VIP Call Girl in Mumbai 💧 9920725232 ( Call Me ) Get A New Crush Everyday Wit...

13 April Daily market report

1. Page 1 of 5

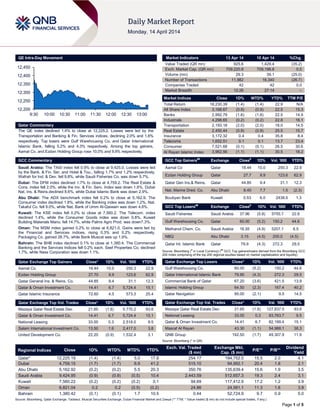

QE Intra-Day Movement

Qatar Commentary

The QE index declined 1.4% to close at 12,225.2. Losses were led by the

Transportation and Banking & Fin. Services indices, declining 2.0% and 1.6%

respectively. Top losers were Gulf Warehousing Co. and Qatar International

Islamic Bank, falling 5.2% and 4.3% respectively. Among the top gainers,

Aamal Co. and Ezdan Holding Group rose 10.0% and 9.9% respectively.

GCC Commentary

Saudi Arabia: The TASI index fell 0.9% to close at 9,425.0. Losses were led

by the Bank. & Fin. Ser. and Hotel & Tou., falling 1.7% and 1.2% respectively.

Wafrah for Ind. & Dev. fell 9.8%, while Saudi Fisheries Co. was down 5.7%.

Dubai: The DFM index declined 1.7% to close at 4,759.2. The Real Estate &

Cons. index fell 2.0%, while the Inv. & Fin. Serv. Index was down 1.6%. Dubai

Nat. Ins. & Reins.declined 8.6%, while Dubai Islamic Bank was down 2.9%.

Abu Dhabi: The ADX benchmark index fell 0.2% to close at 5,162.9. The

Consumer index declined 1.8%, while the Banking index was down 1.2%. Nat.

Takaful Co. fell 9.0%, while Nat. Bank of Umm Al-Qaiwain was down 4.6%.

Kuwait: The KSE index fell 0.2% to close at 7,560.2. The Telecom. index

declined 1.4%, while the Consumer Goods index was down 0.8%. Kuwait

Building Materials Manu. fell 14.7%, while Palms Agro Prod. was down7.3%.

Oman: The MSM index gained 0.2% to close at 6,821.0. Gains were led by

the Financial and Services indices, rising 0.3% and 0.2% respectively.

Packaging Co. gained 28.7%, while Bank Muscat was up 1.9%.

Bahrain: The BHB index declined 0.1% to close at 1,380.4. The Commercial

Banking and the Services Indices fell 0.2% each. Seef Properties Co. declined

1.7%, while Nass Corporation was down 1.1%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Aamal Co. 18.44 10.0 250.3 22.9

Ezdan Holding Group 27.70 9.9 123.6 62.9

Qatar General Ins. & Reins. Co. 44.85 9.4 31.1 12.3

Qatar & Oman Investment Co. 14.41 6.7 5,724.4 15.1

Qatar Islamic Insurance 72.60 4.5 573.3 25.4

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Mazaya Qatar Real Estate Dev. 21.65 (1.6) 5,770.2 93.6

Qatar & Oman Investment Co. 14.41 6.7 5,724.4 15.1

National Leasing 33.00 0.3 2,518.0 9.5

Salam International Investment Co. 13.50 1.6 2,417.0 3.8

United Development Co. 22.20 (0.9) 1,532.4 3.1

Market Indicators 13 Apr 14 10 Apr 14 %Chg.

Value Traded (QR mn) 925.6 1,429.4 (35.2)

Exch. Market Cap. (QR mn) 709,220.8 709,196.8 0.0

Volume (mn) 29.3 39.1 (25.0)

Number of Transactions 11,982 16,340 (26.7)

Companies Traded 42 42 0.0

Market Breadth 12:26 27:14 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,230.39 (1.4) (1.4) 22.9 N/A

All Share Index 3,168.67 (0.9) (0.9) 22.5 15.3

Banks 2,992.79 (1.6) (1.6) 22.5 14.9

Industrials 4,298.65 (0.2) (0.2) 22.8 16.1

Transportation 2,193.18 (2.0) (2.0) 18.0 14.5

Real Estate 2,450.44 (0.9) (0.9) 25.5 15.7

Insurance 3,172.32 0.4 0.4 35.8 8.4

Telecoms 1,652.51 0.1 0.1 13.7 23.4

Consumer 7,521.68 (0.1) (0.1) 26.5 30.6

Al Rayan Islamic Index 3,962.56 (1.1) (1.1) 30.5 18.2

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Aamal Co Qatar 18.44 10.0 250.3 22.9

