2. are not congruent, activities in the shadow economy often imply the evasion of direct or

indirect taxes, so that the factors affecting tax evasion will most certainly also affect the

shadow economy. The main issue that arises and afflicts the research community is the

fact that measuring the black economy is extremely difficult by its nature, as it requires

assessment of the economic activity which derives from informal transactions. Usually,

surveys underestimate the size of the shadow economy, but econometric techniques are

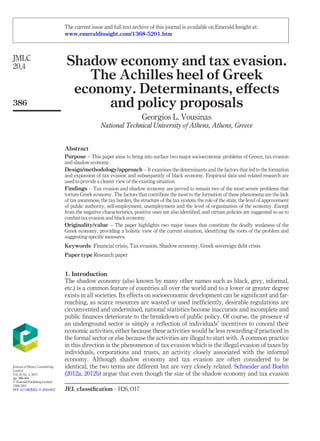

nowadays used for better understanding of its size. The following figure depicts the size

of the shadow economy in selected Organization for Economic Co-operation and

Development (OECD) countries (including the seven major advanced economies as

reported by the International Monetary Fund, the so-called Group of 7 or G7) as a

percentage of gross domestic product (GDP), so as to emphasize the size of the problem

(Figure 1).

As it is made clear from the above figure, the black economy is a reality for all the

countries, but the problem focuses on the so-called PIGS, a term that refers to the

economies of Portugal, Italy, Greece and Spain, which were unable to refinance their

government debt or to bail out over-indebted banks on their own during the recent global

debt crisis. Among them, Greece holds the supremacy with the level of its underground

economy in 2015 reaching the impressive 22.4 per cent of GDP, i.e. almost one quarter of

the Greek economic activity. Italy follows closely with 20.1 per cent, while the Spanish

black economy is 18.2 per cent and the Portuguese one 17.6 per cent. An interesting fact is

that the biggest European economy, Germany, is at the level of 12.2 per cent which is

identical with the average of the selected OECD countries shown on the graph. Even

more, the US economy, the largest in the world, has managed to restrict its shadow

economy to 5.9 per cent, which is the smallest one among all and constitutes one quarter

of the Greek one (the biggest one). In less developed countries, the informal economy is

usually 25 to 40 per cent of national income and represents up to 70 per cent of non-

agricultural employment. In these countries, the informal activity often occurs because of

the inadequacies of legal systems to document and formalize the company registration.

The main driving forces of the shadow economy are tax and social security burdens, the

Figure 1.

Level of the shadow

economy in OECD

countries as of 2015

(percentage of GDP)

Shadow

economy and

tax evasion

387

3. moral attitude to taxation, the quality of state institutions and labor market regulation.

Reducing the tax burden is therefore likely to lead to a reduction in the black economy,

especially if it is combined with lower tax rates, less shadow work and the potential for

lower prices. Of course, a vicious circle in the other direction can also be created. The

number of participants in the shadow economy globally is very large with some sectors

such as the constructing, having almost half of their staff working informally.

The shadow economy is pervasive and is composed of a vast number of small and

scattered transactions. The policy response should be very careful concerning the

mechanisms and the effort to eliminate the informal economy, particularly in terms of

development and promotion of entrepreneurship and business related to illegal employment.

There are also huge potential benefits from the possibility of formalizing the self-employed

in small businesses.

2. Literature review

At this point and before we proceed with the analysis of the origins and the determinants as

well as the effects of black economy and tax evasion on the Greek economy, a review of both

theoretical and empirical literature on these crucial issues is undertaken so as to highlight

the current research results.

Bitzenis et al. (2016) explore the determinants of the Greek shadow economy and its

interaction with the official economy by undertaking an interdisciplinary review of

economic and political studies on the size and determinants of the shadow economy, tax

evasion and undeclared work in Greece to reveal the extent and complexity of these

phenomena. They estimate the size and determinants of the shadow economy via the

multiple-indicators-multiple-causes (MIMIC) approach and their findings indicate that the

important determinants are factors related to macroeconomic conditions, such as

unemployment and GDP growth, as well as institutional factors, such as tax morale and the

rule of law. The overall conclusion is that an adoption of a policy based on these findings

would lead to a successful transfer of part of the shadow economy to the official economy

thus, boosting government revenues and eventually leading the Greek economy out of the

depression that emerged as a result of the sovereign debt crisis.

Artavanis et al. (2015) used a novel approach to estimate tax evasion using the

adaptation of the private sector to the norms of semiformality based on the bank’s

perception of the individual’s true income. They used bank data on household credit and

replicated the bank model of credit capacity decision to infer the banks estimate of

individuals’ true income. The authors estimate a lower bound of 28.2bn euros of unreported

income for Greece, which accounts for 32 per cent of the deficit for 2009. Primary tax-

evading industries are found to be medicine, law, education, engineering and media. They

also provide evidence that tax evasion persists not because the tax authorities are unaware,

but because of a lack of paper trail and political willpower.

Berger et al. (2014) present new estimates of the Greek underground economy and

explore the link between the shadow economy and aggregate debt. They show that the

Greek underground economy has been underestimated heavily and has been on a rising

trend again, as Greece adopted the euro and also show evidence that the size of the

underground economy is positively related to the debt-to-GDP ratio. Their results suggest

that for a sample of eleven EMU member countries the loss of the inflation tax as an

economic policy instrument had drastic consequences. While the underground economy did

not have a statistically significant impact on aggregate debt before the introduction of the

euro, it has pushed up the debt-to-GDP ratio in the sample ever since.

