1. Page 1 of 6

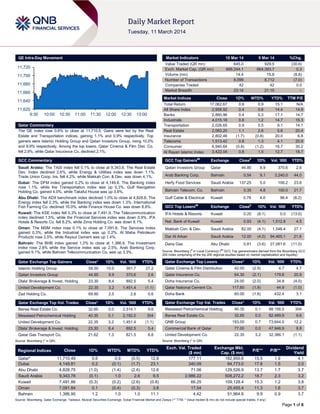

QE Intra-Day Movement

Qatar Commentary

The QE index rose 0.6% to close at 11,710.5. Gains were led by the Real

Estate and Transportation indices, gaining 1.1% and 0.9% respectively. Top

gainers were Islamic Holding Group and Qatari Investors Group, rising 10.0%

and 9.9% respectively. Among the top losers, Qatar Cinema & Film Dist. Co.

fell 2.9%, while Qatar Insurance Co. declined 2.1%.

GCC Commentary

Saudi Arabia: The TASI index fell 0.1% to close at 9,343.8. The Real Estate

Dev. Index declined 2.6%, while Energy & Utilities index was down 1.1%.

Trade Union Coop. Ins. fell 4.2%, while Makkah Con. & Dev. was down 4.1%.

Dubai: The DFM index gained 0.2% to close at 4,149.8. The Banking index

rose 1.1%, while the Transportation index was up 0.3%. Gulf Navigation

Holding Co. gained 4.0%, while Takaful House was up 3.8%.

Abu Dhabi: The ADX benchmark index declined 1.0% to close at 4,828.8. The

Energy index fell 2.3%, while the Banking index was down 1.3%. International

Fish Farming Co. declined 10.0%, while Finance House Co. was down 8.8%.

Kuwait: The KSE index fell 0.3% to close at 7,491.9. The Telecommunication

index declined 1.5%, while the Financial Services index was down 0.9%. IFA

Hotels & Resorts Co. fell 8.2%, while Zima Holding Co. was down 8.1%.

Oman: The MSM index rose 0.1% to close at 7,091.8. The Services Index

gained 0.3%, while the Industrial index was up 0.2%. Al Maha Petroleum

Products rose 2.5%, while Raysut Cement was up 1.4%.

Bahrain: The BHB index gained 1.2% to close at 1,386.9. The Investment

index rose 2.8% while the Service index was up 2.5%. Arab Banking Corp.

gained 9.1%, while Bahrain Telecommunication Co. was up 3.3%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Islamic Holding Group 58.50 10.0 391.7 27.2

Qatari Investors Group 44.85 9.9 370.6 2.6

Dlala' Brokerage & Invest. Holding 23.30 8.4 892.5 5.4

United Development Co. 22.35 3.2 1,451.4 (1.1)

Zad Holding Co. 69.90 2.5 2.6 0.6

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Barwa Real Estate Co. 32.65 0.0 2,514.1 9.6

Mesaieed Petrochemical Holding 40.35 0.1 2,192.0 304

United Development Co. 22.35 3.2 1,451.4 (1.1)

Dlala' Brokerage & Invest. Holding 23.30 8.4 892.5 5.4

Qatar Gas Transport Co. 21.62 1.3 821.5 6.8

Source: Bloomberg (* in QR)

Market Indicators 10 Mar 14 9 Mar 14 %Chg.

Value Traded (QR mn) 645.0 929.5 (30.6)

Exch. Market Cap. (QR mn) 666,244.1 664,393.7 0.3

Volume (mn) 14.4 15.8 (8.8)

Number of Transactions 8,099 8,712 (7.0)

Companies Traded 42 42 0.0

Market Breadth 23:14 21:15 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 17,062.67 0.6 0.9 15.1 N/A