Ezdan Holding Group Qatar 27.7 9.9 123.6 62.9

Qatar Gen Ins.& Reins. Qatar 44.85 9.4 31.1 12.3

Nat. Marine Dred. Co. Abu Dhabi 8.40 7.7 1.5 (2.3)

Boubyan Bank Kuwait 0.53 6.0 2438.5 1.3

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Saudi Fisheries Saudi Arabia 37.96 (5.8) 5755.7 22.8

Gulf Warehousing Co. Qatar 60.00 (5.2) 150.2 44.6

Methanol Chem. Co. Saudi Arabia 16.55 (4.9) 5207.1 8.5

NBQ Abu Dhabi 3.15 (4.5) 200.0 (4.5)

Qatar Int. Islamic Bank Qatar 79.9 (4.3) 272.3 29.5

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Gulf Warehousing Co. 60.00 (5.2) 150.2 44.6

Qatar International Islamic Bank 79.90 (4.3) 272.3 29.5

Commercial Bank of Qatar 67.20 (3.6) 421.5 13.9

Islamic Holding Group 64.50 (2.3) 167.4 40.2

Qatar Navigation 95.00 (2.1) 9.5 14.5

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Mazaya Qatar Real Estate Dev. 21.65 (1.6) 127,837.5 93.6

National Leasing 33.00 0.3 83,763.7 9.5

Qatar & Oman Investment Co. 14.41 6.7 82,199.4 15.1

Masraf Al Rayan 43.30 (1.1) 54,988.1 38.3

QNB Group 192.50 (1.7) 49,307.9 11.9

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,225.19 (1.4) (1.4) 5.0 17.8 254.17 194,752.0 15.5 2.0 4.1

Dubai 4,759.15 (1.7) (1.7) 6.9 41.2 515.10 94,992.1 20.4 1.8 2.1

Abu Dhabi 5,162.92 (0.2) (0.2) 5.5 20.3 350.76 135,639.4 15.6 1.9 3.5

Saudi Arabia 9,424.95 (0.9) (0.9) (0.5) 10.4 2,443.59 512,657.3 19.3 2.4 3.1

Kuwait 7,560.22 (0.2) (0.2) (0.2) 0.1 94.69 117,412.9 17.2 1.2 3.9

Oman 6,821.04 0.2 0.2 (0.5) (0.2) 24.86 24,581.1 11.3 1.6 3.9

Bahrain 1,380.42 (0.1) (0.1) 1.7 10.5 0.44 52,724.9 9.7 0.9 5.0

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any;)

12,200

12,250

12,300

12,350

12,400

12,450

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 5

Qatar Market Commentary

The QE index declined 1.4% to close at 12,225.2. The

Transportation and Banking & Fin. Services indices led the

losses. The index fell on the back of selling pressure from Qatari

shareholders despite buying support from non-Qatari

shareholders.

Gulf Warehousing Co. and Qatar International Islamic Bank were

the top losers, falling 5.2% and 4.3% respectively. Among the

top gainers, Aamal Co. and Ezdan Holding Group rose 10.0%

and 9.9% respectively.

Volume of shares traded on Sunday fell by 25.0% to 29.3mn

from 39.1mn on Thursday. However, as compared to the 30-day

moving average of 19.8mn, volume for the day was 48.0%

higher. Mazaya Qatar Real Estate Dev. and Qatar & Oman

Investment Co. were the most active stocks, contributing 19.7%

and 19.5% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings

Earnings Releases

Company Market Currency

Revenue

(mn)1Q2014

% Change

YoY

Operating Profit

(mn) 1Q2014

% Change

YoY

Net Profit (mn)

1Q2014

% Change

YoY

Saudi Industrial Export Co.

(SIEC)

Saudi SR – – 2.2 -24.1% 1.7 -37.0%

Saudi Arabian Fertilizer Co.

(SAFCO)

Saudi SR – – 797.0 -4.0% 843.0 -9.5%

Saudi Chemical Co. (SCC) Saudi SR – – 102.9 29.1% 91.0 3.0%

Taiba Holding Co. Saudi SR – – 58.9 7.3% 59.5 -18.6%

Saudi Ceramic Co. (SCC) Saudi SR – – 88.5 -2.8% 87.4 6.3%

Shuaa Capital Dubai AED 64.0 77.8% – – 8.2 NA

Al Anwar Ceramic Tiles Co.