JMLC

20,4

388

4. Remeikiene et al. (2014) point out that, in general sense, shadow economy emerges in

such spheres as taxation, social security and labor aspects of undeclared work. The aim of

their article is to identify what country-level determinants from these spheres have the

strongest impact on the scope of shadow economy in Greece during 2005-2013. The results

show that the country-level determinants that influence mostly the scope of shadow

economy in Greece are the unemployment rate, GDP per capita, total labor force, domestic

credit to private, tax rate and tax payment. Calculations confirmed the results of the

theoretical research by showing that tax rate is the determinant having the most significant

impact on shadow economy emergence and development. The authors of the article also

recommend carrying out a detailed analysis of the components of current tax structure in

business and other spheres so as to lead to the introduction of proper taxes which would not

appear to be the fundamental motive to act in a shadow.

Kaplanoglou and Rapanos (2013) highlight a number of shortcomings in the design

and enforcement of the tax system in Greece, which have played a key role in the

exacerbation of fiscal deficits that led to the current sovereign debt crisis. They argue

that these shortcomings resulting in low tax revenue are related to the structure of the

Greek economy and to the failures of formal institutions, as all available indicators point

to the fact that the low and unfairly distributed tax yield is primarily due to the poor

functioning of the tax administration, lax tax enforcement, inefficiency of tax collection

and the lack of effective dispute resolution mechanisms. Such failures result in high tax

evasion and a thriving underground economy. The authors propose a number of specific

measures such as reorganizing tax offices, simplifying tax laws, rationalizing fines,

improving tax audits and establishing credible dispute resolution mechanisms while

emphasizing the fact that if policymakers are successful in introducing reforms that will

enhance the efficiency of the tax administration, this may be the first step in restoring

confidence in public institutions.

Matsaganis and Flevotomou (2010) use a tax benefit model to provide preliminary

estimates of the size and distribution of income tax evasion in Greece. With that method

they estimate income under-reporting at 10 per cent, resulting in a 26 per cent shortfall in tax

receipts. The paper finds that the effects of tax evasion are higher income inequality and

poverty, as well as lower progressivity of the income tax system.

Danopoulos and Znidaric (2007) highlight the fact that Greece has the highest level of tax

evasion among the 15 nations that made up the European Union prior to enlargement in

2004 and also the country’s underground economic activity remains alarmingly high. They

identify the major factors that prompt tax evasion which include the low level of education

and the high level of tax burden among others. They also refer to the negative effects of

informal economy which include damages in the reliability and trustworthiness of official

government statistics, making government policy, planning and efforts to attract foreign

and other forms of investment less than credible; renders government fiscal and spending

policy ineffective. However, there are also benefits in not paying taxes, as it leaves more

money in the hands of consumer and businesses leading to greater investment and prevents

the burden of excessive taxation.

Katsios (2006) highlights the interaction between the underground economy and

corruption, focusing on the determinants of the Greek economy, the tax and national

insurance burdens and the intensity of the relevant regulations in Greece, concluding that

Greece shows profound signs of a transition country in terms of the high level of regulation

leading to a large shadow economy. The taxation problems arising from high

administrative-compliance costs and bribery indicate the urgent need for tax reforms

designed to simplify the regulation framework. Improvement of the quality of Greek

Shadow

economy and

tax evasion

389

5. institutions and rationalization of administrative-compliance costs are a prerequisite for

successful and urgently needed tax reforms in terms of reducing the overall Greek shadow

economy, through the simplification of the regulatory framework.

Christopoulos (2003) uses data from Greece over the period 1960-1997 to examine

whether the underground economy responds asymmetrically to tax changes, both indirect

and direct. Asymmetry implies that taxpayers react in a different manner to tax increases

and to tax reductions. To test this hypothesis, the author specifies and estimates a vector

error correction model, and the empirical evidence suggests that when indirect and direct

taxes rise, taxpayers move into the underground economy as quickly as they move out of it

when indirect and direct taxes decrease. Thus, the empirical results do not give support to

the asymmetry hypothesis, and this has significant implications for the effectiveness of the

country’s fiscal policy.

3. Causes of informal economy and driving factors

For the black economy to exist, the following two conditions must be met:

(1) Those involved in the informal economy must have an incentive in order to decide

to take action in this area. In other words, the benefits they expect from expanding

their activities in the informal sector have to be larger than the suspected cost of

their revelation.

(2) The adequate opportunities should be provided, i.e. there exist employment

opportunities in the informal economy.

The most important factors, as identified by the literature, that lead people to become active

in the shadow economy are as follows.

3.1 The level of the tax burden

The level of tax burden and the high tax rates largely explain the existence and growth of

the shadow economy. Individuals and companies, by keeping hidden a part of their

economic activity, they manage to achieve lower tax burden. Especially in the case of

indirect taxes, there are benefits for all the parties involved, for example, buyers and sellers.

This mutual interest leads to cooperation between them to hide all or part of their trading. A

recent research published by the Institute of Economic Affairs (British Institute of Economic

Affairs, 2013) reveals that high tax rates have led to an underground economy equivalent to

a staggering 10 per cent of Britain’s GDP, with its worth been over £150bn. High levels of

public spending and tax increases led both individuals and enterprises to illegal

employment, thus creating a vicious cycle. The underground economy has as a direct

consequence the loss of tax revenues, and this in turn leads to an increase in tax rates, and

thus to the reinforcement of employment in the black market. Recent findings highlight the

fact that the punitive tax regimes have led to the exacerbation of the shadow economy,

resulting in more than 30 million people across the European Union been employed illegally.