All Share Index 2,958.92 0.4 0.6 14.4 14.9

Banks 2,860.96 0.4 0.3 17.1 14.7

Industrials 4,015.18 0.8 1.2 14.7 15.3

Transportation 2,026.65 0.9 0.5 9.1 14.1

Real Estate 2,063.20 1.1 2.6 5.6 20.4

Insurance 2,802.46 (1.7) (0.8) 20.0 6.8

Telecoms 1,513.42 0.8 1.3 4.1 20.9

Consumer 6,940.64 (0.8) (1.2) 16.7 30.2

Al Rayan Islamic Index 3,422.04 0.8 1.5 12.7 18.7

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Qatari Investors Group Qatar 44.85 9.9 370.6 2.6

Arab Banking Corp. Bahrain 0.54 9.1 3,240.0 44.0

Herfy Food Services Saudi Arabia 137.25 5.0 106.2 23.6

Bahrain Telecom. Co. Bahrain 0.35 4.8 100.0 21.7

Gulf Cable & Electrical Kuwait 0.78 4.0 96.4 (8.2)

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

IFA Hotels & Resorts Kuwait 0.25 (8.1) 0.0 (13.0)

Nat. Bank of Kuwait Kuwait 0.93 (4.1) 1,512.8 4.5

Makkah Con. & Dev. Saudi Arabia 82.00 (4.1) 1,548.4 27.1

Dar Al Arkan Saudi Arabia 12.00 (4.0) 94,465.1 21.8

Dana Gas Abu Dhabi 0.81 (3.6) 27,081.6 (11.0)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar Cinema & Film Distribution 42.00 (2.9) 4.7 4.7

Qatar Insurance Co. 64.30 (2.1) 179.6 20.9

Doha Insurance Co. 24.00 (2.0) 34.8 (4.0)

Qatar National Cement Co. 117.80 (1.8) 44.9 (1.0)

Doha Bank 60.00 (1.6) 432.4 3.1

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Mesaieed Petrochemical Holding 40.35 0.1 88,156.5 304

Barwa Real Estate Co. 32.65 0.0 82,489.9 9.6

QNB Group 193.00 0.7 73,644.0 12.2

Commercial Bank of Qatar 77.00 0.0 47,946.9 8.8

United Development Co. 22.35 3.2 32,386.1 (1.1)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 11,710.49 0.6 0.9 (0.5) 12.8 177.11 182,950.6 15.5 1.9 4.1

Dubai 4,149.81 0.2 (0.1) (1.7) 23.1 340.09 84,773.0 17.8 1.5 2.0

Abu Dhabi 4,828.75 (1.0) (1.4) (2.6) 12.6 71.06 129,526.9 13.7 1.7 3.7

Saudi Arabia 9,343.78 (0.1) 1.0 2.6 9.5 2,986.22 508,272.2 18.7 2.3 3.2

Kuwait 7,491.86 (0.3) (0.2) (2.6) (0.8) 66.25 109,128.4 15.3 1.2 3.8

Oman 7,091.84 0.1 (0.4) (0.3) 3.8 17.54 25,455.4 11.3 1.6 3.7

Bahrain 1,386.90 1.2 1.0 1.0 11.1 4.42 51,964.6 9.9 0.9 3.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,620

11,640

11,660

11,680

11,700

11,720

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QE index rose 0.6% to close at 11,710.5. The Real Estate

and Transportation indices led the gains. The index rose on the

back of buying support from non-Qatari shareholders despite

selling pressure from Qatari shareholders.

Islamic Holding Group and Qatari Investors Group were the top

gainers, rising 10.0% and 9.9% respectively. Among the top

losers, Qatar Cinema & Film Dist. Co. fell 2.9%, while Qatar

Insurance Co. declined 2.1%.

Volume of shares traded on Monday fell by 8.8% to 14.4mn from

15.8mn on Sunday. However, as compared to the 30-day

moving average of 12.9mn, volume for the day was 11.5%

higher. Barwa Real Estate Co. and Mesaieed Petrochemical

Holding Co. were the most active stocks, contributing 17.4% and

15.2% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Dubai Islamic

Insurance Co.

