Independent Lucknow Call Girls 8923113531WhatsApp Lucknow Call Girls make you...

11 March Daily market report

1. Page 1 of 5

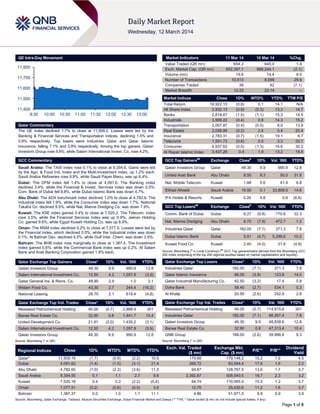

QE Intra-Day Movement

Qatar Commentary

The QE index declined 1.7% to close at 11,509.2. Losses were led by the

Banking & Financial Services and Transportation indices, declining 1.5% and

0.9% respectively. Top losers were Industries Qatar and Qatar Islamic

Insurance, falling 7.1% and 3.9% respectively. Among the top gainers, Qatari

Investors Group rose 9.9%, while Salam International Invest. Co. rose 4.2%.

GCC Commentary

Saudi Arabia: The TASI index rose 0.1% to close at 9,354.6. Gains were led

by the Agri. & Food Ind. Index and the Multi-Investment index, up 1.2% each.

Saudi Arabia Refineries rose 9.8%, while Saudi Paper Manu. was up 6.4%.

Dubai: The DFM index fell 1.4% to close at 4,091.6. The Banking index

declined 3.4%, while the Financial & Invest. Services index was down 2.0%.

Com. Bank of Dubai fell 9.8%, while Dubai Islamic Bank was down 4.7%.

Abu Dhabi: The ADX benchmark index declined 1.0% to close at 4,782.6. The

Industrial index fell 1.9%, while the Consumer index was down 1.7%. National

Takaful Co. declined 9.5%, while Nat. Marine Dredging Co. was down 7.9%.

Kuwait: The KSE index gained 0.4% to close at 7,520.2. The Telecom. index

rose 3.5%, while the Financial Services index was up 0.9%. Jeeran Holding

Co. gained 9.6%, while Egypt Kuwait Holding Co. was up 8.9%.

Oman: The MSM index declined 0.2% to close at 7,077.5. Losses were led by

the Financial Index, which declined 0.5%, while the Industrial index was down

0.1%. Al Batinah Dev. declined 4.3%, while Gulf Inter. Chem. was down 3.9%.

Bahrain: The BHB index rose marginally to close at 1,387.4. The Investment

index gained 0.6%, while the Commercial Bank index was up 0.2%. Al Salam

Bank and Arab Banking Corporation gained 1.9% each.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatari Investors Group 49.30 9.9 990.9 12.8

Salam International Investment Co. 12.50 4.2 1,057.9 (3.9)

Qatar General Ins. & Reins. Co. 48.90 2.9 1.0 2.1

Widam Food Co. 43.30 2.7 244.4 (16.2)

National Leasing 28.70 2.1 618.4 (4.8)

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Mesaieed Petrochemical Holding 40.05 (0.7) 2,868.4 301

Barwa Real Estate Co. 32.90 0.8 1,441.7 10.4

United Development Co. 21.91 (2.0) 1,435.2 (3.1)

Salam International Investment Co. 12.50 4.2 1,057.9 (3.9)

Qatari Investors Group 49.30 9.9 990.9 12.8

Source: Bloomberg (* in QR)

Market Indicators 11 Mar 14 10 Mar 14 %Chg.

Value Traded (QR mn) 654.3 645.0 1.4

Exch. Market Cap. (QR mn) 652,397.1 666,244.1 (2.1)

Volume (mn) 15.6 14.4 8.5

Number of Transactions 10,513 8,099 29.8

Companies Traded 39 42 (7.1)

Market Breadth 12:23 23:14 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 16,922.15 (0.8) 0.1 14.1 N/A

All Share Index 2,932.13 (0.9) (0.3) 13.3 14.7

Banks 2,818.67 (1.5) (1.1) 15.3 14.5

Industrials 3,999.22 (0.4) 0.8 14.3 15.2

Transportation 2,007.87 (0.9) (0.5) 8.0 13.9

Real Estate 2,058.99 (0.2) 2.4 5.4 20.4

Insurance 2,783.31 (0.7) (1.5) 19.1 6.7

Telecoms 1,501.73 (0.8) 0.5 3.3 20.7

Consumer 6,937.62 (0.0) (1.3) 16.6 30.2

Al Rayan Islamic Index 3,437.26 0.4 1.9 13.2 18.8

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Qatari Investors Group Qatar 49.30 9.9 990.9 12.8