(AACT)

Oman OMR 7.2 0.1% – – 2.2 0.8%

National Hotels Co.

(NHOTEL)

Bahrain BHD 1.9 -15.3% 0.9 -23.3% 0.7 -27.5%

Source: Company data, DFM, ADX, MSM

News

Qatar

QE amends foreign ownership limit for CBQK – The Qatar

Exchange has announced that the ownership limit of non-Qatari

investors for the Commercial Bank of Qatar (CBQK) would be

25% with effect from April 13, 2014. (QE)

ETFs to debut on QE, to boost liquidity – According to

sources, exchange traded funds (ETFs) are set to make their

debut next week (April 23) on the Qatar Exchange (QE) as the

bourse enters the MSCI „emerging‟ market grouping by June. As

part of QE‟s measures to enhance liquidity in the market, foreign

debt-based and general index-based ETFs are set to be

launched initially, which will be followed by Islamic-index based

ETFs by the end of summer. (Gulf-Times.com)

MERS to publish 1Q2014 financials on April 22 – Al Meera

Consumer Goods Company (MERS) will publish its 1Q2014

financial results on April 22, 2014. (QE)

MCGS to disclose 1Q2014 results on April 23 – Medicare

Group (MCGS) will disclose its 1Q2014 financial results on April

23, 2014. (QE)

UDCD to disclose 1Q2014 results on April 27 – The United

Development Company (UDCD) to disclose its 1Q2014 financial

results on April 27, 2014. (QE)

QNCD convenes BoD meet on April 13 – Qatar National

Cement Company‟s (QNCD) board of directors held a meeting

on April 13, 2014 to decide about contracting for the

construction of cement plant no 5. We await more details, as of

now we have incorporated 5,000 tpd of expansion in our model

leading to a 12-month target price of QR137.28. (QE, QNBFS)

QA to launch 7th Saudi route from May 15 – Qatar Airways

(QA) has announced that it will add Al Hofuf in Saudi Arabia to

its network with four weekly flights from May 15, 2014. QA has

further doubled its weekly flight frequency to Gassim, while

flights to Madinah have been increased from five to seven per

week. With this, QA will now fly to seven Saudi destinations with

79 flights per week. (Bloomberg)

Bayt survey shows positive economic outlook in Qatar –

According to a survey by Bayt.com, close to half of Qatar‟s

population believes that the country‟s economy has improved in

the last six months. The survey added that while 51% of Qatar

respondents share a positive sentiment about their personal

financial position improving over the next six months, 70%

expect the cost of living to increase. In Qatar, 30% claim their

financial position has improved in the last six months, while 32%

claim that there has been no change and 31% reported a

decline. Almost half of the respondents (45%) claim that their

savings have decreased as compared to 12 months ago.

However, the outlook is positive with 51% anticipating their

financial situation to improve over the next six months, despite

the expected increase in cost of living within the same period.

(Gulf-Times.com)

VFQS appoints senior executives – Vodafone Qatar (VFQS)

has appointed Mahmud Awad as the Chief Business Officer and

Ramy Reyad as the Chief Technology Officer. Awad has 18

years of telecom experience, and joins Vodafone Qatar from du

Telecom where he was the Vice President of Corporate Sales.

Awad has also held executive positions with Neoris, Al Wataniya

Telecom and Nokia Siemens Networks. Meanwhile, Reyad has

over 15 years of experience in the telecom sector and joins

Overall Activity Buy %* Sell %* Net (QR)

Qatari 67.79% 72.92% (47,439,038.18)

Non-Qatari 32.22% 27.09% 47,439,038.18

3. Page 3 of 5

VFQS from Mobilink, where he was the Chief Technology

Officer. (Gulf-Times.com)

International

Euro slides against most peers as Draghi warns of ECB

stimulus – The Eurozone‟s currency has weakened against

most of its 16 major peers after the European Central Bank‟s

President Mario Draghi said its strength requires further

monetary stimulus. The shared currency snapped a gain versus

the US dollar from last week that was the most in six months as

Draghi‟s rhetoric about the euro‟s rise was echoed by other

European policy makers, boosting speculation they will consider

measures to support growth and spur inflation. The dollar gained

against most peers before a report that may show retail sales

gained last month by the most in 1 1/2 years. Draghi reiterated

that the currency does come into ECB‟s views on monetary

policy and it does naturally act as a handbrake on inflation. The

Euro fell 0.3% to $1.385 after climbing 1.3% last week, the

biggest gain since September 20, 2013. (Bloomberg)

Growth pickup may help France meet deficit targets –

France‟s Finance Minister Michel Sapin said the French

economy may grow faster than projected this year, helping the

government to meet European Union budget-deficit targets.