S&P Dubai LT Local Issuer Credit BBB- BB+ – –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC –

Local Currency)

Earnings Releases

Company Market Currency

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

Emirates Refreshments

(ERC)*

Dubai AED 68.8 23.5% 0.7 58.6% 0.5 -28.9%

Union Insurance Co. (UIC)* Abu Dhabi AED 353.7#

40.3% – – 66.7 NA

Source: Company data, DFM, ADX, MSM (*FY 2013 results) (# Gross Insurance Premium Revenue)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

03/10 EU Sentix Behavioral Ind. Sentix Investor Confidence March 13.9 14.0 13.3

03/10 France INSEE Industrial Production MoM January -0.20% 0.30% -0.60%

03/10 France INSEE Industrial Production YoY January -0.10% 1.30% 0.30%

03/10 France INSEE Manufacturing Production MoM January 0.70% 0.30% 0.00%

03/10 France INSEE Manufacturing Production YoY January 1.40% 1.40% 0.50%

03/10 UK Lloyds Bank Lloyds Employment Confidence February -2.0 – -2.0

03/10 Spain INE Industrial Output NSA YoY January -0.10% 4.30% 3.90%

03/10 Spain INE Industrial Output SA YoY January 1.10% 1.80% 2.20%

03/10 Italy ISTAT Industrial Production MoM January 1.00% 0.50% -0.80%

03/10 Italy ISTAT Industrial Production WDA YoY January 1.40% -0.30% -0.70%

03/10 Italy ISTAT Industrial Production NSA YoY January -1.70% – 2.40%

03/10 China The People's Bank Money Supply M1 YoY February 6.90% 7.00% 1.20%

03/10 China The People's Bank Money Supply M2 YoY February 13.30% 13.20% 13.20%

03/10 China The People's Bank Money Supply M0 YoY February 3.30% 7.70% 22.50%

03/10 Japan ESRI GDP SA QoQ 4Q2013 0.20% 0.20% 0.30%

03/10 Japan ESRI GDP Annualized SA QoQ 4Q2013 0.70% 0.90% 1.00%

03/10 Japan ESRI GDP Nominal SA QoQ 4Q2013 0.30% 0.40% 0.40%

03/10 Japan ESRI GDP Deflator YoY 4Q2013 -0.30% -0.40% -0.40%

03/10 Japan ESRI GDP Consumer Spending QoQ 4Q2013 0.40% – 0.50%

03/10 Japan ESRI GDP Business Spending QoQ 4Q2013 0.80% – 1.30%

03/10 Japan Bank of Japan Bank Lending Incl Trusts YoY February 2.20% 2.40% 2.30%

03/10 Japan Bank of Japan Bank Lending Ex-Trusts YoY February 2.40% – 2.50%

03/10 Japan ESRI Eco Watchers Survey Current February 53.0 54.1 54.7

03/10 Japan ESRI Eco Watchers Survey Outlook February 40.0 50.5 49.0

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 65.88% 68.40% (16,226,195.06)

Non-Qatari 34.12% 31.60% 16,226,195.06

3. Page 3 of 6

News

Qatar

QCB Governor: Economic boom, spending drive augur well

for Qatari insurance – Qatar‟s financial regulator said that the

country‟s positive medium-term economic prospects and huge

project spending augur well for the insurance and reinsurance

industry. The Qatar Central Bank‟s (QCB) Governor and Qatar

Financial Market Authority‟s Chairman HE Sheikh Abdullah bin

Saud al-Thani said that economic prospects in Qatar are quite

positive in the medium term. He said overall there has been

positive economic momentum, particularly in the non-oil

segment. Sheikh Abdullah said that insurance and reinsurance

were important partners as Qatar has embarked on mammoth

infrastructure projects ahead of its preparations to host the 2022

FIFA World Cup. (Gulf-Times.com)