Especially in Greece, a country among the most affected by the crisis in the Eurozone, illegal

activity accounts for over 20 per cent of national income.

3.2 The degree of acceptance of state power

A person will be more willing to develop activities in the black economy if it considers the

state as a power that seeks to limit the fruits of his labors compared to a person who believes

that the role of the state increases prosperity and promotes the common good. This

ideological attitude of people is expressed by the term tax consciousness or tax morality.

JMLC

20,4

390

6. 3.3 The level of unemployment

The level of unemployment is a feature of the economic and social structure of a country. The

degree of interaction between the two variables, unemployment and undeclared work, is not

easy to determine. According to a widespread perception, in an economic downturn,

especially in economies characterized by high inflation and rigidities in the labor market, an

increase in the level of unemployment is a reinforcing factor of undeclared employment. As

the recession periods are particularly relevant for the violation of institutional constraints

which weigh heavily on labor costs, unemployment appears to act as a reinforcing demand

factor, and hence supply, of undeclared employment. According to data published by the

Hellenic Statistical Authority, the unemployment rate in Greece in April 2016 stood at 23.3

per cent, versus 25.3 per cent in April 2015 and 27.1 per cent in 2014. The highest

unemployment rate for 2016 was recorded in Western Macedonia (27.6 per cent) and the

lowest in the Aegean (15.4). In 15-24 age group, unemployment increased to 47.4 per cent. A

further important aspect of the unemployment phenomenon is the evolution of the percentage

of long-term unemployed that is both impressive and disturbing. This group of the

workforce, which remains for a long time excluded from the formal labor market and is

inevitably led to social exclusion, is according to all estimates a significant undeclared labor

supply tank.

3.4 The degree of state intervention

The degree of state intervention may be measured in the number of laws and regulations,

including the laws change. In Greece, the laws, reforms and regulations are numerous as

well as the non-stop alterations every now and then, such as the liberalization of closed

professions that require a professional license (e.g. taxi, etc.), market regulations and

restrictions on the job market. The degree of intensity of state rules and regulations are

major factors which lead Greek citizens straight to the black economy. This is directly

related to the burden of social security contributions as regulations lead to an increase in

labor costs in the formal sector which in turn leads to an increase in unemployment (as

occurs in many OECD countries). All of the above provide an incentive for workers to be

used in the shadow economy, especially when labor costs are passed on to the same.

Thus, the unemployed are a double burden for the state, as they continue to receive social

benefits and if these activities, which are undertaken in the black economy, became

official then employers and employees would have payed less tax.

Of course, the percentage change in real labor cost per unit were 2.9 per cent in 2011, 7.4

per cent in 2012 and 1.1 per cent in 2013. This decrease reflects the significant decline in

turnover in almost all sectors of the Greek economy and the existence of significant

employment rate in informal or unofficial forms of employment. There was also a reduction in

the average gross earnings in the whole economy by 4.6 per cent in 2010, 1.7 per cent in 2011,

6.6 per cent in 2012 and 7.7 per cent in 2013 as the efforts made by the government under the

agreed memorandum for the country’s exit from the crisis intensify. There is a general rule that

the greater the number of rules and regulations which exist in an economy, the greater share of

total GDP is occupied by the informal sector. Indeed it has been found that an increase of one

percentage point of government regulations is related with an increase of 8.1 percentage points

to that share. Therefore, many studies suggest that the Greek government should give more

emphasis on the enforcement of laws and regulations rather than increasing their number.

3.5 The social security scheme

Social security charges are considered to be a very influential factor of the extent of the

black economy because, like high taxation, so the contributions paid by employers and

Shadow

economy and

tax evasion

391

7. employees contribute to the development of the shadow economy. Also, the fact that the

government provides various kinds of social benefits to poor, unemployed and generally to

people who have low incomes, motivates many people to be virtually presented as

beneficiaries of social benefits, without actually entitled to. Consequently, a number of

citizens have an incentive to operate in the black economy and to declare a lower income to

take advantage of such benefits thus, depriving valuable resources of the state and social

welfare.

3.6 The role of the state

The black economy is related to violation of state rules and therefore the state policy makers

should make serious efforts to mitigate it. In practice, however, often tolerated or supported

by the state, the grey economy, whether this is because it serves the interests of individuals

or social groups that have the ability to influence the institutions’ decisions or because it is

thought to contribute, in short term period, to the achievement of certain objectives of

economic policy as, for example, improving the balance of payments, increasing

employment and stimulating economic growth. Such phenomena are observed in the case

where the governmental mechanisms are loose and show a high level of tolerance on

something which is clearly forbidden, as for example the illegal immigration in Greece that

has skyrocketed the current period and has become a major threat for all Europe.

Therefore, it is not only the level of the administrative machinery but also the political

will that affect the size of the shadow economy. From all the above mentioned, several

studies have concluded that the most important causes for the creation of the informal

economy in many countries are the tax burden, the large number of freelancers and the

government restrictions. For Greece, in particular, it is found that the three most important

causes are unemployment, the large number of self-employed and social levies as part of the

overall tax burden.

