Recommended

More Related Content

Similar to Magic Blades stock has risen rapidly to $50 per share. Th.docx

Similar to Magic Blades stock has risen rapidly to $50 per share. Th.docx (20)

More from smile790243

More from smile790243 (20)

Recently uploaded

Recently uploaded (20)

Magic Blades stock has risen rapidly to $50 per share. Th.docx

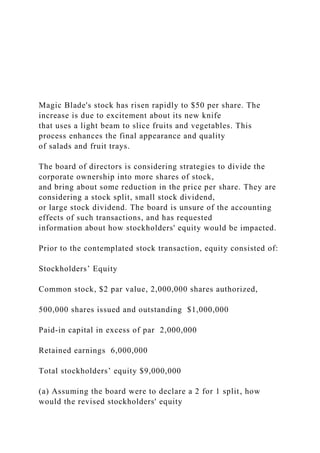

- 1. Magic Blade's stock has risen rapidly to $50 per share. The increase is due to excitement about its new knife that uses a light beam to slice fruits and vegetables. This process enhances the final appearance and quality of salads and fruit trays. The board of directors is considering strategies to divide the corporate ownership into more shares of stock, and bring about some reduction in the price per share. They are considering a stock split, small stock dividend, or large stock dividend. The board is unsure of the accounting effects of such transactions, and has requested information about how stockholders' equity would be impacted. Prior to the contemplated stock transaction, equity consisted of: Stockholders’ Equity Common stock, $2 par value, 2,000,000 shares authorized, 500,000 shares issued and outstanding $1,000,000 Paid-in capital in excess of par 2,000,000 Retained earnings 6,000,000 Total stockholders’ equity $9,000,000 (a) Assuming the board were to declare a 2 for 1 split, how would the revised stockholders' equity

- 2. appear? (b) Assuming the board were to declare a 15% stock dividend, how would the revised stockholders' equity appear? B-14.07 Stock dividends and splits x SPREADSHEET TOOL: Holding a cell reference constant Mike Highlight Summary information for Branford Corporation's balance sheet follows: BRANFORD CORPORATION Balance Sheet August 15, 20X4 Assets

- 3. Cash $ 125,000 Accounts receivable 250,000 Inventory 750,000 Property, plant, & equipment (net) 860,000 Total assets $1,985,000 Liabilities Accounts payable $125,000 Accrued liabilities 260,000 Notes payable 290,000 Total liabilities $ 675,000 Stockholders’ equity Common stock, $5 par $700,000 Paid-in capital in excess of par 300,000 Retained earnings 310,000 Total stockholders’ equity 1,310,000 Total liabilities and equity $1,985,000 Branford's business is growing rapidly, and the company needs to expand its manufacturing facilities. This expansion will require the company to obtain an additional

- 4. $1,000,000 in cash. The company is exploring five alternatives to obtain the necessary capital: Equity structure and impact I-14.01 Mike Highlight 366 | CHAPTER 14 DEBT OPTION: Branford is able to borrow, on a 5-year note, the full amount needed. The interest rate on this note would be 7%, and the note would require monthly payments. COMMON STOCK OPTION: Branford has identified an investor who is willing to pay $1,000,000 for 40,000 newly is- sued common shares. Common shares have been paying a dividend of $0.50 per share. Branford anticipates that this dividend rate will be maintained. NONCUMULATIVE PREFERRED STOCK OPTION: Branford has identified a hedge fund that will pay $1,000,000 for 8% noncumulative preferred stock to be issued at par. CUMULATIVE PREFERRED STOCK OPTION: Branford has identified an insurance company that will pay

- 5. $1,000,000 for 6% cumulative preferred stock to be issued at par. CONVERTIBLE PREFERRED STOCK OPTION: Branford has identified a retirement fund that will pay $1,000,000 for 4% cumulative preferred stock to be issued at par. The preferred stock must be convertible into 25,000 shares of common stock at the option of the retirement fund. (b) Which of the alternative financing scenarios involve fixed committed payments to investors, and which involve discretionary payments? (c) Which one of the alternative financing scenarios presents the least risk to existing shareholders? Which one of the scenarios involves the most ownership dilution for existing shareholders? Three of the following statements are patently false. Find the three false statements. The other statements are true, and may include additional insights beyond those mentioned in the textbook. “Earnings” is synonymous with “income from continuing