MDPS: Qatar PPI rises 1.6% in 4Q2013 on higher oil, gas

and basic chemical prices – Higher prices for crude oil, natural

gas, utilities and basic chemicals led Qatar‟s Producer Price

Index (PPI) to rise about 1.6% YoY in 4Q2013. The Ministry of

Development Planning & Statistics (MDPS) released the PPI for

the industrial sector, which measures the average price changes

received by domestic producers for their output. The PPI for

mining (77% weight in the PPI basket) was up 1.4% YoY in

4Q2013 due to a 1.4% rise in the price of crude petroleum and

gas, as well as a 2.6% rise in stone, sand and clay. The

manufacturing sector (21% weight in PPI), reported a 2.3% gain

YoY in 4Q2013 due to an 8.8% jump in the prices of basic

chemicals, 0.6% in refined petroleum products and 0.2% in

cement and other non-metallic products. Prices fell for dairy

products (3.1%), grain mill & beverages (0.9% each) and basic

metals (0.6%). The electricity & water group (2% weight in PPI)

saw its index surge 5.4% YoY in 4Q2013 powered by 5.7% and

4.8% rise in the prices of electricity and water respectively.

(Gulf-Times.com)

ERES acquires 20% of IHGS shares – Ezdan Holding Group

(ERES) has acquired more than 20% of the Islamic Holding

Group‟s (IHGS) shares from the Qatar Exchange. IHGS mainly

invests in shares and bonds, and providing brokerage services

on the Qatar Exchange based on Shari‟ah principles and done

through Islamic Finance Securities Company. IHGS owns many

companies, which will enhance the profitability of Ezdan Holding

Group. ERES‟ Chairman Sheikh Dr Khalid bin Thani bin

Abdullah al-Thani said the deal comes within the framework of

the group‟s keenness to diversify its investment portfolio and

demonstrate professionalism in the market. (Gulf-Times.com)

Doha airport’s passenger growth up 18% – Doha

International Airport (DIA) has clocked a record number of

2.19mn passengers in January 2014, up nearly 18% on the

same period last year. DIA said that it had successfully

increased its passenger traffic by 10% YoY in 2013. Cargo

traffic also saw a substantial 12.1% increase in January. The

data highlights the DIA‟s enhanced cargo facility and transport

capabilities, with the introduction of QR Pharma and QR Fresh

that are designed to optimize the transportation of time and

temperature sensitive goods. January also brought a notable

7.39% growth in aircraft movements at the DIA compared to

January the previous year. (Gulf-Times.com)

Kahramaa: Water reservoirs project cost likely to increase

by 15% – A senior official of Qatar General Electricity & Water

Corporation (Kahramaa) said that the cost of the project to build

20 huge reservoirs at five strategic sites in Qatar is likely to be

higher by 15% from the initial estimate of QR11bn. Kahramaa‟s

Manager, Water Projects Department, Mohammed Salme Al

Mansoori said this increase is due to rising cost of raw materials,

including sand, cement, bitumen. Al Mansoori stated that

keeping prices under control will be quite challenging since a lot

of big projects, including those of Qatar Rail and Ashghal, are

simultaneously under construction. So prices are expected to

steadily rise until 2017. (Peninsula Qatar)

Trading suspension in QIIK’s shares on March 11 – The

Qatar Exchange (QE) announced the suspension in the trading

of Qatar International Islamic Bank‟s (QIIK) shares on March 11,

2014 due to its AGM scheduled on that day. (QE)

Trading suspension in GISS’ shares on March 11 – The

Qatar Exchange (QE) announced the suspension in the trading

of Gulf International Services Company‟s (GISS) shares on

March 11, 2014 due to its AGM and EGM being held on that

day. (QE)

QBIC aims to reach out to entrepreneurs – The Qatar

Business Incubation Centre (QBIC) aims to reach out to at least

330 Qatari entrepreneurs and 150 local companies over a three-

year period to help them become the next QR100mn companies

in the country. QBIC's Chief Executive Officer Raed al-Emadi

said that QBIC will provide incubator space for entrepreneurs

and scale-ups to carry out their work assignments with their

teams. In addition, QBIC provide balanced training courses that

enrich both knowledge and expertise. The start-ups will be able

to avail up to QR200,000, while established local companies can

secure financing of up to QR4mn through QBIC's partnership

with Qatar Development Bank (QDB). (Gulf-Times.com)