3.7 Workforce synthesis and the number of self-employed

The synthesis of the workforce in Greece plays a vital role in creating and strengthening the

informal economy. This is due to the fact that the agricultural sector and related industries,

as well as the tourism sector, employ a high percentage of undeclared workers. So although

these people produce work, it does not appear in official statistics of GDP and their

insurance contributions are not paid despite grants and facilities offered by the state and the

European Union. In addition, self-employed are those who greatly contribute to the growth

of the informal economy according to a related research held by the British Institute of

Economic Affairs (2013). It is also argued that self-employed constitute one of the major

factors that lead to the formation of the underground economy regardless of the level of

economic development. For example, it was found that the informal economic activities

derived from this employment accounted for 10.6 per cent of GDP. This means that there is

lot of chance that all these professionals do not declare all their work and operate in the

black economy, as they have a larger number of deductible expenses, both from their tax

base and the taxation of their personal income, and they are subjected to fewer internal and

external controls compared to larger enterprises. Greece has the highest percentage of self-

employed in the EU according to Eurostat (2012) with 32 per cent of its employees,

compared with 15.1 per cent in the Eurozone and 15.2 per cent in the EU (32.8 million self-

employed). After Greece, the highest percentage of self-employed is found in Italy (23.4

per cent), Portugal (21 per cent) and Romania (20 per cent). In Greece, according to the study,

the percentage of uninsured workers stands at 37.3 per cent of the total, while the country

JMLC

20,4

392

8. also holds first place in the percentage of illegal immigrants working (4.4 per cent of the

total) followed by the USA (3.2 per cent).

4. Determinants and causes of tax evasion

Tax evasion is a global problem, but its range and effects depend on several factors, the

major of which are:

4.1 The educational level of the population

The higher the educational level the higher the grade of tax consciousness and the lower the

tax evasion trend. On the contrary, when the educational level is low, tax payers are not able

to understand the fact that tax revenues are the main source for the financing of public

goods (health, security, etc.) which satisfy critical social needs.

4.2 The level of tax burden in comparison to the aggregate income

The higher the level of the burden by a single tax, the higher the benefit for a tax payer by

tax evasion. Subsequently, the higher the average tax burden, the higher the trend for tax

evasion due to the restriction of the individual’s basic needs (food, clothing, etc.) that

becomes more noticeable and the gain by the tax amount outweighs for the risk taken in

case of tax evasion apocalypse.

4.3 The distribution way of tax burdens

If the distribution of tax burdens responds to the prevailing view for social justice, then the

trend for tax evasion is smaller. On the other hand, when the principle of fair distribution is

violated with the implementation of tax exceptions to specific private entities, then a handful

of unpleasant consequences occur:

the sense of unfairness is cultivated among the tax payers and reinforced by their

will to assimilate in any possible way with those excepted from tax;

increases the level of total tax burden as the amounts to be paid by those exempted

have to be given by the rest; and

creates unequal conditions of competition between favored and non-favored

companies as taxes generally affect the production and business plans of private

productive units.

4.4 The structure of the taxation system

The type and cash significance that constitute the taxation system of a country determine

the range of tax evasion. As a result, if the taxation system is dominated by direct taxes, i.e.

income taxes, then the tendency for tax evasion is bigger because private entities have more

opportunities to hide their tax than individuals. This can be done in the following two ways:

(1) households like freelancers by declaring lower income than the real one; and

(2) companies by transferring part of their profits to depreciation accounts, research

expenses, etc.

On the other hand, if the taxation system consists mostly of indirect taxes, the trend for tax

evasion is smaller because the tax control is more effective, the related taxed units are fewer,

and they are also obliged to keep accounting books from which taxation can be accrued like

value-added tax (VAT). Of course, this is a general rule that does not apply in the unique

Shadow

economy and

tax evasion

393

9. case of Greece. This is justified by the fact that while indirect taxes are more important than

the direct in Greek taxation system, tax evasion is very high due to the existence of an

ineffective control mechanism and high levels of corruption.

4.5 The degree of market and business organization

When the economy is organized in such a way that a significant proportion of transactions

take place in kind, for example, the possibility of tax evasion will be greater compared with

an economy where all transactions are made with money. Moreover, if companies operating

in one country are numerous but small, the evasion potential is large because the accounting

of these enterprises is low; thus, monitoring by the tax authorities becomes difficult or even

impossible. In contrast, in countries where companies are fewer and larger their monitoring

by tax authorities is easier.

4.6 The level of development and organization of the economy

In well-organized economies, transactions between taxpaying units are easily recorded, and

tax authorities have available more reliable stuff, e.g. transaction documents etc., so as to

properly perform their work. Therefore, they can relatively easily reduce the tendency of

taxpayers for tax evasion.

4.7 The structure of the national income

The structure of the national income is very important to the extent of tax evasion. This is

especially true for evasion of income tax because there are incomes where tax evasion is

necessarily limited if not impossible, while in other cases, its inhibition is difficult. In the

first case are the incomes from salaries and pensions. In the second is the income from the

exercise of agricultural activities and business.

