(1.1)

(0.4)

3.6

(1.3)

1.5

(0.0)

23.0

78.2

45.6

22.6

32.1

17.6

12.8

Exch. Val. Traded

($ mn)

149.95

166.33

92.59

1055.54

196.12

23.60

1.18

Exchange Mkt.

Cap. ($ mn)

151,960.8

69,303.71

110,027.3

452,545.4

108,474.5

24,119.5

16,705.9

P/E**

P/B**

13.1

17.1

10.6

17.1

18.1

10.8

8.1

1.8

1.2

1.3

2.1

1.3

1.6

0.8

Dividend

Yield

4.5

3.1

4.7

3.6

3.6

3.8

4.0

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 5

2. Qatar Market Commentary

The QE index declined 0.5% to close at 10,283.0. The

Transportation and Telecoms indices led the losses. The index

declined on the back of selling pressure from Qatari

shareholders despite buying support from non-Qatari

shareholders.

Qatari Investors Group and Medicare Group were the top losers,

falling 5.6% and 1.5% respectively. Among the top gainers, Dlala

Brok. & Inv. Holding Co. rose 4.8%, while Zad Holding Co.

gained 4.6%.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

67.89%

69.08%

(6,531,748.88)

Non-Qatari

32.11%

30.91%

6,531,748.88

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Thursday declined by 37.9% to

18.4mn from 29.7mn on Wednesday. Further, as compared to

the 30-day moving average of 9.3mn, volume for the day was

99.1% higher. Mazaya Qatar Real Estate Dev. and Barwa Real

Estate Co. were the most active stocks, contributing 22.0% and

14.9% to the total volume respectively.

Global Economic Data

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

Previous

11/21

US

Department of Labor

Initial Jobless Claims

16-November

323K

335K

344K

11/21

US

Department of Labor

Continuing Claims

9-November

2876K

2870K

2810K

11/21

US

Bureau of Labor Stat.

PPI MoM

October

-0.20%

-0.20%

-0.10%

11/21

US

Bureau of Labor Stat.

PPI YoY

October

0.30%

0.30%

0.30%

11/21

US

Bloomberg Indices

Markit US PMI Preliminary

November

54.3

52.3

51.8

11/21

US

Bloomberg

Bloomberg Economic Expectations

November

-14

–

-31

11/21

US

Bloomberg

Bloomberg Consumer Comfort

17-November

-34.6

–

-33.9

11/22

US

Bureau of Labor Stat.

JOLTs Job Openings

September

3913

3850

3844

11/21

EU

Markit

PMI Manufacturing

November

51.5

51.5

51.3

11/21

EU

Markit

PMI Services

November

50.9

51.9

51.6

11/21

EU

Markit

PMI Composite

November

51.5

52.0

51.9

11/21

EU

European Commission

Consumer Confidence

November

-15.4

-14

-14.5

11/21

France

Markit

PMI Manufacturing

November

47.8

49.5

49.1

11/21

France

Markit

PMI Services

November

48.8

51.0

50.9

11/21

Germany

Markit

PMI Manufacturing

November

52.5

52.0

51.7

11/21

Germany

Markit

PMI Services

November

54.5

53.0

52.9

11/22

Germany

Destasis

GDP SA QoQ

3Q2013

0.30%

0.30%

0.70%

11/22

Germany

Destasis

GDP WDA YoY

3Q2013

0.60%

0.60%

0.50%

11/22

Germany

Destasis

GDP NSA YoY

3Q2013

1.10%

1.10%

0.90%

11/22

Germany

Destasis

Exports QoQ

3Q2013

0.10%

0.30%

2.40%

11/22

Germany

Destasis

Imports QoQ

3Q2013

0.80%

0.60%

1.90%

11/22

Germany

IFO

IFO Business Climate

November

109.3

107.7

107.4

11/22

Germany

IFO

IFO Current Assessment

November

112.2

111.5

111.3

11/22

Germany

IFO

IFO Expectations

November

106.3

104.0

103.7

11/21

UK

ONS

Public Finances (PSNCR)