Ooredoo chairman appointed to WB gender panel –

Ooredoo‟s Chairman HE Sheikh Abdullah bin Mohamed bin

Saud al-Thani has been appointed to the World Bank (WB)

Group‟s Advisory Council on Gender and Development. This is

the first time that a representative from the Middle East has

been named to this global body that is dedicated to promoting

gender equality around the world. (Gulf-Times.com)

International

White House has optimistic growth forecast for 2014, 2015 –

The White House has forecast a more robust economic growth

in 2014 than last year and a further pickup in the US economy

for 2015. The US economy is expected to expand by 3.1% this

year, faster than last year's 1.7%. The White House said growth

would pick up to 3.4% in 2015. The administration also forecast

that unemployment would settle to an average of 6.9% in 2014.

The jobless rate, which reached a high of 10% in 2009, fell to a

five-year low of 6.6% in January. Many economists say that the

unemployment rate has dropped in part because many people

have stopped looking for work. The US labor force participation

rate has fallen from 66% before the start of the recession to

63%. (Reuters)

EU Finance Ministers claim progress on bank-failure fund –

Finance ministers of the European Union (EU) claimed good

progress in talks in Brussels as they worked toward breaking a

deadlock on a Eurozone bank-failure regulation that is urgently

sought by the European Central Bank (ECB). The EU is

searching for a compromise on the Single Resolution

Mechanism and an accompanying common fund to cover the

cost of saving or closing banks. The ECB President Mario

Draghi warned that a failure to reach a deal before the European

Parliament elections in May 2014 would have serious

consequences for the Eurozone and its fledgling banking union.

(Bloomberg)

BoE: Stronger sterling could delay interest rate rise – The

Bank of England‟s (BoE) Deputy Governor Charlie Bean said

BoE could keep its interest rates lower for longer if the pound

4. Page 4 of 6

sterling strengthens much more. Bean said that the currency's

current level was fine, but that Britain would find it harder to

enjoy a solid export-based recovery if the currency strengthened

any more. He also cautioned about the eagerness as to when

the central bank will raise interest rates from its record low of

0.5%, after financial markets and other policymakers indicated

the 2015 spring as a possibility. Bean further added that Britain's

economy was recovering, but these are still early days as the

country‟s trade deficit needs to narrow down to put growth on a

more solid footing. Bean said any further appreciation of sterling,

which has risen almost 10% in trade-weighted terms since

March 2013, would not be helpful in terms of facilitating a

rebalancing toward net exports. (Reuters)

BoJ expected to maintain stimulus – The Bank of Japan

(BoJ) is expected to maintain its massive monetary stimulus

since it views the Japanese economy can weather the sales tax

increase scheduled in April without extra support, although there

is some concern about weakness in exports. The BoJ‟s board

can point to strength in industrial output, labor demand and

consumer spending to back its view the economy will continue a

gradual recovery and its 2% inflation target is achievable over

the next 12 months or so. There is some concern within the BoJ

about slow exports, but pessimists are not expected to have the

numbers to tip the votes towards a downgrade of the central

bank's stance that export growth will eventually rebound.

(Reuters)

PBoC sees deposit rate liberalization in two years; bank

lending halves after spike in January – The People's Bank of

China (PBoC) Governor Zhou Xiaochuan said China is likely to

liberalize bank deposit rates in one to two years. Xiaochuan also

said that interest rates will initially rise as controls are removed.

There has been widespread market talk that the central bank is

quietly loosening policy to support economic growth as short-

term money rates and the Chinese yuan weakened this week

after surprisingly weak exports data came in at the weekend.

Meanwhile, official data showed that the number of new yuan

loans offered by Chinese banks halved in February and liquidity

in the economy tightened, which according to analysts indicated

that the previous month's surge was not a sign of a policy shift.