5. Size of Greek shadow economy in comparison with other Organization for

Economic Co-operation and Development countries

According to recent estimates by Schneider (2013), prolonged economic crisis in Greece

and Spain has somehow reduced the phenomenon of the underground economy, and more

specifically, the recession in the formal economy in both countries is so strong and also

reductions in the income of citizens so great, having vertically further decrease even the

demand for the activities of the shadow work (e.g. house-keepers etc.). As a result, the

informal sector in both countries is declined substantially: while in Greece, in 2013, it

accounted for 23.6 per cent of GDP, compared to 24 per cent in the past year, 25.1 per cent

in the pre-crisis 2007 and 28.2 per cent in 2003, while in Spain, it estimated to have fallen

to 18.6 per cent of GDP, from 19.2 per cent in 2012 and 22.2 per cent in 2003. Meanwhile,

the fight against tax evasion in Greece has begun, to some extent, to pay off. More

specifically, the amount of tax evasion related to indirect taxes and self-employment in

Greece decreased to 4 per cent of GDP in 2010 from 5.6 per cent in 2009. In the years to

follow, 2012 and 2013, the shadow economy has decreased in most of the 38 countries of

the OECD, compared with 2008. However, contrary to other countries, the reason of the

reduction in Greece was the prolonged economic crisis. With the official economy either

recovering or growing rapidly, people have less incentive to develop further activities in

the shadow economy. In the following table, the average relative impact of the main

determinants of the underground economy of 38 OECD countries, for the decade 2000-

2010, is presented (Table I).

JMLC

20,4

394

12. Concerning the most critical factors which matter the most to the creation of the informal

economy in 38 OECD countries for the period 1999 to 2010, indirect taxation ranks first

(average 29.4 per cent) and self-employment second (22.2 per cent), while in Greece the figure

is reversed. Specifically, in Greece self-employment plays by far the most crucial role in the

size and growth of the shadow economy (37.6 per cent), followed by indirect taxation (21.8

per cent). Both in the 38 countries and Greece, unemployment ranks third in the list of

factors with the greatest impact on the size and growth of the shadow economy, with a share

“contribution” of 16.9 per cent (at 38) and 18 per cent, respectively (due to the fact that lack of

work often incites the unemployed in illicit economic activity to ensure their living). Overall,

in 2012, Greece ranked ninth among the 27 EU Member States, in terms of the black

economy (24 per cent of GDP), significantly exceeding the EU average (18.4 per cent), as seen

in the next Figure 2.

In the first place is Bulgaria where the shadow economy represents 31.9 per cent of

GDP, followed by Romania (29.1 per cent), Lithuania (28, 5 per cent), Estonia (28.2

per cent), Latvia (26, 1 per cent) and Cyprus (25.6 per cent). Reversing the list, the less

shadow economy in the EU-27 has Austria (only 7.6 per cent), followed by Luxembourg

(8, 2 per cent), The Netherlands (9.5 per cent) and the UK (10.1 per cent). The size of the

shadow economy in Greece as of 2012 was estimated at e60bn of which; however, only

Figure 2.

Size of the shadow

economy of EU-27 in

2012 (percentage of

GDP)

Shadow

economy and

tax evasion

397

13. e20bn were recorded to the official GDP as derived from partially legitimate activities,

while the remaining e40bn came from illegal activities.

6. Effects of the black economy and tax evasion on Greek economy

6.1 Negative effects

Having identified the causes of the black economy and the factors that contribute to

the systematic increase of tax evasion, at this point, we are going to refer to their

direct negative impact on Greek economy. The main effects are summarized to the

following:

The principle of fair distribution of the tax burden is violated.

The existence of high level of tax evasion does not allow the collection of the

required revenues for the satisfactory and proper functioning of the public sector.

Fiscal policy bodies are unable to use the tax system effectively in favor of the

economic development of the country, because the effectiveness of the statutory

exemptions which are granted as incentives to promote this objective is

weakening.

Serious social injustices are caused and an unequal redistribution of income is

developed, from the moral taxpayers to the tax evaders. Because evasion belongs

mainly to the higher economic classes, this redistribution of national income is not

desired by the society as wealth differences become even more bigger.

The state may face cash flow problems as it happens in Greece nowadays. This has

led to an increase in taxes, to state borrowing and to a reduction in government

spending (e.g. education, health, etc.). This condition can also cause chronic budget

deficit, continuous use of borrowings and accumulation of sovereign debt, with all

the known catastrophic consequences in the economy.

In Greece, the problem of non-payment of taxes has taken great dimensions and the

consequences became even more intense as the economic crisis deepens in the country.

According to a recent survey of the Economic Chamber of Greece on “Measurement of Tax

Consciousness”, it was found out that:

eight of ten respondents believe that tax evaders are doing so because “there is little

chance of detection” by tax control authorities;

one of five are prepared to take the risk of hiding their income, even if aware that it

is possible to be identified by the tax authorities;

almost one in two respondents believe that “if you want to conceal income from the

tax authorities, you can carry out”;

one in ten admit to having attempted to cheat the tax authorities regarding their real

income;

eight of ten consider it their moral obligation to declare their real income; and

one in two citizens consider that in a highly corrupted state, tax evasion is a

reasonable reaction.

Conclusively, the failure to arrest tax evaders and the extent of corruption are critical factors

in determining the fiscal behavior of citizens and the effectiveness of tax revenue collection

by the state.

JMLC

20,4

398

14. 6.2 Positive consequences

As explained before, black economy and tax evasion have severe negative consequences on

the Greek economy being one of the main reasons for the ongoing fiscal and financial crisis

that plagues the country. But on the other hand, there are also several positive effects which

are mainly connected to employment and income creation. First, the informal sector of the

economy often functions as a life vest for businesses, as it enhances their competitiveness. In

the formal economy, increasing labor costs and the rise of tax burden create very often

problems of competitiveness both in the international and in the internal market and

encourage companies to the underground side of the economy to avoid government barriers

and gain competitive advantage.