United Arab Bank Abu Dhabi 8.50 8.3 50.0 31.8

Nat. Mobile Telecom. Kuwait 1.88 5.6 41.9 6.8

Etihad Atheeb Saudi Arabia 16.50 5.1 33,809.5 14.6

IFA Hotels & Resorts Kuwait 0.26 4.8 0.6 (8.8)

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Comm. Bank of Dubai Dubai 6.27 (9.8) 770.8 32.3

Nat. Marine Dredging Abu Dhabi 8.70 (7.9) 472.7 1.2

Industries Qatar Qatar 182.00 (7.1) 371.3 7.8

Dubai Islamic Bank Dubai 5.91 (4.7) 5,299.6 10.3

Kuwait Food Co. Kuwait 2.40 (4.0) 31.8 (4.8)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Industries Qatar 182.00 (7.1) 371.3 7.8

Qatar Islamic Insurance 66.00 (3.9) 123.8 14.0

Qatar Industrial Manufacturing Co. 42.50 (3.2) 17.4 0.8

Doha Bank 58.40 (2.7) 534.1 0.3

Al Khaliji 20.55 (2.6) 252.9 2.8

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Mesaieed Petrochemical Holding 40.05 (0.7) 114,815.6 301

Industries Qatar 182.00 (7.1) 68,267.4 7.8

Qatari Investors Group 49.30 9.9 48,838.6 12.8

Barwa Real Estate Co. 32.90 0.8 47,313.4 10.4

QNB Group 188.00 (2.6) 39,998.8 9.3

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 11,509.16 (1.7) (0.8) (2.2) 10.9 179.68 179,148.2 15.2 1.9 4.5

Dubai 4,091.62 (1.4) (1.5) (3.1) 21.4 266.72 83,594.4 17.6 1.5 2.2

Abu Dhabi 4,782.60 (1.0) (2.3) (3.6) 11.5 94.67 128,767.5 13.6 1.7 3.7

Saudi Arabia 9,354.55 0.1 1.1 2.7 9.6 2,392.87 508,540.5 18.7 2.3 3.2

Kuwait 7,520.16 0.4 0.2 (2.2) (0.4) 84.74 110,065.5 15.5 1.2 3.7

Oman 7,077.51 (0.2) (0.6) (0.5) 3.6 12.70 25,430.6 11.2 1.6 3.7

Bahrain 1,387.37 0.0 1.0 1.1 11.1 4.86 51,971.5 9.9 0.9 3.9

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,400

11,500

11,600

11,700

11,800

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 5

Qatar Market Commentary

The QE index declined 1.7% to close at 11,509.2. The Banking &

Financial Services and Transportation indices led the losses. The

index fell on the back of selling pressure from non-Qatari

shareholders despite buying support from Qatari shareholders.

Industries Qatar and Qatar Islamic Insurance were the top

losers, falling 7.1% and 3.9% respectively. Among the top

gainers, Qatari Investors Group rose 9.9%, while Salam

International Invest. Co. rose 4.2%.

Volume of shares traded on Tuesday rose by 8.5% to 15.6mn

from 14.4mn on Monday. Further, as compared to the 30-day

moving average of 13.0mn, volume for the day was 19.9%

higher. Mesaieed Petrochemical Holding Co. and Barwa Real

Estate Co. were the most active stocks, contributing 18.3% and

9.2% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

Al-Khabeer Capital (AKC)* Saudi SR 125.0 NA – – 43.3 NA

Eshraq Properties Co.* Abu Dhabi AED 716.6 26.0% – – 318.7 11.5%

Abu Dhabi Ship Building

(ADSB)*

Abu Dhabi AED 1,118.6 -12.4% – – 48.0 78.2%

National Hospitality Institute

(NHI)*

Oman OMR 0.7 -4.8% – – – –

Kuwait Consulting and

Investment Co. (KCIC)*

Kuwait KD 7.8 NA – – 1.0 NA

Source: Company data, DFM, ADX, MSM (*FY2013 results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