October

-16.8B

–

-0.5B

11/21

UK

CBI

CBI Trends Total Orders

November

11

1

-4

11/21

UK

CBI

CBI Trends Selling Prices

November

5

-3

-2

11/22

Italy

ISTAT

Retail Sales MoM

September

-0.30%

0.10%

0.00%

11/22

Italy

ISTAT

Retail Sales YoY

September

-2.80%

–

0.20%

11/21

China

HSBC Bank

HSBC/Markit Flash Mfg PMI

November

50.4

50.8

50.9

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

Real estate prices fall seen slowing – The fall in land prices in

Qatar since May this year is expected to slow down the rate of

increase in rents, a QNB Group analysis has said. According to

the QNB Group, the fundamental driver of real estate prices is

the cost of land. If land prices rise, the price of villas, apartments

and other property is also likely to go up. The QNB Group, while

analyzing the Real Estate Price Index of the Qatar Central Bank

(QCB), said that the rise in the land prices up to May 2013 was

mainly due to the acquisition of land for major projects that are

being implemented in Qatar, particularly land for the Doha

metro, large shopping malls and mixed use real estate

development, like Msheireb and Lusail. Since these projects

have reached the construction phase, much of the land is

Page 2 of 5

3. already secured. This could lead to an easing of real estate

prices. The Group has analyzed data on land transactions in

Qatar, based on weekly statistics published by the Ministry of

Justice, which indicates that the cost of land has fallen in the last

five months from May to September. This is likely to ease

upward pressures on rents, enhancing the competitiveness of

the Qatari economy and relieving concerns that the real estate

sector is again experiencing an asset-price bubble like the one

in 2007-08. (Peninsula Qatar)

Azevedo said WTO may agree on its first worldwide trade

reform package within the next few days. The deal would

streamline customs procedures worldwide, making bordercrossing processes more predictable and transparent. Azevedo

forced the marathon negotiations to try to get the deal before a

meeting of WTO ministers in Bali in the first week of December.

Meanwhile, studies by the World Bank and the OECD have

found this deal would add hundreds of billions of dollars to the

world economy. (Reuters)

Qatar to export 23mn tons of petrochemicals per year by

2020 – Muntajat’s CEO Abdulrahman Ali Al-Abdulla said

planned investments in Qatar’s chemical and petrochemical

industry will enhance the country’s export portfolio to 23mn tons

per year by 2020 from 10mn tons in 2013. Al-Abdulla said the

Gulf petrochemicals industry continues to be the largest

producer and exporter in the world, accounting for 11% of the

$600bn global market. (Gulf-Times.com)

ECB warns of deflationary pressures in Eurozone – The

European Central Bank's Chief Economist Peter Praet said the

Eurozone faces deflationary pressures, while the bank's

President Mario Draghi stressed that interest rates must remain

low because the economy remains weak. Peter Praet said the

financial crisis had saddled the Eurozone with an unprecedented

debt burden in Europe's post-war history, because it has created

a more deflationary environment. Meanwhile, with Eurozone

inflation running at 0.7%, which is well below its target of around

2% this week, a raft of ECB speakers said that fresh measures

may have to be taken to support the economy. (Reuters)

Kahramaa: Power demand to rise 10% in 5 years – The

Qatar General Electricity & Water Corporation (Kahramaa) said

the electricity demand in Qatar is set to rise 10% YoY over the

next five years. The rising demand in Qatar has fuelled the

recent decision to pre-qualify bidders for the tender to build

Kahramaa’s next independent water & power project, which is

expected to deliver its first electricity output by 2016.

(GulfBase.com)

Plans for new medical commission units, 836 more hospital

beds – According to sources, Qatari Supreme Council of Health

(SCH) and Hamad Medical Corporation (HMC) are

implementing plans that include the establishment of two new

units of the Medical Commission and addition of 836 beds to

hospitals by 2015, among other key projects. The key future

projects include the establishment of three hospitals attached to

SCH, six hospitals attached to HMC and 18 health centers

attached to the Primary Health Care Corporation. There will also

be expansion in other health services and facilities, including

pharmacies, ambulance, X-ray, laboratories and outpatient

clinics. (Gulf-Times.com)

Qatar Steel’s sustainability report gets A rating from GRI –

Qatar Steel’s 2012 sustainability report has achieved an “A”

rating from Global Reporting Initiative (GRI) following an

external audit for assurance of the accuracy of its content.

