This document outlines creditable withholding tax rates that apply to various types of income payments in the Philippines. It provides withholding tax rates for professional fees, talent fees, rentals, contractors, income distributions, partnership income, real estate sales, additional government personnel income, credit card payments, supplier payments, interest income, and REIT income. It also lists some exemptions from creditable withholding tax, such as socialized housing projects, certain non-profit corporations, joint construction ventures, and low-income individuals. The withholding tax rates range from 1% to 15% depending on the type of income and amount.

Antisemitism Awareness Act: pénaliser la critique de l'Etat d'Israël

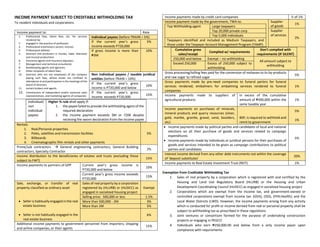

INCOME PAYMENT SUBJECT TO CREDITABLE WITHHOLDING TAX.docx

1. INCOME PAYMENT SUBJECT TO CREDITABLE WITHHOLDING TAX

To resident individuals and corporations

Income payment to: Rate

1. Professional fees, talent fees, etc. for services

rendered by:

2. engaged in the practice of profession

3. Professional entertainers (actors, emcees

4. Professional athletes

5. directors and producers in movies, radio, television

and musical productions

6. Insurance agents and insurance adjusters

7. Management and technical consultants;

8. Bookkeeping agents and agencies;

9. Other recipients of talent fees;

10. directors who are not employees of the company

paying such fees, whose duties are confined to

attendance at and participation in the meetings of the

board of directors

11. certain brokers and agents

12. Commissions of independent and/or exclusive sales

representatives, and marketing agents of companies

Individual payees (before TRAIIN = 5%)

If the current year’s gross

income exceeds P720,000

5%

If gross income is more than

₱3M

10%

Non individual payees / taxable juridical

entities (before TRAIN = 10%)

If the current year’s gross

income is P720,000 and below

10%

If the current year’s gross

income exceeds P720,000

15%

Individual/

non

individual

payees

Higher % rule shall apply if:

1. the payee failed to provide the withholding agent of the

required declaration

2. the income payment exceeds 3M or 720K despite

receiving the sworn declaration from the income payee

Rentals

1. Real/Personal properties

2. Poles, satellites and transmission facilities

3. Billboards

4. Cinematographic film rentals and other payments

5%

Prime/sub contractors General engineering contractors, General Building

contractors, Specialty Contractor

2%

Income distribution to the beneficiaries of estates and trusts (excluding those

subject to FWT)

15%

Income payments to partners of GPP Current year’s gross income is

P720,000 and below

10%

Current year’s gross income exceeds

P720,000

15%

Sale, exchange, or transfer of real

property classified as ordinary asset

Seller is habitually engaged in the real

estate business

Seller is not habitually engaged in the

real estate business

Sales of real property by a corporation

registered by (HLURB) or (HUDCC) as

engaged in socialized housing project

Exempt

Selling price: 500,000 or less 1.5%

More than 500,000 - 2M 3%

More than 2M 5%

6%

Additional income payments to government personnel from importers, shipping

and airline companies, or their agents

15%

Income payments made by credit card companies ½ of 1%

Income payment made by the government, TWA to:

Top Withholding agent Large taxpayers

Top 20,000 private corp

Top 5,000 individuals

Taxpayers identified and included as Medium Taxpayers, and

those under the Taxpayer Account Management Program (TAMP).

Supplier

of goods

1%

Supplier

of services

2%

Cumulative gross

sales/receipt

Complied w/ requirements

Don’t complied with

requirements (IF SILENT)

250,000 and below Exempt – no withholding

All amount subject to

withholding

Exceed 250,000 Excess of 250,000 subject to

withholding

Gross processing/tolling fees paid for the conversion of molasses to its by-products

and raw sugar to refined sugar

5%

Gross payments made by pre-need companies to funeral parlors for funeral

services rendered; embalmers for embalming services rendered to funeral

companies

1%

Income payments made to suppliers of

agricultural products

in excess of the cumulative

amount of ₱300,000 within the

same taxable year

1%

Income payments on purchases of minerals,

mineral products and quarry resources (silver,

gold, marble, granite, gravel, sand, boulders,

etc)

BSP, is required to withhold and

remit to government

5%

1%

Income payments made by political parties and candidates of local and national

elections on all their purchase of goods and services related to campaign

expenditures

Income payments made by individuals or juridical persons for their purchases of

goods and services intended to be given as campaign contributions to political

parties and candidates

5%

Interest income derived from any other debt instruments not within the coverage

of ‘deposit substitutes’

20%

Income payments to Real Estate Investment Trust (REIT) 1%

Exemption from Creditable Withholding Tax

1. Sales of real property by a corporation which is registered with and certified by the

Housing and Land Use Regulatory Board (HLURB) or the Housing and Urban

Development Coordinating Council (HUDCC) as engaged in socialized housing project

2. Corporations which are exempt from the income tax, and government-owned or

controlled corporations exempt from income tax: (GSIS), (SSS), (PHILHealth); and the

Local Water Districts (LWD). However, the income payments arising from any activity

which is conducted for profit or income derived from real or personal property shall be

subject to withholding tax as prescribed in these regulations

3. Joint ventures or consortium formed for the purpose of undertaking construction

projects or engaging in PEGCO

4. Individuals who earn ₱250,000.00 and below from a only income payor upon

compliance with requirements