Telegram. One step toward $1B opportunity.

•

0 likes•921 views

Telegram messaging app + messaging apps universe

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (12)

Similar to Telegram. One step toward $1B opportunity.

Similar to Telegram. One step toward $1B opportunity. (20)

Recently uploaded

Recently uploaded (20)

Telegram. One step toward $1B opportunity.

- 1. TELEGRAM ONE STEP TOWARD $1B OPPORTUNITY Despite questions re intellectual property rights and tension between Telegram’s founder Pavel Durov and Vkontakte investors’ UCP/mail.ru, messaging is interesting theme for VCs and Telegram is one of the top10 and the fastest growing app. Messaging Mobile instant messaging is the new social networking. Social graph, network effect and threat to social networks are the major points why this model will succeed. The scaling model is ultra efficient. Accessing the address book, messengers leverage the graph that is already available in phones, what made them the fastest scaling platforms’ ever. Graph are built behind social networks’ territory, which made a threat to i.e. Facebook’s 90x P/E multiply supposed that there would be no competitors absorbing users’ communication. Messengers steal telecoms’ business share by disrupting $120B SMS market. WhatsApp traffic would cost operators $30B in SMS fees in 2013, projecting to reach $55B by 2016. With 50B of messages sent by WhatsApp per day, the annual ones delivered are two times more than the global SMS traffic (18T vs 8T respectively, taking into account that SMS feature is available on 7B phones, while messaging one at 1-2B smartphones only). SMS is a great business with substantial margin and messaging is its risky next gen variation with 10-100x return (Sequoia made 50x by investing in WhatsApp). Messengers boast the majority of user engagement. Only WhatsApp is accounted for 70% of it on a daily basis (vs 60% for Facebook). WhatsApp users share 0.5B photos/day (certainly more than Facebook). It’s among Top10 app in 100 countries. Network effect. When new user join the app his whole address book with 300-500 connections are added in a second. Messengers become the primary communication channel that drive word of mouth marketing and increase switching cost. Sector is hot for M&A. WhatsApp was acquired for $19B, Viber for $900m and Snapchat got an $3- 4B offer from Google. In terms of price per user WhatsApp user costs $34-42 and are about what Google paid when acquiring YouTube.

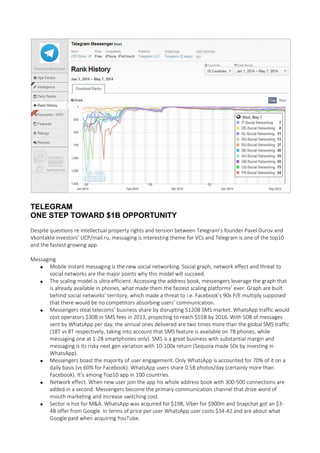

- 2. While its winner take all business, the local specifics matter (as there are Vkontakte vs Facebook, Yandex vs Google, Ozon vs Amazon). After WhatsApp acquisition by Facebook, Telegram growth even accelerated. Pavel is ambitious, eccentric and product focused entrepreneur, who attract users slightly faster than investors. Telegram Telegram is the youngest messaging among Top10 by MAU. It scales ultra-fast, from 0.1m MAU in late 2013 to 35m in May 2014. It’s more popular than MoiMir, Russian parts of Facebook and Twitter. While Top3 players are 5-15x larger, Telegram has 2.5m more users than SnapChat, which rejected $3-4B offer by Google. When all messengers offer the same features, user acquisition is the core competency. There are 7B ppl on the Earth, 6.8B cell phones, 1-2B smartphones and 1B messaging users. The stakes are high. Mobile cellular is the fastest growing communication ever. The idea is that mobile Internet will widespread even faster and messengers will be the main apps that absorb the majority of primary communication. Twitter (ru), 11 Facebook (ru), 30 MoiMir, 30 TELEGRAM, 35 Odnoklassniki, 42 Vkontakte, 52 Comparison of Russian social/messaging networks MAU mm

- 3. Leveraging know-how in running social network Pavel advanced in product and user focused approach. How to approach Telegram? While Pavel have excessive capital, VC may bring legal, financial and investment competencies. Legal issues are on today’s agenda. Pavel might be interested in reliable partner that recognize IP rights clarity after due dill, show investment attractiveness for other financial and strategic investors, fix the initial valuation at high level and move forward with bus dev/smart money as usual Most probably it might be done by acquiring small/minority stake only, that is comfortable for Pavel and not a big money for VC fund High valuation, no need in capital, tension in dealing with historical investors and tight competition for messaging space are the risks