03/11 US BLS JOLTs Job Openings January 4015 3914 3914

03/11 US US Census Bureau Wholesale Inventories MoM January 0.40% 0.40% 0.40%

03/11 US US Census Bureau Wholesale Trade Sales MoM January 0.20% 0.10% 0.10%

03/11 Germany Destatis Labor Costs WDA YoY 4Q2013 – 1.90% 1.90%

03/11 Germany Destatis Trade Balance January 15.0B 13.9B 13.9B

03/11 Germany Deutsche Bundesbank Exports SA MoM January 1.50% -0.90% –

03/11 Germany Deutsche Bundesbank Imports SA MoM January 1.40% -1.40% -1.40%

03/11 UK UK Office for Nat. Statist Industrial Production MoM January 0.20% 0.50% 0.50%

03/11 UK UK Office for Nat. Statist Industrial Production YoY January 3.00% 1.90% 1.90%

03/11 UK UK Office for Nat.Statist Manufacturing Production MoM January 0.30% 0.40% 0.40%

03/11 UK UK Office for Nat.Statist Manufacturing Production YoY January 3.30% 1.40% 1.40%

03/11 UK Nat. Institute of Eco. NIESR GDP Estimate February – 0.70% 0.70%

03/11 Italy ISTAT GDP WDA QoQ 4Q2013 0.10% 0.10% –

03/11 Italy ISTAT GDP WDA YoY 4Q2013 -0.80% -0.80% –

03/11 Japan Bank of Japan Money Stock M2 YoY February 4.40% 4.30% 4.30%

03/11 Japan Bank of Japan Money Stock M3 YoY February 3.50% 3.50% –

03/11 Japan JMTBA Machine Tool Orders YoY February – 40.30% –

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

Qatar Rail awards €506mn Doha Metro contract – The Qatar

Railways Company has awarded a €506mn contract to build

three stations and a 6.97-kilometer long stretch of the Doha

Metro to a consortium led by Spain's FCC. The consortium is

made up of FCC, Greece-based Archirodon, Turkey-based

Yuksel and Petroserv of Qatar. The execution period of the

contract is 31 months, which includes building three elevated

stations at Barwa Village, Al Wakrah and the Qatar Economic

Zone, and tunneling the road at the entrance to Al Wakrah.

(GulfBase.com)

IQCD AGM approves 110% cash dividend – Industries Qatar‟s

(IQCD) AGM has approved the board‟s recommendation for

110% cash dividend, representing QR11.00 per share. (QE)

QIIK to focus on expanding in Qatar – Qatar International

Islamic Bank‟s (QIIK) CEO Abdulbasit A al-Shaibei said that the

bank has its eyes set on gaining a major share of the rapidly

expanding Qatari market and will expand both on the corporate

and retail businesses. Al-Shaibei said that many new projects

Overall Activity Buy %* Sell %* Net (QR)

Qatari 67.87% 67.62% 1,640,647.65

Non-Qatari 32.13% 32.39% (1,640,647.65)

3. Page 3 of 5

are in the pipeline and the bank expects to do more business,

keeping pace with Qatar‟s growth. He added that the bank has

planned to set up six new branches in Qatar in 2014, but

currently, there are no plans to enhance the bank‟s capital.

(Gulf-Times.com)

QE suspends trading in QISI, MCGS shares on March 12 –

The Qatar Exchange (QE) has suspended trading in the shares

of two companies on March 12, 2014 due to their AGMs being

scheduled on that day. The two companies are: Qatar Islamic

Insurance Company (QISI) and Medicare Group (MCGS). (QE)

QNNS’ AGM to be held on March 26 – The Qatar Navigation

Company‟s (QNNS) AGM is scheduled to be held on March 26,

2014 at the Great Room, W Hotel. In case of lack of quorum,

another meeting will be held on March 30, 2014 at the same

place. The AGM‟s agenda includes approving the board of

directors‟ recommendation of distributing 50% cash dividends

(QR5 per share) for 2013, among others. (QE)

HFC to sign meat import deal with Bulgaria – Qatar-based

Hassad Food Company (HFC) will be visiting Bulgaria next

month to sign a new meat import agreement and explore

possibilities of buying land for agriculture. Hassad Food is

planning to take this relationship to a higher level by investing in

Bulgaria‟s agriculture sector. (Qatar Tribune)

Al Wa'ab City to serve a community of 50,000 – Lebanon-

based Benchmark Company is constructing Al Wa'ab City, one

of the largest privately owned real estate projects in Qatar.