(Peninsula Qatar)

Indian Ambassador: Great potential for solar energy tie-ups

with Qatar – Indian Ambassador to Qatar Sanjiv Arora said

there is enormous potential for tie-ups in developing solar

energy among the two countries as both are looking forward to

more areas of efficient application of renewable energies in the

coming years. (Gulf-Times.com)

International

Iran agrees to curb its nuclear program – Iran and world

powers struck an accord, setting limits on the Islamic Republic’s

nuclear program in exchange for limited relief from sanctions.

The accord was reached after foreign ministers from the US,

Europe, China and Russia made unscheduled trips to Geneva to

push the third round of talks to a conclusion. The accord is

intended to be a first step toward a comprehensive agreement,

and is reversible if reciprocal measures are not taken. Iran will

get about $7bn in relief from economic sanctions over six

months under the first-step agreement. In return for Iran limiting

its nuclear program, the first-step agreement will release $4.2bn

in frozen assets from Iran’s diminished oil revenue. (Bloomberg)

WTO chief hopeful of global trade reform deal within days –

The World Trade Organization’s General Director Roberto

EU trade Chief: China investment pact must address

opening markets – EU Trade Commissioner Karel De Gucht

said Europe has no interest in a bilateral investment pact with

China that omits measures to open up markets in the Asian

giant. These comments were made after a summit with Chinese

leaders announced plans for treaty talks. EU officials said talks

on the pact – a widely expected outcome of the summit – will be

a test of China's willingness to compromise and play by the

rules set by the World Trade Organization. De Gucht said he

expected talks would begin within weeks, but he would not

estimate how long a deal would take. (Reuters)

OECD: Luxembourg, Cyprus, Switzerland fail tax

transparency test – According to the Global Forum on

Transparency & Exchange of Information for Tax Purposes (an

Organization for Economic Cooperation & Development (OECD)

forum), Luxembourg, Cyprus, the British Virgin Islands,

Switzerland and the Seychelles did not meet international

standards on tax transparency. The five countries either failed to

share taxpayer information with other countries or gather

information on beneficial ownership of corporate entities

registered on their territory, or both, which potentially puts

investments in the countries at risk. The OECD, which oversees

the forum, has been asked by the group of 20 leading

economies, to lead efforts on curbing international tax evasion

and avoidance. (Reuters)

Regional

Oil market to remains well supplied – Saudi Arabia’s

Assistant Minister for Petroleum Affairs Abdulaziz bin Salman

bin Abdulaziz said that the oil market remains well supplied for

maintaining the balance in the global economy. Abdulaziz said

concerns over tight oil supply have now been replaced by

perceptions of abundant oil resources. (GulfBase.com)

SDF signs deals with SAIB, Saudi Export Co – The Saudi

Development Fund (SDF) has signed a MoU worth SR145mn

with the Saudi Investment Bank (SAIB), under which SDF will

offer guarantees to exports of Saudi non-oil products.

Meanwhile, SDF has also entered into a SR11.25mn deal with

Saudi Export Company to finance the export of electrical

products and other Saudi commodities to Ghana through

Lumiere Energy Services Company. (GulfBase.com)

SEC awards SR2.1bn turbine contracts – The Saudi

Electricity Company (SEC) has awarded contracts worth

SR2.1bn to supply gas and steam turbines for its two new power

Page 3 of 5

4. plants in Riyadh. Under these contracts, 12 gas units and 4

steam turbines will be built and tested within 40 months.

