This document discusses the taxable territory and service tax provisions under Indian law. It specifies that the whole of India except Jammu and Kashmir constitutes the taxable territory, which includes territorial waters, continental shelf, exclusive economic zone, and airspace up to 12 nautical miles. It also states that service tax shall be levied at 15% on the value of services provided or agreed to be provided in the taxable territory by one person to another, excluding services specified in the negative list, and shall be collected in the prescribed manner.

6th sem cpc notes for 6th semester students samjhe. Padhlo bhai

India taxable territory and GST rates

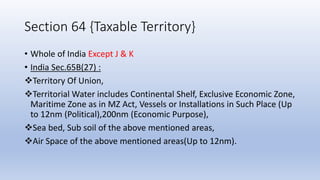

1. Section 64 {Taxable Territory}

• Whole of India Except J & K

• India Sec.65B(27) :

Territory Of Union,

Territorial Water includes Continental Shelf, Exclusive Economic Zone,

Maritime Zone as in MZ Act, Vessels or Installations in Such Place (Up

to 12nm (Political),200nm (Economic Purpose),

Sea bed, Sub soil of the above mentioned areas,

Air Space of the above mentioned areas(Up to 12nm).

2. Section 66B

ST shall be Levied

•@ 15%

On

•Value{Sec.67} of Services{Sec.65B(44)}

Other than those

Specified in

•-Ve list{Sec.66D}

ST- 14% (Creditable)

SBC- 0.5% (Non Creditable)

KKC- 0.5% (Creditable)

3. Section 66B

Provided/ Agreed

to be Provided in

•Taxable Territory

By

•One Person{Sec.65B(37)} to Another Person

Collected in the

•Manner Prescribed{Procedural Aspects}