Bassim Halaby, Chairman & CEO of Benchmark said that Al

Wa'ab City will be a mix of 2,400 apartments and villas, which

will accommodate a total of 8,000 residents and serve a

community of 50,000 people. The 1.3mn square meter mega

project, which is being developed as a central district, is

expected to be completed by 2017. Further, Halaby said a

world-class mall will be operational at Al Wa'ab City by the end

of 2014 or early 2015. (Gulf-Times.com)

Qatalum posts world’s best power efficiency – Qatar

Aluminum Company (Qatalum) has recorded the best

rectiformer efficiency levels in the world. Rectiformers, which

convert AC power into DC power, play a vital role in the

aluminum smelting process. Qatalum‟s rectiformers have

recorded zero loss in terms of kilo amps per hour in more than

two years, an unprecedented achievement. (GulfBase.com)

International

US Fed set to drop threshold guidance under Yellen – Janet

Yellen's first policy-setting meeting as the chair person of the US

Federal Reserve will focus on how to fine tune the central bank's

promise in order to keep interest rates low without roiling

financial markets. Fed policymakers are expected to decide next

week to scrap their threshold of a 6.5% unemployment rate used

for considering a rate rise, and instead embrace new language

that is less specific about when tighter policy might come. The

threshold has been a staple of the central bank's „forward

guidance‟ since December 2012, when it was first adopted to

underscore a commitment to stimulate the US economy until it

was on surer footing. However, the US unemployment rate has

come down at a surprising speed, and now stands at 6.7%,

leaving Fed officials anxious to adopt a new guidance in line

with their view that the economy won't be ready for higher rates

for some time to come. (Reuters)

EU ministers hold line on bank failures as ECB sees risks –

European finance ministers made a few concessions to break a

deadlock on a bank-failure bill, since the European Central Bank

(ECB) warned that failure to enact it would hinder efforts to

combat fragmentation of the financial sector. At the end of talks

in Brussels, ministers identified six areas for possible

compromise in talks with the European Parliament on the Single

Resolution Mechanism legislation. However, details of new room

for maneuver were in short supply as meetings wrapped up, and

the consensus was that the parliament would need to cede

ground for a deal to get done. (Bloomberg)

ONS: UK manufacturing output grows more than forecast –

Factory production in the UK rose more than forecast in January

2014, adding to evidence for a broadening recovery. The Office

for National Statistics (ONS) said output rose 0.4% from

December, when it also gained at the same rate. The median of

25 estimates in a Bloomberg News survey was for 0.3% growth.

Industrial production, which includes utilities and mines, rose

0.1% – less than the 0.2% forecast – as bad weather hit oil &

gas output. Meanwhile, the Bank of England Governor Mark

Carney said a recovery is under way in the UK, though

investment and exports need to keep growing for it to be

sustained. Officials have pledged to hold the key interest rate at

a record low of 0.5% at least until unemployment falls to 7%

(now at 7.2%). (Bloomberg)

PBoC ready to cut bank reserves if growth falters –

According to sources, China's central bank is prepared to take

its strongest action since 2012 to loosen its monetary policy if

economic growth slows further, by cutting the amount of cash

that banks must keep as reserves. A cut would be triggered if

growth slips below 7.5% and toward 7.0%. Apart from

supporting a stumbling economy, the stronger action of cutting

bank reserves would provide a cushion against any shocks from

financial reforms that the People's Bank of China (PBoC) is

widely expected to push through this year, including a widening

of the Yuan's trading band to give the currency more room to

rise or fall each day and allowing banks more room to set

deposit rates. (Reuters)

Regional

Centrepoint to invest AED1bn in 100 stores – Landmark

Group‟s Centrepoint will invest AED1bn to set up 100 new

outlets and hire around 10,000 employees over the next five

years across the MENA region. Centrepoint‟s Director, Vinod

Talreja, said that the group will enter new markets in MENA

such as Iraq and Libya over the next few months. Centrepoint is

planning to open 20 stores in 2014 and 15 stores in 2015. In

2014, the company is set to open 7-9 new stores in the UAE and

hire 1,000 new employees. (GulfBase.com)

