Three mortgage scams

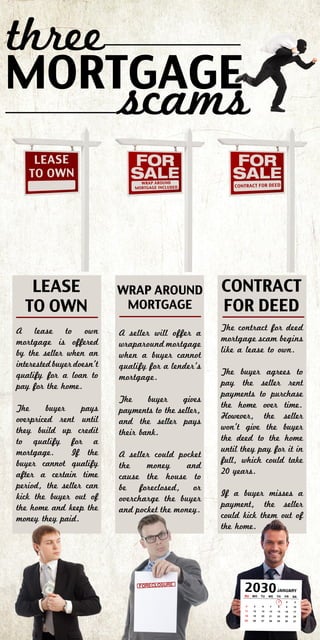

Buying a home has so many caveats and limitations that it may be hard to find a dream home. It’s especially hard for individuals who aren’t able to pay for a home in cash and don’t qualify for a mortgage loan from a lender. These individuals sometimes can get trapped in home mortgage scams where they lose money and their new home. Landmark outlines three possible mortgage scams and how to avoid them. click button for infographic scams three mortgage scams click button for infographic scams Lease to Own A lease to own mortgage is usually something offered by the seller when an interested buyer doesn’t qualify for a loan to pay for the home up front. Instead, the seller becomes a landlord for a time and charges rent to the homeowners, until they can build up their credit and qualify for a mortgage. Often times the seller charges “opt-in” money at the start of a lease to own agreement, which shows the buyers intent to purchase the home after qualifying. Many times a lease-to-own mortgage seems like a great deal.The buyer pays “rental” payments until they can buy the home outright. However, these rental payments are usually overpriced. Worse than that is when the contract states it’s time for the buyer to purchase the home outright, and they still cannot qualify for a home loan. The seller can then kick them out of the home and keep all of the rental payments and opt-in money. Many times a lease-to-own mortgage seems like a great deal. The buyer pays “rental” payments until they can buy the home outright. However, these rental payments are usually overpriced. Worse than that is when the contract states it’s time for the buyer to purchase the home outright, and they still cannot qualify for a home loan. The seller can then kick them out of the home and keep all of the rental payments and opt-in money.¬¬ If you don’t qualify for a mortgage, talk to your local Approved Housing Counseling Agencies. Some can find mortgages for low credit or low-income individuals. With this lower rate, homeowners can purchase home warranty insurance and save money by protecting their systems and appliances. Home warranty insurance could also be included in a home sale. Wraparound Mortgages For individuals who cannot qualify for a home loan, a scamming seller will provide a mortgage instead of a traditional lender. This “mortgage” wraps around the mortgage the seller has on the home already. When the buyer pays money to the seller, the seller pays it on their mortgage to the bank. Some sellers in this situation scam the buyer. If the seller doesn’t make payments to the bank, the home will be foreclosed and the buyer is kicked out. Or, if the seller wants to make money, they’ll charge more from the buyer on the mortgage payment, pay their minimum to the bank, and pocket the rest. The best way to combat this mortgage scam is to make sure there is a written contract between the seller and the buyer of t

Recommended

More Related Content

Viewers also liked

Similar to Three mortgage scams

Similar to Three mortgage scams (20)

More from Whitney Bennett

More from Whitney Bennett (20)

Recently uploaded

Recently uploaded (20)

Three mortgage scams

- 1. WRAP AROUND MORTGAGE LEASE TO OWN CONTRACT FOR DEED A lease to own mortgage is offered by the seller when an interested buyer doesn’t qualify for a loan to pay for the home. The buyer pays overpriced rent until they build up credit to qualify for a mortgage. If the buyer cannot qualify after a certain time period, the seller can kick the buyer out of the home and keep the money they paid. A seller will offer a wraparound mortgage when a buyer cannot qualify for a lender’s mortgage. The buyer gives payments to the seller, and the seller pays their bank. A seller could pocket the money and cause the house to be foreclosed, or overcharge the buyer and pocket the money. The contract for deed mortgage scam begins like a lease to own. The buyer agrees to pay the seller rent payments to purchase the home over time. However, the seller won’t give the buyer the deed to the home until they pay for it in full, which could take 20 years. If a buyer misses a payment, the seller could kick them out of the home.