Another positive effect is the fact that black economy helps in creating new job

positions by absorbing workforce. If it was not for the shadow economy many people

which find employment in the informal sector would be unemployed. Of course, there are

also negative consequences for workers in the informal sector such as the lack of

insurance. Moreover, the higher the level of the shadow economy, the greater the

difference among the formal and informal economy. The informal economy has resulted

in the exemption of certain individuals, while on the other side, increases the tax burden

of those people employed in the formal economy. Taking for granted that persons

employed by the informal sector are usually low-income people one might say that

shadow economy helps improve the disposable income distribution and therefore

increases the social welfare. Finally, it is estimated that approximately 66 per cent of the

informal economy revenues are returned immediately in the formal economy by

increasing consumption of households, mainly for durable goods and services, thereby

contributing to economic growth and tax revenues. The informal sector may also help in

creating markets, fostering entrepreneurship and what is very important for Greece,

changing the legal, social and economic factors which are necessary so as to achieve the

desired development.

All of the above provide a positive image of the shadow economy that may lead

someone to the conclusion that there should not be great effort to crack it down,

especially in times of recession and rising unemployment. But any benefits of the black

economy are uncertain and always extremely short. Furthermore, informal activities

undermine long-term planning and the implementation of strategies aimed at developing

the economy on sound bases. For this reason, it is more than necessary the existence and

implementation of a long and rigorous policy to combat the grey economy.

7. Measures for combating tax evasion and shadow economy

7.1 Measures for tax evasion

The ability of tax authorities to tackle satisfactorily the trend of taxpayers for tax evasion

depends on the degree of organization of tax consulting services, the quality of tax

accounting institutions, the system used for the assessment and collection of taxes, the

structure of the tax system and finally the degree of accounting organization of economic

units. It is obvious that if taxpayers feel that the state is able to detect tax evasion, the

tendency for such action would be limited and vice versa.

But it is common knowledge that tax evasion has deep roots in the Greek economy and

cannot be easily eliminated. Therefore, certain measures are proposed to deal with this

major problem. They are as follows.

7.1.1 Regular checks on persons and companies. These checks should be performed

based on the profile of tax evaders and randomly. The control based on the profile will focus

mainly on individuals and companies which have higher chances of tax evasion. On the

Shadow

economy and

tax evasion

399

15. other hand, checks on persons and businesses that do not fit the above profile will be

checked randomly. Thus, tax evasion levels will be monitored continuously so as

appropriate measures to be undertaken.

7.1.2 Automatic cross-check of receipts and related documents. To strengthen the role of

receipts in the improvement of tax revenues collection, it can be examined the possibility to

increase the tax credit for certain expenditure, even if it is done at the expense of tax

revenues. That way, there will be a shift in the mentality of taxpayers and will now be

considered obvious the issuing of receipts for any kind of service.

The European Union, to address this phenomenon and protect member states,

established in 1993 the VIES system, where firms are monitored making intra-

community trade for the proper return of VAT. In every located case, the way each

invoice is paid off is checked, i.e. if there is a bank document for the collection or payment.

When no such documents exist and the company claims that the transaction was made in

cash and without the mediation of a bank, then the case will be considered suspicious and

will be investigated in depth.

7.1.3 Professional accounts. On January 1, 2011, it has been decided that all transactions

between any enterprise and the payrolls should be made mandatory through commercial

bank accounts. This measure, of course, has not been yet implemented, but huge efforts are

made to achieve this goal.

7.1.4 Electronic invoicing and signature certification. In conjunction with the business

accounts, another measure which moves in the right direction is electronic invoicing and

certification of electronic signatures, where the application will be made among businesses

and between businesses and public.

7.1.5 Re-organization of tax services. In this sector, the establishment of a specific service

is required, which will control individuals with large incomes, using data and information

collected from different areas. The mission of this specialized service would be investigation,

methodology, control and detection of tax evasion in areas of illegal trade as well as its

confrontation, in cooperation with other bodies.

7.1.6 Education. The area of education should be reconfigured in all its stages, from

primary level up to university. It is appropriate to teach students, from the beginning of

their learning activity, the correct moral principles, about how they should behave in the

future, as potential entrepreneurs or employees so as to have increased tax consciousness, in

all areas of the economy.

7.1.7 Active citizens. Every citizen ought to become active, but at the same time, the

legislation of the country needs to be amended and the public administration to be

upgraded.

7.1.8 Simplification of legislation. This measure aims to provide a simplified legislation

to be understood by all citizens, regardless of age, educational level, etc. At the same time,

the technical support by the related information systems, such as TAXIS, must be

reinforced so as to place constant controls and crossings of tax information to better serve

the fight against tax evasion.

7.1.9 Amplification of transparency. There must also be correct and effective

management and distribution of taxes paid by the citizens in the state and targeted

fiscal policy to reduce government spending. Achieving this will enable the reduction of

tax evasion, a fact which will enhance the trust of citizens to the state. Citizens, by

paying taxes corresponding to each one and seeing that the money paid to the state, are

properly exploited, covering crucial public needs such as health, education, etc., then

and only then shall taxpayers trust the state, as they see the society in which they live,

JMLC

20,4

400

16. to thrive. It is therefore a more than important incentive for citizens to pay to the state

what it owns and in this way, tax evasion to be avoided.