The PBoC said new bank loans totaled 644.5bn yuan in

February, down from 1.3tn yuan in January. Total social

financing, a broad measure of liquidity and credit, fell sharply to

938.7bn yuan from January's 2.58tn yuan. (Reuters, Bloomberg)

Regional

QNB Group: Jordan sees fast recovery – According to QNB

Group, the Jordanian economy is recovering from the crisis

suffered in 2012 due to support from the IMF and GCC

countries. The Central Bank of Jordan‟s international reserves

have more than doubled in 2013 and economic activity is picking

up. QNB Group said that on this basis, the country‟s real GDP

growth is expected to accelerate from an estimated 2.9% in

2013 to 3.6% in 2014 and to average 4.4% during 2015-16. This

growth will be driven by a private sector-led growth in the

construction sector, lower energy costs, a recovery in tourism, a

normalization of mining exports as well as growth in other

services. However the long-term outlook is still below the

economy‟s full potential. This is mainly due to political

challenges such as the impact of flow of Syrian refugees into

Jordan and the Jordanian government‟s budget deficit.

(Peninsula Qatar)

Markaz: Gulf Islamic banking accounts for 28.7% of $1.5tn

global assets – According to a report by Kuwait Financial

Centre (Markaz), Islamic banking assets in the Gulf region now

account for roughly 28.7% of global Shari‟ah-compliant assets,

which have crossed $1.5tn. Markaz said that Islamic banking

has been witnessing high levels of growth in recent years, but at

the same time, the industry has faced criticism for lack of

standardization and non-adherence to pure Islamic financing

practices. Given the emphasis on tangible assets and business

models, rather than creditworthiness, Islamic banking is seen as

less speculative than its conventional counterpart. The Markaz

study said given the head-start that conventional banks have

had, it is no surprise that they account for roughly 80% of the

region‟s banking assets. The overall GCC banking sector

accounts for 94% of nominal GDP in 2013. (Gulf-Times.com)

Al Khalaf invests in Canon technology – Al Khalaf Advertising

& Press Company has signed a deal with Al Eqtessad Holding

Company, to invest in the cutting-edge Canon Océ Inkjet UV-

Flatbed print technology. Al Eqtessad will install and service the

Canon Océ Arizona large format UV-flatbed 460GT printer at Al

Khalaf, which will enable the company to deliver better services

to its customers from the private and public sectors alike.

(GulfBase.com)

DSOA launches AED1.1bn Silicon Park project – The Dubai

Silicon Oasis Authority (DSOA) has launched the „Silicon Park‟,

the first integrated smart city project to be built inside Dubai

Silicon Oasis at a cost of AED1.1bn. DSOA‟s Chairman, Sheikh

Ahmed bin Saeed Al Maktoum said that the project will be

completed by 4Q2017. The Silicon Park project comprises

97,000 square meters of office space, 25,000 square meters of

commercial space, 20,000 square meters of residential area and

a 115 rooms business hotel. (GulfBase.com)

Emaar to launch Mulberry second phase – Emaar Properties

will launch the second phase of its Mulberry at Park Heights

development in the Dubai Hills Estate this week. Emaar is

developing the project in a joint venture with Meraas Holding.

The second phase, set in Mohammed Bin Rashid City, will

feature around 330 premium quality apartments, an 18-hole golf

course, a tennis academy, swimming pool, and jogging and

cycle tracks. (GulfBase.com)

Emirates launches Dubai–Boston route – The Emirates

Airline has launched a daily, non-stop service to Boston, which

will be its eighth destination in the US. For this new route,

Emirates will operate daily flights between Dubai and Boston

using a Boeing 777-200LR aircraft in a three-class configuration,

with 8 seats in first class, 42 in business class and 216 in

economy. (GulfBase.com)

Emirates SkyCargo to launch service to Abidjan, Tunis –

The Emirates Airline‟s freight division, Emirates SkyCargo, is set

to increase its cargo capacity to Tunis and Abidjan in Africa with

the introduction of a weekly freighter service from March 17,

2014. The new freighter flight will supplement the existing belly

hold cargo capacity provided on Emirates‟ daily passenger

services to the two cities. Emirates SkyCargo currently offers

200 tons of capacity each week on the Tunis route, while the

Abidjan route offers 300 tons. (GulfBase.com)