Sapin said in 2014, the economy will do slightly better than the

0.9% growth forecast by the government. President Francois

Hollande‟s new government is seeking to regain economic

credibility after his Socialist Party suffered a crushing defeat in

the recent municipal elections. Sapin‟s remarks indicate that

officials are looking for ways to stimulate growth while meeting

budget pledges that Hollande put in doubt last month. France‟s

deficit amounted to 4.3% of GDP in 2013. To adhere to the EU

economic rules, Hollande had promised to trim the shortfall to

3.6% in 2014 and 3% in 2015. (Bloomberg)

Bloomberg: Price surge could harm public confidence on

Abenomics – Japanese Prime Minister Shinzo Abe‟s efforts to

vault the country out of 15 years of deflation risk losing public

support by spurring too much inflation too quickly as companies

add extra price increases to this month‟s sales-tax hike.

Businesses have raised costs more than the 3% point levy

increase. This month‟s inflation rate could be 3.5%, the fastest

since 1982. The challenge for Abe and the Bank of Japan is to

keep the public focused on the long-term benefits of exiting

deflation when wages are yet to pick up. Any jump in inflation

that is perceived as excessive by a population more used to

prices falling could worsen consumer confidence and make it

harder to boost growth. (Bloomberg)

Regional

MEED: GCC new contract awards to approach $150bn in

2014 – According to a report released by MEED, new contract

awards in the GCC region are set to approach $150bn in 2014,

rising over about $135bn in the previous 12 months. The

projects boom encompasses all the six GCC markets and

extends across all sectors. MEED said that with more than

$40bn worth of new contracts awarded in the six-nation GCC

alone in 1Q2014, the projects market in the Middle East is set to

enjoy a record-breaking in 2014. Among the high-profile projects

that have been awarded include: the $12bn Kuwait National

Petroleum Company‟s Clean Fuels Project; $3bn worth of

projects awarded by Qatar‟s Ashgal for the Expressway and

LRDP schemes; Abu Dhabi Musanada‟s $1bn worth of contracts

for the Mafraq-Ghuweifat Road Development Project; Qatar

Rail‟s $700mn worth of contracts for the elevated section of the

Doha Metro‟s Red Line South project; and $705mn awarded by

the Al Reem Island (UAE). Figures compiled by MEED Projects

show that a total of almost $2.5tn worth of contracts have been

planned or under way in the GCC. (Gulf-Times.com)

Saudia to invest $476.7mn for cargo expansion – The Saudi

Arabian Airlines (Saudia) is planning to pump in $476.7mn over

the next 5-7 years to boost its cargo handling facilities. About

$26.7mn will be injected into Saudia Cargo for investing in its

ground facilities over the next 12 months, while $450mn will be

spent on its hubs at Riyadh, Jeddah and Dammam over 5-7

years. (GulfBase.com)

Chemanol to shutdown Methanol plant from April 14 – The

Methanol Chemicals Company (Chemanol) announced that will

begin the non-scheduled shutdown of its Methanol plant for a

period of 15 days, from April 14, 2014. The non-scheduled

maintenance activity will be carried out for inspecting the valve

trays of the distillation column to improve the production

efficiency of the plant. Such activity will result in the shutdown of

the Dimethylformamide unit, which mainly uses the carbon

monoxide produced by the Methanol plant. (Tadawul)

SCPMA approves Bahri’s merger – The Supreme Council for

Petroleum & Mineral Affairs (SCPMA) has approved the merger

of Vela‟s fleet and operations with the National Shipping

Company of Saudi Arabia (Bahri). (Tadawul)

Saudi CMA approves Bank Al Jazira’s capital increase – The

Saudi CMA board has approved the Bank Al Jazira‟s request to

increase its capital from SR3bn to SR4bn by issuing one bonus

share for every three existing shares. This increase will be paid

by transferring SR500mn from the statutory reserve account and

SR500mn from retained earnings account to the bank‟s capital.