7.2 Measures for shadow economy

From time to time, several measures have been proposed by the Greek Governments to

find appropriate ways to deal with the phenomenon of the informal economy. Some of

these propositions are in place, but even more are “frozen”, without ever to be able to be

applied. The most significant of these measures as well as new ones are summarized

below:

7.2.1 Incentives for voluntary compliance. Tax authorities around the world adopt

increasingly in recent years, various strategies which aim to the consolidation and adoption

of fiscal conscience by taxpayers. In these strategies, the continuous increase of voluntary

compliance by taxpayers to the tax authorities is also provided. In this way, a gradual

reduction of the cost of the tax audit will be achieved, and also violations and irregularities

that have been committed will be revealed by the taxpayers themselves.

7.2.2 Regulations for young entrepreneurs. One of the most important measures is the

tax authority to pay special attention to creating a climate of mutual trust with taxpayers

and especially with young entrepreneurs who are new comers on the market. Experience

shows that the special treatment of new traders through education and specific guidance

creates a degree of benefits, as for example increased voluntary compliance with the rules

of the tax authorities.

7.2.3 Incentives for disclosure of violating behavior concerning tax issues. There should

be certain incentives to taxpayers to disclose cases for which there should be elements that

have actually taken place, as that in these cases, the taxpayers will be exempt from fines and

other kind of penalties.

7.2.4 Expenditures discounts of the tax payers’ income. In this sector what is required is

whatever legitimate deductions or exemptions are provided by law for the taxpayers, not to

be hidden, but to be given so as to allow taxpayers and state to build a mutual trust.

7.2.5 Fair tax burden. It is necessary to develop a fair taxation system and the tax

burden to meet and be consistent with the real conditions of the economy.

7.2.6 Control mechanisms and frequent checks. A measure that would be quite effective

is the strengthening of the control mechanisms and the performing of frequent checks by the

relevant departments for better addressing of the problem.

7.2.7 Education. As for tax evasion, so for the underground economy, education is of

great importance, where there could be tax courses at all levels of education. For those

interested in expanding their knowledge of the taxation, it would be very useful to attend

related courses such as financial accounting, etc.

7.2.8 Legislation simplification. Simplification of legislation should be a priority, so as to

enable companies to know in a clear way, what are their tax obligations to avoid unpleasant

situations.

7.2.9 Improvement of productivity. There is an urgent need to increase the productivity

of the entire public sector, of the tax assessment authorities not only to improve the methods

of organization and administration but also to improve quality.

7.2.10 Registration of foreigners-immigrants. There should be strict registration of

foreigners, as it is generally accepted that the largest proportion of workers employed

without insurance are immigrants. This is because it is profitable for entrepreneurs, as

they offer relatively low wages which do not correspond to the work that can be

performed by employees, or in hours that can work in the business. On the other hand,

from this situation foreign immigrants also benefit because they can work without a

Shadow

economy and

tax evasion

401

17. residence permit, having secured a small income to enable them to cover the essentials

(e.g. housing, food, clothing, etc.). In this sector, therefore, companies must become more

sensitive, so as not to resort to illegal employment of foreigners, but to oppose, thus

preventing a large part of the informal economy. Motivation and support from the state is

crucial in this direction, especially nowadays that the migration flows from Syria have

become a scourge and threaten the whole socioeconomic structure of Greece.

8. Conclusion

Tax evasion is a serious cause for large public deficits by provoking lack of financial

sources, thus making the state unable to cover its costs. This leads the government to

increased external and internal borrowing. The first means less independence and

freedom of economic and other options for the country and also an increase in

government debt due to higher interest rates of foreign borrowing. The second is an

increase in interest rates to attract private capital to meet the public deficit, but this

deteriorates the circulation of money in the market and captures large private funds,

resulting in the reduction of private investments, which is absolutely necessary for the

development of economy. The overall result is economic stagnation and loss of

competitiveness, a critical and long-lasting drawback of the Greek economy. Even

more, tax evasion means creating disparities among citizens, as some professions can

evade taxes and some not, which not only creates inequality of the burden on taxpayers

but also taxes become onerous for non-tax evaders because of government revenue lag,

which is usually covered by the burden of those who already pay taxes. Another

negative consequence of tax evasion is that companies are discouraged from new

investments and risk taking so as to increase their profitability, as this can be

accomplished on a much easier way through not payment of taxes. Tax evasion means

wasting resources in unproductive activities, as it creates high transaction costs for tax

evaders. It also entails high administration and transaction costs for the government, as

it has to establish and maintain an effective control mechanism that is essential for

purposes of mitigation of tax evasion. On the other hand, the underground economy,

whose main part and cause is tax evasion, means that many private incomes remain

outside official statistics and calculations as, for example, GDP are not properly

reflected to the real economic situation. Therefore, the governments do not have an

accurate picture of the situation and are likely to take wrong decisions in relation to the

economy and the creation of revenues, thereby imposing additional burdens on

consistent and law-abiding taxpayers. Even more if we take into account that the

activities of tax evaders are paid in cash, tax evasion reduces the elasticity of cash

demand to changes in public interest rates which means more difficulties in

implementing monetary policy. Finally, measures which should be implemented to

reduce the black economy in Greece and increase the growth rate are mainly related to

consistent and fair tax practices. It is also considered important to reduce the existing

restrictions on product and labor markets (overregulation) in order the access to the

formal economy to be easier and more attractive, while placing regular checks and

sanctions where necessary to achieve compliance with tax authorities. It is the only way

to start diminishing corruption of public servants and citizens, too. Last but not least,

related inquires must be performed so as to identify why Greek citizens evade taxes and

what they would like to receive as goods and services in exchange for preferring the

formal economy. It would also be useful to consider what is it for which citizens would

be willing to comply to establish an honest relationship with the state.