(GulfBase.com)

Alstom SA secures €170mn generator contract from HHI for

Shuqaiq project – Alstom Saudi Arabia Transport & Power

Limited (Alstom SA) has secured a contract worth €170mn from

South Korea-based Hyundai Heavy Industries (HHI) to supply

four 720MW steam turbine generators for the Shuqaiq power

plant project. Under this contract, Alstom SA will provide

engineering, manufacturing, supply and field services for the

steam turbines and generators, which will also include all direct

control and auxiliary systems. The Shuqaiq plant is due to enter

into commercial operation in 2017. (GulfBase.com)

FIPCO signs SR11.4mn loan deal with SIDF – Filling &

Packing Materials Manufacturing Company (FIPCO) has

entered into a long-term loan agreement worth SR11.4mn with

the Saudi Industrial Development Fund (SIDF) to finance its

project of form fill seal (FFS) bags. (Tadawul)

DAAR closes second tranche of Sukuk program – The Dar

Al Arkan Real Estate Development Company (DAAR) has

successfully closed the second Sukuk tranche under its

International Islamic Sukuk Program by raising SR1.1bn. The

order book was oversubscribed by twice the amount and the

Sukuk was issued at a profit rate of 5.75% per annum, which

matures on November 25, 2016. DAAR appointed Bank Al

Khair, Goldman Sachs, Deutsche Bank, Emirates NBD, Bank of

America Merrill and Al Hilal bank to manage this second

tranche. (Tadawul)

KEC’s unit begins delivery of villas to customers – The

Knowledge Economic City Company (KEC) announced that its

subsidiary, the Knowledge Real Estate Company Ltd has begun

the delivery of 206 villas in the Phase 1 of Dar Al Jiwar project to

residential customers. This is considered to be the first gated

community center in Al Madinah Al Munawwarah. The delivery

of these villas is expected to continue from 4Q2013 through the

next financial year ending December 31, 2014. (Tadawul)

Alwaleed weighs options for Four Seasons, Fairmont Hotels

– Saudi billionaire Prince Alwaleed bin Talal is weighing stake

sale options including an IPO for his US-based hotels, Four

Seasons Holdings and Fairmont Hotels & Resorts. Alwaleed,

who took a 95% stake in the Four Seasons chain, said he is

considering strategic options for the two companies including an

IPO or a merger. (GulfBase.com)

ADC signs deal with SFC for portfolio management – AlAhsa Development Company (ADC) has signed an agreement

with Saudi Fransi Capital (SFC) for discretionary portfolio

management and transfer of all its portfolios to the SFC for the

purpose of Saudi equities listed trading. The portfolio’s

conservative assessment stood at SR105mn on October 31,

2013, and then re-evaluated after conversion to the new

portfolio at SR110mn on November 10, 2013. (Tadawul)

SCC delays re-operation of Kilns 4 & 5 in Hofuf factory –

The Saudi Cement Company (SCC) stated that the re-operation

of Kilns 4 & 5 in its Hofuf factory has been delayed due to

technical reasons, which is now expected to take place in

3Q2014. (Tadawul)

could not confirm projections on its financial performance.

Earlier, the Saudi CMA had given approval for selling 11mn

shares, which represents 40% of the company’s shares.

(GulfBase.com)

EIB changes name to Emirates Islamic – The Emirates

Islamic Bank (EIB) has changed its name to “Emirates Islamic”

as a part of a comprehensive rebranding exercise undertaken by

the bank.

Abu Dhabi scraps 5% cap on annual rent increase – The

Abu Dhabi Executive Council said the Emirate has decided to

scrap a 5% cap on annual rent increase. In January 2008, Abu

Dhabi had imposed this cap on annual rent hikes after surging

demand had boosted rents and inflation. (GulfBase.com)

Emaar Chairman: Good time to weigh retail spinoff – Emaar

Properties said the current environment makes it good time to

for the company to consider spinning of its retail business into a

separate company to increase investor returns. (GulfTimes.com)

ADCCI, Masdar sign MoU to promote Abu Dhabi and

Masdar City – The Abu Dhabi Chamber of Commerce &

Industry (ADCCI) has entered into a MoU with the Abu Dhabi

Future Energy Company (Masdar) to promote Abu Dhabi and

Masdar City as key investment destinations in the UAE. Under

this MoU, ADCCI and Masdar will showcase the Emirate's

unique commercial offerings and attract international investors.