Saudi oil output inches up to 9.849mn bpd in February –

According to sources, Saudi Arabia produced 9.849mn bpd of

crude oil in February, up from 9.767mn bpd in January. The

Kingdom supplied 9.899mn bpd in February to the market, down

from 9.916mn bpd in January. However, market supply from the

OPEC heavyweight may differ from production depending on the

movement of barrels in and out of storage. (Reuters)

Saudi Aramco to produce gas for phosphate project, power

plant – According to sources, Saudi Aramco is planning to

produce 200mn cubic feet per day (cfd) of unconventional

natural gas by 2018 to supply to a new phosphate project and a

power plant. Out of this, 40mn cfd will be supplied to the

phosphate project that the Saudi Arabian Mining Co. is

developing at the Waad al Shamal Mining City, while 160mn cfd

will be supplied to the Saudi Electricity Company for a power

plant. Aramco is keen to increase gas output as it can fetch

$100 per barrel by exporting crude oil versus around $4 if it sells

it to a Saudi power plant. (GulfBase.com)

GHG plans two properties in Dubai – Gulf Hotels Group

(GHG) is expanding beyond the shores of Bahrain and plans to

4. Page 4 of 5

set up two five-star hotels in Dubai over the next few years.

GHG‟s Chairman Farouk Almoayyed said that BD50mn will be

invested in the development of the five-star hotel, Gulf Hotel

Business Bay. He said this waterfront property, located 1.5

kilometers from Burj Khalifa and Dubai Mall, is now in the design

stage and is expected to open mid-2017. The hotel will feature

230 rooms, three fine-dining restaurants, a variety of function

halls and meeting facilities. (Bloomberg)

DMCC, USSC sign deal to boost ties – Dubai Multi

Commodities Centre (DMCC) has signed a MoU with the United

States Chamber of Commerce (USCC) to promote trade

between the UAE and the US. The UAE is America‟s largest

export market in the Middle East, with over $22.5bn in exports in

2012. Around 1,000 US firms have presence in the UAE, of

which 294 are based in the DMCC Free Zone. (GulfBase.com)

Emirates REIT IPO to raise AED500mn on Nasdaq Dubai –

The UAE‟s first real estate investment trust, Emirates REIT has

planned to raise at least AED500mnthrough an IPO of its shares

on the Nasdaq Dubai bourse. The equity listing would be only

the second IPO on Dubai's two stock exchanges since 2009.

The company‟s Chairman, Abdulla al-Hamli said that the

company will use the proceeds for future acquisitions and

investment in existing assets. Emirates REIT was established in

2010 by the Dubai Islamic Bank and France-based Eiffel

Management for investing in real estate. Emirates REIT has

appointed Shuaa Capital and Emirates NBD as joint

bookrunners for the IPO. (Reuters)

DSI awards key supply contract to OSES – Drake & Scull

International (DSI) has awarded a key supply contract to Off-Site

Engineering Solutions (OSES), a Dubai-based specialist

provider of pre-engineered MEP solutions. The deal awarded by

DSI‟s Saudi unit is for supply of prefabricated multi service

modules to the Jabal Omar Development in Makkah. The scope

includes services in the main corridors to the four towers in the

development. The MEP modules will be delivered to site fully

finished and will be manufactured in OSES‟ Jeddah workshop.

(Bloomberg)

NBAD predicts 8-10% loan growth in 2014 – The National

Bank of Abu Dhabi‟s (NBAD) Chief Executive Alex Thursby said

that the bank expects 8-10% growth in its loans in 2014.

Thursby said the loan growth will be positive in 2014 since there

are many growth drivers such as current account, trade, foreign

exchange, etc. Last year, NBAD's net loans and advances rose

11.7% to AED183.8bn. Meanwhile, First Gulf Bank, the UAE's

second-largest lender, has also predicted 2014 loan growth to

be in low double digits. (Reuters)

