Raquel Thompson: Combining Creativity with Practicality in Architecture

Single Tenant Net Lease Research Report

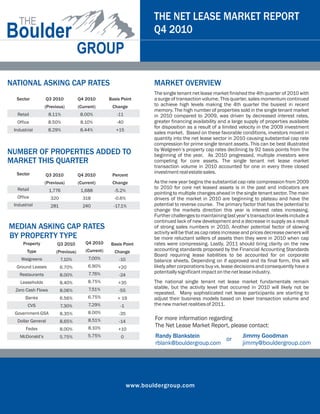

1. THE NET LEASE MARKET REPORT

Q4 2010

NATIONAL ASKING CAP RATES MARKET OVERVIEW

The single tenant net lease market finished the 4th quarter of 2010 with

Sector Q3 2010 Q4 2010 Basis Point a surge of transaction volume. This quarter, sales momentum continued

(Previous) (Current) Change to achieve high levels making the 4th quarter the busiest in recent

memory. The high number of properties sold in the single tenant market

Retail 8.11% 8.00% -11 in 2010 compared to 2009, was driven by decreased interest rates,

Office 8.50% 8.10% -40 greater financing availability and a large supply of properties available

for disposition as a result of a limited velocity in the 2009 investment

Industrial 8.29% 8.44% +15

sales market. Based on these favorable conditions, investors moved in

quantity into the net lease sector in 2010 causing substantial cap rate

compression for prime single tenant assets. This can be best illustrated

by Walgreen’s property cap rates declining by 92 basis points from the

NUMBER OF PROPERTIES ADDED TO beginning of the year. As 2010 progressed, multiple investors were

MARKET THIS QUARTER competing for core assets. The single tenant net lease market

transaction volume in 2010 accounted for one in every three closed

Sector investment real estate sales.

Q3 2010 Q4 2010 Percent

(Previous) (Current) Change As the new year begins the substantial cap rate compression from 2009

Retail to 2010 for core net leased assets is in the past and indicators are

1,776 1,688 -5.2%

pointing to multiple changes ahead in the single tenant sector. The main

Office 320 318 -0.6% drivers of the market in 2010 are beginning to plateau and have the

Industrial 281 240 -17.1% potential to reverse course. The primary factor that has the potential to

change the markets direction this year is interest rates increasing.

Further challenges to maintaining last year’s transaction levels include a

continued lack of new development and a decrease in supply as a result

MEDIAN ASKING CAP RATES of strong sales numbers in 2010. Another potential factor of slowing

activity will be that as cap rates increase and prices decrease owners will

BY PROPERTY TYPE be more reluctant sellers of assets then they were in 2010 when cap

Property Q3 2010 Q4 2010 Basis Point rates were compressing. Lastly, 2011 should bring clarity on the new

Type (Previous) (Current) Change accounting standards proposed by the Financial Accounting Standards

Board requiring lease liabilities to be accounted for on corporate

Walgreens 7.10% 7.00% -10 balance sheets. Depending on if approved and its final form, this will

Ground Leases 6.70% 6.90% +20 likely alter corporations buy vs. lease decisions and consequently have a

Restaurants 7.76% potentially significant impact on the net lease industry.

8.00% -24

Leaseholds 8.40% 8.75% +35 The national single tenant net lease market fundamentals remain

7.51% stable, but the activity level that occurred in 2010 will likely not be

Zero Cash Flows 8.06% -55

repeated. Many sophisticated net lease participants are starting to

Banks 6.56% 6.75% + 19 adjust their business models based on lower transaction volume and

CVS 7.30% 7.29% -1 the new market realities of 2011.

Government-GSA 8.35% 8.00% -35

Dollar General 8.65% 8.51% -14

For more information regarding

Fedex 8.10% The Net Lease Market Report, please contact:

8.00% +10

McDonald’s 5.75% 5.75% 0 Randy Blankstein Jimmy Goodman

or

rblank@bouldergroup.com jimmy@bouldergroup.com

www.bouldergroup.com