GE Aviation Engine Industry Leader

•Download as PPSX, PDF•

0 likes•542 views

Tushar has created company profile on GE Aviation covering key information, industry insights (trends and drivers) and competitors etc.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to GE Aviation Engine Industry Leader

Similar to GE Aviation Engine Industry Leader (20)

Recently uploaded

Recently uploaded (20)

GE Aviation Engine Industry Leader

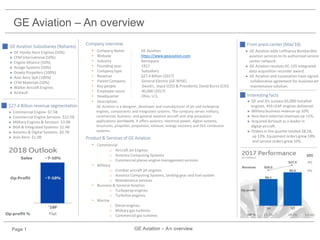

- 1. GE Aviation – An overview ► GE and JVs surpass 65,000 installed engines, 459 LEAP engines delivered. ► Military business revenue up 10%. ► Avio Aero external revenues up 11%. ► Acquired AirVault as a leader in digital aircraft. ► Orders in the quarter totaled $8.1B, up 13%. Equipment orders grew 18% and service orders grew 10%. Interesting facts4 Company overview • Company Name GE Aviation • Website https://www.geaviation.com • Industry Aerospace • Founding year 1917 • Company type Subsidiary • Revenue $27.4 Billion (2017) • Parent Company General Electric (GE-NYSE) • Key people David L. Joyce (CEO & President); David Burns (CIO) • Employee count 40,000 (2017) • Headquarter Ohio, U.S. • Description: GE Aviation is a designer, developer and manufacturer of jet and turboprop engines, components and integrated systems. The company serves military, commercial, business and general aviation aircraft and ship propulsion applications worldwide. It offers avionics, electrical power, digital systems, structures, propeller, propulsion, exhaust, energy recovery and DLE combustor systems. GE Aviation – An overviewPage 1 Product & Services of GE Aviation • Commercial o Aircraft Jet Engines o Avionics Computing Systems o Commercial planes engine management services • Military o Combat aircraft jet engines o Avionics Computing Systems, landing gear and fuel system o Maintenance services • Business & General Aviation o Turboprop engines o Turbofan engines • Marine o Diesel engines o Military gas turbines o Commercial gas turbines ► GE Aviation adds Lufthansa Bombardier aviation services to its authorized service center network. ► GE Aviation receives KC-135 Integrated data acquisition recorder award. ► GE Aviation and Luxaviation have signed collaborative agreement for business jet maintenance solution. From press center (May’18)3 ► GE Honda Aero Engines (50%) ► CFM International (50%) ► Engine Alliance (50%) ► Aviage Systems (50%) ► Dowty Propellers (100%) ► Avio Aero SpA (100%) ► CFM Materials (50%) ► Walter Aircraft Engines ► AirVault 1 GE Aviation Subsidiaries (%shares) ► Commercial Engine- $7.5B ► Commercial Engine Services- $12.5B ► Military Engines & Services- $3.9B ► BGA & Integrated Systems- $1.4B ► Avionics & Digital Systems- $0.7B ► Avio Aero- $1.0B $27.4 Billion revenue segmentation2

- 2. GE Electric’s Revenue Segmentation (Parent company of GE Aviation) Page 2 • The revenue segmentation of GE Electric (Figure1) states that $27.38 Billion revenue is contributed by GE Aviation division. • GE Aviation is the second largest contributor in General Electric revenue after GE Power division with $35.99 Billion number. • GE Lighting is contributing lowest revenue in General Electric portfolio. GE Aviation – An overview Figure 1 Key competitors of GE Aviation 1. Rolls-Royce Rolls-Royce is seen as one of GE Aviation's biggest rivals. Rolls-Royce is headquartered in London, England, and was founded in 1906. Rolls-Royce generates 11,303% the revenue of GE Aviation. 2. United Technologies United Technologies was founded in 1934, and its headquarters is in Hartford, Connecticut. United Technologies operates in the Aerospace industry. United Technologies has 204,510 more employees than GE Aviation. 3. Honeywell Honeywell is one of GE Aviation's top rivals. Honeywell is a Public company that was founded in Morris Plains, New Jersey in 1906. Honeywell competes in the Electronic Equipment industry. Honeywell has 130,510 more employees vs. GE Aviation.

- 3. SWOT Analysis- GE Aviation Page 3 GE Aviation – An overview Figure 1 GE Aviation • Global recognition: The name of GE and recognition given the conglomerate globally is a huge. • GE Aviation is into manufacturing of commercial as well as military airplanes engines including technical services. • Extensive R&D capabilities with a strong workforce. • Preference of GE engine for next generation aircrafts by leading OEMs, like Boeing and Airbus. • Coming with narrow body engines. Weakness • Legal proceedings against GE Aviation from competitors for patent rights etc. • Dependence for raw material supply from multiple third parties. • Weak performance in Asian markets. • Delay in delivery of engines to Aircraft manufacturers. Strengths • Growing Demand in the airline business. • Leading Aviation OEMs are now looking 5th generation engine manufacturer as the motor supplier for their crafts. • Increased prices of crude oil demands more fuel efficient and lighter engines. GE R&D is strongly focus on to get more efficient engines in terms of power with low in weight technology. • GE Aviation strong relationship with service center in various countries. Opportunity • Variety of engines manufactured by competitors (Rolls- Royce engines are in service with more than 30 types of commercial aircraft worldwide). • Defense budgetary cuts in various countries. • Entry of various European companies in Aviation Industry. • Long term agreements of GE Aviation competitors with OEMs. Threats