- 6. operations plus or minus the effects of any discontinued operations or extraordinary items.” Changes in accounting estimates must be reported by retrospective adjustment. EBIT and EBITDA are accounting values that are required to be reported on the face of the income statement. Other comprehensive income can be reported on the face of a statement of comprehensive income or in a separate reconciliation. When there is reported change in value for available for sale securities, “comprehensive income” becomes synonymous with “net income.” Book value per share is an amount related to shares of common stock. Trinity Railway began 20X5 with 900,000 shares of common stock outstanding. On March 1, 20X5, Trinity Railway issued 300,000 additional shares of common stock. 50,000 shares of common stock were reacquired on October 1. Trinity Railway reported net income of $2,275,000 for the year ending December 31, 20X5. Trinity Railway paid $250,000 in common dividends during 20X5. B-15.05 Concepts including OCI/ROA/EBIT/EBITDA/etc. B-15.06 Earnings per share Mike

- 7. Highlight Mike Highlight (a) Calculate the weighted-average common shares outstanding for 20X5. (b) Calculate basic earnings per share for 20X5. Calculate the price earnings ratio, PEG ratio, dividend rate, and dividend payout ratio for each of the following companies. Will each ratio consistently rank the companies from "best" to "worst" performer? Earnings Per Share Dividends Per Share Market Price Per Share Average Annual Increase in Earnings Andrews Corporation $2.50 $0.00 $25.00 5% Borger Corporation $1.00 $1.00 $18.00 10% Calvert Corporation $5.00 $2.50 $20.00 5%

- 8. P/E, PEG, Dividend rates B-15.07 x Mike Highlight Fairfield Corporation owns three separate subsidiaries. The Board of Directors is developing a strategy to withdraw $1,000,000 in cash from one of the subsidiaries to finance the acquisition of a fourth business. Prepare the current and quick ratio for each subsidiary, and rank order the subsidiaries based on their ability to pay a dividend to the parent company without jeopardizing liquidity. Sub A Sub B Sub C Cash $1,000,000 $3,000,000 $ 5,000,000 Trading securities 3,000,000 2,000,000 1,000,000 Accounts receivable 6,000,000 5,000,000 14,000,000 Inventory 4,000,000 8,000,000 7,000,000 Prepaid rent 2,000,000 2,000,000 3,000,000

- 9. Accounts payable 5,000,000 2,000,000 8,000,000 Interest payable 1,000,000 1,000,000 6,000,000 Note payable (due in 6 months) 4,000,000 1,500,000 4,000,000 Unearned revenues 3,000,000 500,000 2,000,000 B-16.01 Liquidity analysis x Mike Highlight Following is an incorrectly prepared statement of cash flows for Herman Corporation. Review and correct this presentation, using a direct approach. HERMAN CORPORATION Statement of Cash Flows For the Year Ending December 31, 20X2 Cash balance at January 1, 20X2: $ 175,000

- 10. Cash receipts during 20X2: Sale of building $ 800,000 Dividend received on investments 10,000 Cash received from customers 2,350,000 Proceeds from issuing stock 1,400,000 4,560,000 Cash payments during 20X2: Purchase of inventory $ 760,000 Interest on loans 56,000 Income taxes 124,000 Repayment of long-term note payable 2,000,000 Purchase of equipment 435,000 Selling and administrative expenses 696,000 Dividends on common 175,000 (4,246,000) Cash balance at December 31, 20X2 $ 489,000 Noncash investing/financing activities: Bought land by issuing promissory note payable $ 450,000 B-16.09 Rearranging cash flows in good form - direct approach Mike