Dubai Exports to launch Halal Index – The Dubai Export

Development Corporation‟s (Dubai Exports) CEO, Saeed Al

Awadi, said that the corporation is planning to issue an online

Halal index to list all UAE-based halal firms. The index will

include relevant information about all the Shari‟ah compliant

companies such as banks, financial institutions, Islamic products

and services in Dubai. (GulfBase.com)

Deyaar launches The Atria at Business Bay – Dubai-based

Deyaar Development announced its first foray into the hospitality

sector as the company launched the AED900mn “The Atria at

Business Bay”. The 1.25-million square feet twin-tower project

5. Page 5 of 6

comprises luxury serviced apartments and residential units. The

project is expected to be completed in 1Q2017. Deyaar signed

up with a global design, development and branding firm Yoo

Studio, for 350 serviced apartments and 219 apartments at The

Atria project. (Bloomberg)

Aldar to develop AED5.7bn national housing projects –

Aldar Properties announced that its current pipeline of National

Housing projects being developed on behalf of the Abu Dhabi

Government totals 2,300 units worth AED5.7bn. The projects

are fully funded by the Abu Dhabi Government. The current

projects under construction include two large developments in

Abu Dhabi and one in Al Ain, which are expected to be

completed in 2016. The projects consist of 1,020 villas on Yas

Island and 996 villas in Al Falah and 275 Villas at Al Ghuraibah

in Al Ain. (ADX)

NDC acquires AED120mn drilling rig from NOV – The

National Drilling Company (NDC) has signed an agreement with

National Oilwell Varco (NOV) to acquire a new land rig valued at

approximately AED120mn. The agreement will help NDC to

meet the needs of its client, the Abu Dhabi Company for

Onshore Oil Operations (ADCO), and step-up the company's

ability to perform specific drilling operations. (GulfBase.com)

Kuwait’s budget spending up 8%, below full-year plan –

According to preliminary finance ministry figures, Kuwait‟s

government spending rose 8% in the first 10 months of this

fiscal year as compared to the same period the previous year,

but is still far below its initial plan. The major oil exporting

country‟s public expenditure reached KD10.58bn in the April-

January period, up from KD9.78bn a year ago, but little over half

of its spending plan of KD21bn for the fiscal year ending in

March. Kuwait has been undershooting its budget plans as

political wrangling delays budget approvals in parliament and

investment spending. (Gulf-Base.com)

NBK declares 30% cash dividend, 5% bonus shares – The

National Bank of Kuwait‟s (NBK) AGM has approved its board

recommendation to distribute 30% cash dividends (30 fils per

share) and 5% bonus shares to the shareholders.

(GulfBase.com)

Oman to divest stake in 11 state-owned companies – Omani

CMA‟s Executive President, Sheikh Abdullah bin Salem Al

Salmi, said that the Omani government is planning to divest its

stake in as many as 11 state-owned companies via IPOs. This

stake sale is in an apparent move to spur market trading and

pass on the corporate earnings benefits to Omani nationals. Al

Salmi noted that the state-owned companies that are planning

IPOs are unlisted currently, but declined to name the

companies. However, the first company to offer shares on the

MSM is the state-owned Oman Telecommunications Company

(Omantel), which is offering 142.5mn shares (19% of

government ownership in the company). Meanwhile, the Omani

government is planning to restructure the ownership pattern of

65 state-owned companies into four or five holding companies

for enhancing administrative efficiency and strengthening

controls. (GulfBase.com)

NCSI: Oman’s foreign trade rises by 9.1% – According to the

statistics released by the National Centre for Statistics &

Information (NCSI), Oman's foreign trade witnessed a 9.1%

increase in the total value of commodity exports at the end of

November 2013, as compared to November 2012. The total

value of commodity exports stood at OMR19,838mn at the end

of November 2013, against OMR18,186.5mn in November

2012. This increase was attributed to a 3.4% increase in oil &

gas exports, which amounted to OMR13,093.4mn in November

2013, as compared to OMR12,668.2mn in December 2012.