JMLC

20,4

402

18. In conclusion, the measures to tackle tax evasion and the underground economy in

Greece are almost identical to the measures for addressing the effects of the debt crisis

which still plagues the country. As research on the topic of the informal economy remains

difficult and relatively limited, due to lack of sufficient and integrated data, economic

research should go even deeper in this crucial issue. Greece, a relatively developed economy

with high percentage of shadow economy and tax evasion, provides a fruitful ground for

study as proven by the present analysis.

References

Artavanis, N., Adair, M. and Margarita, T. (2015), “Tax evasion across industries: soft credit evidence

from Greece”, National Bureau of Economic Research, No. w21552.

Berger, W., Pickhardt, M., Pitsoulis, A., Prinz, A. and Sardà, J. (2014), “The hard shadow of the Greek

economy: new estimates of the size of the underground economy and its fiscal impact”, Applied

Economics, Vol. 46 No. 18, pp. 2190-2204.

Bitzenis, A., Vlachos, V. and Schneider, F. (2016), “An exploration of the Greek shadow economy: can

its transfer into the official economy provide economic relief amid the crisis?”, Journal of

Economic Issues, Vol. 50 No. 1, pp. 165-196.

British Institute of Economic Affairs (2013), “The shadow economy”, available at: www.iea.org.uk

Christopoulos, D.K. (2003), “Does underground economy respond symmetrically to tax changes?

Evidence from Greece”, Economic Modelling, Vol. 20 No. 3, pp. 563-570.

Danopoulos, C.P. and Znidaric, B. (2007), “Informal economy, tax evasion, and poverty in a democratic

setting: Greece”, Mediterranean Quarterly, Vol. 18 No. 2, pp. 67-84.

Eurostat (2012), European Union Labour Force Survey, Annual Results 2012 – Issue number 14/2013,

Eurostat.

Kaplanoglou, G. and Rapanos, V.T. (2013), “Tax and trust: the fiscal crisis in Greece”, South European

Society and Politics, Vol. 18 No. 3, pp. 283-304.

Katsios, S. (2006), “The shadow economy and corruption in Greece”, South- Eastern Europe Journal of

Economics, Vol. 1, pp. 61-80.

Matsaganis, M. and Flevotomou, M. (2010), Distributional Implications of Tax Evasion in Greece.

Remeikiene, R., Ligita, G. and Jekaterina, K. (2014), “Country-level determinants of the shadow

economy during 2005-2013: the case of Greece”, Mediterranean Journal of Social Sciences,

Vol. 5 No. 13, p. 454.

Schneider, F. and Buehn, A. (2012a), “Shadow economies in highly developed OECD countries: what are

the driving forces?”, IZA Discussion Paper no. 6891.

Schneider, F. and Buehn, A. (2012b), “Size and development of tax evasion in 38 OECD countries: what

do we (not) know?”, CESifo Working Paper no. 4004.

Schneider, F. (2013), Size and Development of the Shadow Economy of 31 European and 5 Other OECD

Countries from 2003 to 2013: A Further Decline, Johannes Kepler Universität, Linz, pp. 5-7.

Further reading

Dell Anno, R., Gomez-Antonia, M. and Alanon-Pardo, A. (2007), “The shadow economy in three

mediterranean countries: France, Spain and Greece”, Empirical Economics, Vol. 33 No. 1, pp. 51-84.

Economic Chamber Economic University of Athens (2011), “Economic chamber economic

university of Athens, department of statistics”, Research of Tax evasion in Greece.

IMF (2006), “Report on the observance of standards and codes”, Fiscal Transparency Module, WA.

OECD (2009), “Tax administration in OECD and selected non-OECD countries: comparative

information series”, (2008), Forum on Tax Administration, Paris.

Shadow

economy and

tax evasion

403

19. Schneider, F. (2002), Size and Measurement of the Informal Economy in 110 Countries Around the

World, available at: rru.worldbank.org

Schneider, F. (2005), Shadow Economies of 145 Countries all Over the World: What do We Really

Know?, Mimeo: University of Linz.

Schneider, F. (2007), “Shadow economies and corruption all over the world: new estimates for 145

countries”, Economics, the Open Access, Open Assessment e- Journal, No. 2007-9.

Schneider, F. (2010), “Size and development of the shadow economy of 31 European countries from 2003

to 2010 (revised version)”, Working Paper, University of Linz.

Schneider, F. (2011), “Size and development of the shadow economy of 31 European and 5 other OECD

countries from 2003 to 2012: some new facts”, Consultado en, available at: www.economics.

unilinz.ac.at/members/Schneider/files/publications/2012/ShadEcEurope31.pdf

Tafenau, E., Herwartz, H. and Schneider, F. (2010), “Regional estimates of the underground economy in

Europe”, International Economic Journal, Vol. 24 No. 4, pp. 629-636.

Vousinas, G. (2016), “Greek sovereign debt deficit: determinants, evolution and effects on the

economy. an empirical study with policy aspects”, Proceedings of the International Conference

on Business Economics of the Hellenic Open University, Athens.

Corresponding author

Georgios L. Vousinas can be contacted at: vousinas@yahoo.com

For instructions on how to order reprints of this article, please visit our website:

www.emeraldgrouppublishing.com/licensing/reprints.htm

Or contact us for further details: permissions@emeraldinsight.com

JMLC

20,4

404