1. CHAPTER 4

FRAUD & ERROR

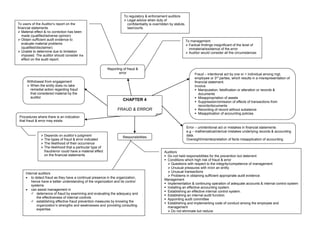

Fraud – intentional act by one or > individual among mgt,

employee or 3rd

parties, which results in a misrepresentation of

financial statement.

Involve

Manipulation, falsification or alteration or records &

documents

Misappropriation of assets

Suppression/omission of effects of transactions from

records/documents

Recording of record without substance

Misapplication of accounting policies

Error – unintentional act or mistakes in financial statements

e.g – mathematical/clerical mistakes underlying records & accounting

data.

Oversight/misinterpretation of facts misapplication of accounting

policies

Withdrawal from engagement

When the entity does no take

remedial action regarding fraud

that considered material by the

auditor

Procedures where there is an indication

that fraud & error may exists

Responsibilities

Reporting of fraud &

error

Auditors

Do not held responsibilities for the prevention but deterrent

Conditions which high risk of fraud & error

Questions with respect to the integrity/competence of management

Unusual pressures with in/on an entity

Unusual transactions

Problems in obtaining sufficient appropriate audit evidence

Management

Implementation & continuing operation of adequate accounts & internal control system

Installing an effective accounting system.

Establishing an effective internal control system.

Establishing an internal audit function.

Appointing audit committee

Establishing and implementing code of conduct among the employee and

management

Do not eliminate but reduce

Depends on auditor’s judgment

The types of fraud & error indicated

The likelihood of their occurrence

The likelihood that a particular type of

fraud/error could have a material effect

on the financial statements

To management

Factual findings insignificant of the level of

immaterial/existence of the error

Auditor would consider all the circumstances

To users of the Auditor’s report on the

financial statements

Material effect & no correction has been

made (qualified/adverse opinion)

Obtain sufficient audit evidence to

evaluate material problems

(qualified/disclaimer)

Unable to determine due to limitation

imposed. The auditor should consider the

effect on the audit report.

To regulatory & enforcement auditors

Legal advice when duty of

confidentiality is overridden by statute,

law/courts.

Internal auditors

to detect fraud as they have a continual presence in the organization,

hence have a better understanding of the organization and its control

systems.

can assist management in

deterrence of fraud by examining and evaluating the adequacy and

the effectiveness of internal controls

establishing effective fraud prevention measures by knowing the

organization’s strengths and weaknesses and providing consulting

expertise.