- 4. Aircraft Engines Market Overview Page 4 GE Aviation – An overview Key facts • The aircraft engines market is projected to grow from an estimated USD 68.05 Billion in 2017 to USD 92.38 Billion by 2022, at a CAGR of 5.23%. Factors such as increase in aircraft deliveries and rising demand for fuel-efficient aircraft engines are expected to drive the aircraft engines market. • Turbofan type engine segment projected to witness the highest growth during the 2017 to 2022. • Commercial application segment projected to witness the highest growth among Military Aviation, General Aviation Engines segments. • The Asia-Pacific region is one of the fastest-growing markets for aircraft engines. This growth is attributed to the increase in manufacturing of commercial aircraft in countries such as China and Japan. • The international aircraft engines market is prophesied to see a segmentation into North America and other major regions such as Asia Pacific Excluding Japan (APEJ) and Europe. Amongst these, North America could take the driver’s seat in the market while clutching a top revenue growth. • Asia Pacific Excluding Japan, is predicted to expand at a faster pace and gain between 2017 and 2022. Key Industry Drivers • Consistently growing demand for air-transport. • Up-gradation of the existing technology to make the engines more fuel efficient and powerful engines. • Strategic partnerships and alliance of aircraft engine manufacturers with leading aircraft manufacturing companies to provide aircraft engines. • Increase of Aircraft demand in emerging market increase the engine OEMs to deliver motor to Aircraft manufacturers. • Tapping into cargo is a major reason for OEMs to manufacture the engines. • Increase in aircraft deliveries and rising demand for fuel-efficient aircraft engines are expected to drive the aircraft engines market. • Engine manufacturers are replacing the age-old engines with new-generation engines. Changing of engines require changing its engine start system. Such replacement programs will increase the consumption of engine start systems and drive the market growth • Advanced processes such as 3D printing along with materials like ceramic matrix composites are being used to develop the engines and components of new-generation aircraft. This low cost manufacturing way attract new entrants in this market.

- 5. Global Commercial Aviation Overview Page 5 • Commercial Aviation Revenue Per Kilometer (RPKs) is projected to be grow by GE Aviation to 6.4 (in ‘20F) from 6.0 (in ’18F). • Commercial departures is projected to be increase to 41.2M (in ‘20F) than 38.6M (in ’18F). • Fuel charges going to be decrease $0.7/Barrel which is the positive sign for the Global Commercial Airline Industry and dependent industries. • As per the geographic segmentation Revenue Per Kilometer (billions) is highest in Latin America and Africa (8.0% each) followed by Asia Pacific and Middle east (7.0% each). GE Aviation – An overview

- 6. Global Commercial Engine Utilization Page 6 • GE Aviation has major stake in commercial departures. • The above data of GE includes GE Aviation and Joint venture engines. • High utilization of GE Aviation engines. GE Aviation – An overview • GE Aviation 60% cfm56-5b engine has not come back with any compliant. This states the durability and reliability of its engines. • 4,800 cfm56-5b engine has been delivered and 5,500 to be delivered till 2020 at forecasted CAGR of 5%. • 2017 GE comm’l installed base 12,121; JV comm’l installed base 22,898. • 2020F GE comm’l installed base 11,749; JV comm’l installed base 27,394. • 2025F GE comm’l installed base 11,879; JV comm’l installed base 34,932.

- 7. Global Military Engines Portfolio Page 7 GE Aviation – An overview • GE and Joint Ventures has installed around 24,200 engines in Military Aircrafts or Vessels. (Figure 1) • GE and JV is the highest among all the competitors (Figure 1) in Industry followed by Rolls-Royces with 16,200 number. • Sales growth of GE Aviation (Figure2,marked in blue) represents the Engine Services number from 2015 ($3.7) to 2025 ($8.7). Figure 1 Figure 2

- 8. GE Aviation – An overview Page 8 Data source: • https://en.wikipedia.org/wiki/GE_Aviation • https://www.ge.com/investor-relations/sites/default/files/GE%20Aviation%20031418.pdf • https://www.geaviation.com/ • https://www.statista.com/statistics/245430/revenue-of-general-electric-by-segment/ • http://www.fi-aeroweb.com/firms/Competitors/Competitors-General-Electric.html • https://www.prnewswire.com/news-releases/aircraft-engines-market---global-industry-analysis-size-share-growth- trends-and-forecast-2017---2022-300559793.html • https://www.marketsandmarkets.com/PressReleases/aircraft-engine.asp • https://www.transparencymarketresearch.com/aircraft-engine-market.html • http://www.iata.org/ • https://www.morningstar.com/news/business-wire/BWIPREM_20180404006047/global-commercial-aircraft-engine- start-system-market-trends-drivers-and-challenges-technavio.html • https://www.ge.com/investor-relations/ar2017/ceo-letter GE Aviation – An overview