Recommended

More Related Content

What's hot

What's hot (13)

Viewers also liked

Viewers also liked (20)

Similar to 1.5 bundles services

Similar to 1.5 bundles services (20)

Recently uploaded

Recently uploaded (20)

1.5 bundles services

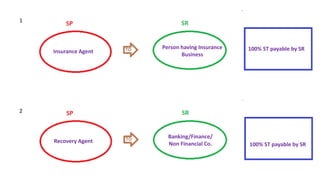

- 1. Insurance Agent Person having Insurance Business 100% ST payable by SR Recovery Agent Banking/Finance/ Non Financial Co. 1 2 100% ST payable by SR

- 2. Selling/ Marketing Agent Lottery distributor or Selling Agent of State Govt. 100% ST payable by SR Director Company or Body Corporate 3 4 100% ST payable by SR

- 3. Govt. or Local Authority Any Business Entity 100% ST payable by SR Sponsoree Sponsoror 5 6 100% ST payable by SR Any Service except a. Renting of Immovable Property b. Item No. 1 (i), 1(ii), 1(iii) of –ve List Body Corporate + TT

- 4. Any Person in NTT Any Person in TT 100% ST payable by SR Arbitral tribunal or Firm of Advocates or Individual Advocates Any business entity in TT 7 8 100% ST payable by SR Not Senior Advocates Legal Services

- 5. GTA Factory, Society, Co- Operative society, Dealer Body Corporate Firm Must be Registered 100% ST payable by SR Transportation of Goods by Road 9 Exception: If SR is in NTT then SP need to Pay ST

- 6. Aggregator Service Receiver 100% ST payable by Aggregator 10