Consequently, the bank's outstanding shares will increase from

300mn to 400mn shares. The bonus shares‟ eligibility is limited

to those shareholders who are registered at the close of trading

on the day of the extraordinary general assembly, which will be

determined later. (Tadawul)

Saudi CMA approves Jadwa’s capital increase – The Saudi

CMA board has approved the Jadwa Investment Company‟s

request to increase its capital from SR568.5mn to SR852.7mn

by capitalizing a part of its retained earnings. (Tadawul)

Al Rajhi Bank’s 1Q2014 profit slips by 16.9% – Al Rajhi Bank

has reported a net profit of SR1.71bn in 1Q2014 as compared to

SR2.05bn in 1Q2013, reflecting 16.9% decline. The bank‟s total

assets stood at SR288bn at the end of 1Q2014 as compared to

SR275bn a year ago. Loans & advances grew by 7% to

SR193bn in 1Q2014 from SR180bn in 1Q2013, while customer

deposits grew by 2.9% to reach SR238.6bn from SR231.8bn.

EPS amounted to SR1.14. (Tadawul)

UAE to issue new law to support SME sector – The UAE

Minister of Economy & Foreign Trade Sultan Al-Mansouri said

the UAE will issue a new law to promote the growth of SMEs. Al-

Mansouri said the new law will require the federal government

agencies to contract with local SMEs for not less than 10% of

the total contracts that meet their purchasing, service and

consulting needs. Al-Mansouri added that as a further incentive

for local SMEs, government-related entities, where the state

owns more than 25% of the capital, will have to grant 5% of their

contract volumes to SMEs. Further, SMEs will also be exempted

from bank guarantees that companies have to pay for each new

worker. The government will also be committed to sponsor and

organize local, specialized exhibitions for SMEs to promote their

products. (Bloomberg)

Dubai airport to cut 26% flights during runway resurfacing

work – Airlines flying into Dubai are preparing for diversions and

schedule changes as the emirate's main airport plans to reduce

the number of flights it handles during construction work on its

4. Page 4 of 5

runways. Dubai's Airports Authority said that the Dubai

International Airport, which handled 66.4mn passengers in 2013,

will cut flights by 26% for an 80-day period. The cut-back will

occur between May 1 and July 20 as both the runways will be

closed one after the other for resurfacing and other construction

work. (Reuters)

Dubai property deals surge to AED60bn in 1Q2014 –

According to the Land Department, property deals in Dubai have

surged by 38% to top AED60bn in 1Q2014. The number of

transactions for the quarter grew to 15,694, indicating 11%

increase over 1Q2013. (GulfBase.com)

DSI Kuwait signs three AED128mn projects deals – Drake &

Scull International‟s (DSI) subsidiary DSI Kuwait has won a

major engineering contract worth AED68mn for Sheikh Jaber Al

Ahmad Cultural Center in Kuwait City. The company further

revealed that it has also bagged an MEP contract worth

AED60mn for a healthcare facility in Shuwaikh and two

commercial developments in Al-Qebla. (DFM)

Abu Dhabi ports expect spike in traffic as projects boom –

Abu Dhabi Ports Company (ADPC) expects a surge in shipping

traffic toward the end of 2014 as work on major infrastructure

projects in the UAE capital gathers pace. ADPC‟s CEO

Mohammad Juma Al Shamisi said that container traffic at

Khalifa Port is expected to climb to around 1.1mn 20-foot

equivalent units (TEUs) in 2014, up 22% from 905,000 TEUs in

2013, when traffic rose 17%. Meanwhile, general and bulk cargo

traffic at the Emirate‟s Khalifa and Zayed ports combined is

expected to top 12mn tons in 2014, up from 9.3mn tons in 2013.

(Bloomberg)

AFNIC declares 7.5% dividend – Al Fujairah National

Insurance Company‟s (AFNIC) AGM has approved its board of

directors‟ recommendation for the distribution of 7.5% dividend

for the year ended December 31, 2013. (ADX)

ADIB arranges AED1.2bn financing for IMG Theme Park –

Abu Dhabi Islamic Bank (ADIB) has arranged and successfully

closed an AED1.2bn syndicated Islamic facility for IMG Theme

Park. The park will be a world-class tourist attraction for 10mn

tourists who visit the UAE every year. ADIB acted as the

mandated lead arranger, investment agent, security agent and

account bank for the facility. The deal was structured by ADIB to

meet lMG Theme Park's specific financing needs, including

refinancing of its existing corporate facility and providing finance

for the expansion of the Worlds of Adventure project. (ADX)