During this period, Oman's non-oil exports increased by 7.1% to

OMR3,492.2mn as compared to OMR3,260.1mn. Re-export

trade rose by 44% to hit OMR3,252.4mn as compared to

OMR2,258.2mn in 2012. The NCSI statistics added that the

UAE topped the countries that imported Omani non-oil exports.

(GulfBase.com)

Al Batinah declares 7% bonus shares – Al Batinah Hotels

Company‟s AGM has approved its board‟s proposal to distribute

7% bonus shares. This will increase the company‟s capital from

OMR3,384.9bn to OMR3,621.9bn. (MSM)

GFH to start $3bn Tunisia project – Gulf Finance House

(GFH) plans to start building a $3bn financial park and real

estate development north of Tunisia's capital, Tunis. The

project, billed as the first financial park in North Africa, was

scheduled to begin in 2009, but had been suspended for five

years. The project known as „Tunis Financial Harbour‟ would

cover 450 hectares in the Raoued suburb of Tunis, which will be

one of the largest private foreign investments in the North

African state. The site will contain a corporate center,

investment banking and advisory center and an insurance area.

It will also include homes, offices, a golf course, a business

school and trade centers. It is expected to create 17,000 jobs.

(GulfBase.com)

NBB declares 35% cash dividend – The National Bank of

Bahrain‟s (NBB) has approved its board‟s proposal for

distributing 35% cash dividends (35 fils per share). (Bahrain

Bourse)

6. Contacts

Saugata Sarkar Ahmed M. Shehada Keith Whitney Sahbi Kasraoui

Head of Research Head of Trading Head of Sales Manager - HNWI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6535 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa ahmed.shehada@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg (* Market closed on March 10, 2014) Source: Bloomberg (* Market closed on March 10, 2014)

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

(0.1%)

0.6%

(0.3%)

1.2%

0.1%

(1.0%)

0.2%

(1.2%)

(0.8%)

(0.4%)

0.0%

0.4%

0.8%

1.2%

1.6%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,339.72 (0.0) (0.0) 11.1 DJ Industrial 16,418.68 (0.2) (0.2) (1.0)

Silver/Ounce 20.82 (0.4) (0.4) 6.9 S&P 500 1,877.17 (0.0) (0.0) 1.6

Crude Oil (Brent)/Barrel (FM

Future)

108.08 (0.8) (0.8) (2.5) NASDAQ 100 4,334.45 (0.0) (0.0) 3.8

Natural Gas (Henry

Hub)/MMBtu

4.63 (3.0) (3.0) 6.5 STOXX 600 331.40 (0.5) (0.5) 1.0

North American Spot LPG

Propane Price*

108.50 0.0 0.0 (14.2) DAX 9,265.50 (0.9) (0.9) (3.0)

North American Spot LPG

Normal Butane Price*

121.00 0.0 0.0 (10.9) FTSE 100 6,689.45 (0.3) (0.3) (0.9)

Euro 1.39 0.0 0.0 1.0 CAC 40 4,370.84 0.1 0.1 1.7

Yen 103.27 (0.0) (0.0) (1.9) Nikkei 15,120.14 (1.0) (1.0) (7.2)

GBP 1.66 (0.4) (0.4) 0.5 MSCI EM 955.02 (1.2) (1.2) (4.8)

CHF 1.14 0.1 0.1 1.7 SHANGHAI SE Composite 1,999.07 (2.9) (2.9) (5.5)

AUD 0.90 (0.5) (0.5) 1.2 HANG SENG 22,264.93 (1.7) (1.7) (4.5)

USD Index 79.77 0.1 0.1 (0.3) BSE SENSEX 21,934.83 0.1 0.1 3.6

RUB 36.35 (0.3) (0.3) 10.6 Bovespa 45,533.20 (1.5) (1.5) (11.6)

BRL 0.43 (0.5) (0.5) 0.5 RTS* 1,158.87 0.0 0.0 (19.7)

168.3

145.5

132.6