NBAD plans second sale of Kangaroo bonds; declares 50%

dividends – The National Bank of Abu Dhabi (NBAD) is

planning to sell Kangaroo bonds, its second foray into the

Australian dollar-denominated debt market, as it diversifies its

investor base. ANZ Banking Group, Citigroup, HSBC Holdings

and NBAD are arranging the sale of five-year notes. According

to sources, NBAD is marketing the sale at about 130 basis

points more than swaps. NBAD is selling bonds in diverse

currencies right from the Mexican peso to Malaysia‟s ringgit in

order to tap wider investor pools. Meanwhile, NBAD‟s AGM has

approved the distribution of 40% cash dividend and 10% stock

dividend for the year ended December 31, 2013. (Bloomberg)

(GulfBase.com)

Eshraq’s BoD proposes 5% cash dividend, 10% bonus

shares – Eshraq Properties Company‟s board of directors has

proposed the distribution of 5% cash dividend and 10% bonus

shares to the shareholders for the year ended December 31,

2013. (ADX)

DDC, Starcare sign OMR7mn hospital deal – Duqm

Development Company (DDC) and Starcare Hospital have

signed an agreement to establish a multi-specialty, state-of-the-

art hospital at Duqm. The project‟s development cost is

estimated at around OMR7mn. Starcare is also setting up a 24-

hour multi-specialty medical center and pharmacy with the

support from DDC. While the hospital project will take two years

to be completed, the medical center is scheduled to open within

five months. The first phase of the hospital is a 30-35 bed

inpatient facility built at a cost of around OMR3.5-4mn, while in

the second phase, the hospital will have 75 beds at a cost of

around OMR7-8mn. (GulfBase.com)

DUTYF declares 55% cash dividend – Bahrain Duty Free

Shop Complex‟s (DUTYF) AGM has approved its board‟s

proposal to distribute 55% cash dividend, representing 55 fils

per share, of which 20 fils per share has already been

distributed as interim dividend. (Bahrain Bourse)

Bhotel declares 40% cash dividend – Gulf Hotels Group‟s

(Bhotel) AGM has approved its board‟s proposal to distribute

40% cash dividend (40 fils per share) for 2013. (Bahrain Bourse)

5. Contacts

Saugata Sarkar Ahmed M. Shehada Keith Whitney Sahbi Kasraoui

Head of Research Head of Trading Head of Sales Manager - HNWI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6535 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa ahmed.shehada@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

0.1%

(1.7%)

0.4%

0.0%

(0.2%)

(1.0%)

(1.4%)

(2.0%)

(1.6%)

(1.2%)

(0.8%)

(0.4%)

0.0%

0.4%

0.8%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,348.97 0.7 0.7 11.9 DJ Industrial 16,351.25 (0.4) (0.6) (1.4)

Silver/Ounce 20.85 0.1 (0.3) 7.1 S&P 500 1,867.63 (0.5) (0.6) 1.0

Crude Oil (Brent)/Barrel (FM

Future)

108.55 0.4 (0.4) (2.0) NASDAQ 100 4,307.19 (0.6) (0.7) 3.1

Natural Gas (Henry

Hub)/MMBtu

4.65 0.6 (2.5) 7.1 STOXX 600 331.49 0.0 (0.5) 1.0

North American Spot LPG

Propane Price

109.50 0.9 0.9 (13.4) DAX 9,307.79 0.5 (0.5) (2.6)

North American Spot LPG

Normal Butane Price

120.50 (0.4) (0.4) (11.2) FTSE 100 6,685.52 (0.1) (0.4) (0.9)

Euro 1.39 (0.1) (0.1) 0.9 CAC 40 4,349.72 (0.5) (0.4) 1.3

Yen 103.02 (0.2) (0.3) (2.2) Nikkei 15,224.11 0.7 (0.3) (6.6)

GBP 1.66 (0.2) (0.6) 0.4 MSCI EM 955.89 0.1 (1.1) (4.7)

CHF 1.14 (0.1) (0.0) 1.7 SHANGHAI SE Composite 2,001.16 0.1 (2.8) (5.4)

AUD 0.90 (0.5) (1.0) 0.7 HANG SENG 22,269.61 0.0 (1.7) (4.4)

USD Index 79.74 (0.0) 0.0 (0.4) BSE SENSEX 21,826.42 (0.5) (0.4) 3.1

RUB 36.52 0.5 0.2 11.1 Bovespa 45,697.62 0.4 (1.2) (11.3)

BRL 0.42 (0.5) (1.0) (0.0) RTS 1,132.05 (2.3) (2.3) (21.5)

165.4

145.5

132.7