KNPC signs $12bn oil deals; tenders others – The Kuwait

National Petroleum Company (KNPC) signed contracts worth

$12bn with three international consortia to upgrade two

refineries and invited bids to build a new multibillion-dollar

refinery. KNPC‟s Chief Mohamed al-Mutairi signed the contracts

with the three consortia led by Britain‟s Petrofac, US Fluor and

Japan‟s JGC Corp. Most of the other companies in the consortia

are South Korean. Al-Mutairi said the project is due to be

completed in early 2018. Al-Mutairi added that these contracts –

the first mega project in the country‟s oil sector for 25 years –

will upgrade two of the three existing refineries by installing 37

advanced processing units that will reduce sulfur and carbon

pollutants. The current production capacity of the two refineries

of Mina Al-Ahmadi and Mina Abdullah is around 730,000 bpd,

while the capacity of Kuwait‟s third refinery at Shuaiba is

200,000 bpd. (Gulf-Times.com)

NBK reports KD83.9mn net profit in 1Q2014 – The National

Bank of Kuwait (NBK) has reported a net profit of KD83.9mn in

1Q2014 as compared to KD81.3mn in 1Q2013, reflecting an

increase of 3.2%. NBK Group‟s total assets at the end of the

quarter increased by 13.1% to reach KD20.5bn. Loans &

advances reached KD10.95bn at end of 1Q2014 up 9.6% as

compared to 1Q2013, while customer deposits reached

KD11.12bn, up 12.9%. NBK‟s net operating income grew by

7.6% to KD158.4mn. (GulfBase.com)

SAC approves project to boost aluminum output – Sohar

Aluminium Company (SAC) has approved plans for the

implementation of a productivity optimization project that will

boost output by a significant 28,000 tons of primary aluminum

annually. The Amperage Creep Project is one of THE two

important initiatives launched by the company for optimizing

energy efficiency and productivity at its giant smelter located in

Sohar Industrial Area. The other initiative concerns a

comprehensive revamp of the potline designed to achieve a

reduction in energy consumption. (GulfBase.com)

5. Contacts

Saugata Sarkar Keith Whitney Sahbi Kasraoui

Head of Research Head of Sales Manager - HNWI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

(0.9%)

(1.4%)

(0.2%) (0.1%)

0.2%

(0.2%)

(1.7%)

(2.4%)

(1.6%)

(0.8%)

0.0%

0.8%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,318.42 0.0 0.0 9.4 DJ Industrial 16,026.75 0.0 0.0 (3.3)

Silver/Ounce 20.00 0.0 0.0 2.7 S&P 500 1,815.69 0.0 0.0 (1.8)

Crude Oil (Brent)/Barrel (FM

Future)

107.33 0.0 0.0 (3.1) NASDAQ 100 3,999.73 0.0 0.0 (4.2)

Natural Gas (Henry

Hub)/MMBtu

4.65 0.0 0.0 7.1 STOXX 600 328.77 0.0 0.0 0.2

LPG Propane (Arab Gulf)/Ton 111.38 0.0 0.0 (11.8) DAX 9,315.29 0.0 0.0 (2.5)

LPG Butane (Arab Gulf)/Ton 122.00 0.0 0.0 (10.6) FTSE 100 6,561.70 0.0 0.0 (2.8)

Euro 1.39 0.0 0.0 1.0 CAC 40 4,365.86 0.0 0.0 1.6

Yen 101.62 0.0 0.0 (3.5) Nikkei 13,960.05 0.0 0.0 (14.3)

GBP 1.67 0.0 0.0 1.1 MSCI EM 1,015.44 0.0 0.0 1.3

CHF 1.14 0.0 0.0 1.9 SHANGHAI SE Composite 2,130.54 0.0 0.0 0.7

AUD 0.94 0.0 0.0 5.4 HANG SENG 23,003.64 0.0 0.0 (1.3)

USD Index 79.45 0.0 0.0 (0.7) BSE SENSEX 22,628.96 0.0 0.0 6.9

RUB 35.64 0.0 0.0 8.4 Bovespa 51,867.29 0.0 0.0 0.7

BRL 0.45 0.0 0.0 6.5 RTS 1,204.07 0.0 0.0 (16.5)

175.7

151.8

138.0