(GulfBase.com)

Mubadala Aerospace eyes US acquisitions to expand

manufacturing capabilities – Mubadala Aerospace’s Executive

Director Homaid Al Shemmari said that the company is targeting

acquisitions in the US to expand its manufacturing capabilities,

after securing billion dollar contracts at the Dubai Airshow. This

expansion will include acquisitions of companies in aero

structures, engineering, and research & development areas.

Shemmari also said that the company aims to become the

world’s top three manufacturers of composite and metal parts for

airplanes by 2020. (GulfBase.com)

Kuwait Airways resumes flights to Iraq – Kuwait Airways has

resumed flights to Iraq and has planned to begin two weekly

flights to Najaf in Iraq. For the first time since the 1990 Iraqi

invasion, a Kuwait Airways flight landed in Iraq on Wednesday,

indicating improved ties between the neighbors. (GulfBase.com)

Oman’s Advisory Committee proposes tax on remittances –

Oman’s Advisory Committee has proposed that the Sultanate

should tax the billions of dollars that foreign workers send back

to their home countries every year. According to Central Bank of

Oman’s data, outward worker remittances stood at OMR3.1bn in

2012, indicating an increase of 12.1%. (GulfBase.com)

Takamul signs 25-year deal with SEZAD to provide

industrial utilities – The Takamul Investment Company,

through its newly incorporated Centralised Utilities Company

(CUC) has signed a 25-year agreement with the Special

Economic Zone Authority at Duqm (SEZAD) to provide industrial

utilities within the Duqm SEZ. This agreement provides CUC

exclusive rights to provide all utilities to the industrial zone within

the Duqm SEZ. (GulfBase.com)

Saudi CMA approves SEC’s sukuk – The Saudi CMA’s board

has approved Saudi Electricity Company's (SEC) sukuk. The

total offering size will be determined at a later stage by the

Company. (Tadawul)

AFCO cancels IPO plan – The Astra Food Company (AFCO)

has canceled its plan to go for an IPO of its shares, since it

Page 4 of 5

5. Daily Index Performance

1.0%

147.8

0.5%

132.3

118.9

0.7%

0.1%

0.0%

0.0%

(0.1%)

QE Index

S&P Pan Arab

Jul-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Oman

May-12 Dec-12

Bahrain

Oct-11

Qatar

(1.0%)

Jan-10 Aug-10 Mar-11

Saudi Arabia

(0.5%)

(0.2%)

(0.4%)

Kuwait

(0.5%)

Dubai

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

Abu Dhabi

Rebased Performance

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,243.83

0.1

(3.6)

(25.8)

DJ Industrial

16,064.80

0.3

0.6

22.6

19.87

(0.5)

(4.5)

(34.5)

S&P 500

1,807.65

0.4

0.5

26.7

111.05

0.0

2.4

(0.1)

NASDAQ 100

3,991.65

0.6

0.1

32.2

3.77

2.5

6.0

10.1

STOXX 600

322.77

0.1

(0.1)

15.4

119.75

(0.4)

0.9

33.8

DAX

9,219.04

0.2

0.5

21.1

143.00

(1.2)

(0.3)

(17.3)

FTSE 100

6,674.30

(0.1)

(0.3)

13.2

4,278.53

0.6

(0.3)

17.5

15,381.72

0.1

1.4

48.0

1.36

0.6

0.5

2.8

101.27

0.1

1.1

16.7

Nikkei

GBP

1.62

0.2

0.7

(0.2)

MSCI EM

1,009.17

0.5

0.4

(4.4)

CHF

1.10

0.7

0.9

1.0

SHANGHAI SE Composite

2,196.38

(0.4)

2.8

(3.2)

AUD

0.92

(0.4)

(1.8)

(11.5)

HANG SENG

23,696.30

0.5

2.9

4.6

USD Index

80.71

(0.5)

(0.2)

1.2

BSE SENSEX

20,217.40

(0.1)

(0.9)

4.1

RUB

32.77

(0.8)

0.6

7.4

Bovespa

52,800.70

0.2

(1.2)

(13.4)

BRL

0.44

1.1

1.7

(10.0)

1,444.91

1.3

0.0

(5.4)

Yen

Source: Bloomberg

CAC 40

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5