- 11. Highlight Mike Typewritten Text OPTIONAL - EXTRA CREDIT Mike Typewritten Text Mike Typewritten Text Mike Typewritten Text Mike Typewritten Text Mike Typewritten Text Mike Typewritten Text Review the following technical comments about the presentation methodology for the statement of cash flows. Identify if the comment pertains to the "direct" or "indirect" approach, or "both." The operating cash flows section typically begins with net income. Separate disclosure is provided for noncash investing/financing

- 12. activities. Requires supplemental disclosure reconciling net income to operating cash flows. Conceptually, the preferred approach. Includes three separate sections - operating, investing, and financing. Requires supplemental disclosure of cash paid for interest and cash paid for taxes. A loss on the sale of a plant asset would be added back in operating cash flows. Waguespack Corporation and Hedrick Corporation had identical cash positions at the beginning and end of 20X9. Each company also reported a net income of $150,000 for 20X9. Evaluate their cash flow statements that follow. Which company is displaying elements of cash flow stress? What factors cause you to reach this conclusion? What is the importance of evaluating a company's cash flow statement? Knowledge of cash flow statement components B-16.11 Company cash flow evaluation B-16.12 Mike Highlight Mike

- 13. Highlight WAGUESPACK CORPORATION Statement of Cash Flows For the Year Ending December 31, 20X9 Cash flows from operating activities: Net income $150,000 Add (deduct) noncash effects on operating income Depreciation expense $ 20,000 Gain on sale of equipment (185,200) Increase in accounts receivable (45,000) Decrease in inventory 37,500 Increase in accounts payable 11,400 Decrease in income taxes payable (3,000) (164,300) Net cash provided by operating activities $ (14,300) Cash flows from investing activities: Sale of equipment 204,900 Cash flows from financing activities: Proceeds from long-term borrowing 20,000

- 14. Net increase in cash $210,600 Cash balance at January 1, 20X9 66,000 Cash balance at December 31, 20X9 $276,600 HEDRICK CORPORATION Statement of Cash Flows For the Year Ending December 31, 20X9 Cash flows from operating activities: Net income $150,000 Add (deduct) noncash effects on operating income Depreciation expense $160,000 Decrease in accounts receivable 43,700 Increase in inventory (87,500) Decrease in accounts payable (8,100) Decrease in income taxes payable (8,600) 99,500 Net cash provided by operating activities $249,500 Cash flows from investing activities: Purchase of equipment (20,400) Cash flows from financing activities: Repayment of long-term borrowing (18,500)

- 15. Net increase in cash $210,600 Cash balance at January 1, 20X9 66,000 Cash balance at December 31, 20X9 $276,600 Perfect Pad manufacturers floor mats for trailers that are used to transport horses. The mats provide for a firm footing surface that quickly sheds water. Mats are made to customer specifications via orders submit- ted over an internet site. The mats are completed and shipped in about one day. As a result, Perfect Pad does not maintain any work in process or finished goods inventory. The following costs were incurred in producing and selling mats during August: Synthetic rubber used in the mat $134,300 Lubricant used in the molding machine 14,000 Factory rent 9,600 Electricity to run the molding machine 2,600 Labor cost of machine operators 34,100 Internet sales site 1,500 Administrative salaries 12,500 Depreciation of molding machine 7,400 Salary of factory safety inspector 3,500

- 16. Office rent 13,500 Evaluate these costs, and determine the amount of direct material, direct labor, factory overhead, and sell- ing/general/administrative costs. Next, identify how much is considered to be a "prime cost" and how much is considered to be a "conversion cost." Direct material/direct labor/factory overhead/SG&A B-17.04 Mike HighlightWeek 5 - Homework Problems - ACCT301.pdfWeek 5 - Homework Problems - ACCT301.pdf3 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 3713 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 3723 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 3733 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 3973 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 3983 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 4233 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 4273 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 4283 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 4293 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 3983 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 4233 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 4273 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 4283 - TEXT - ACCT221 - Walther, Accounting - May 2015 (part 1) 429B-17.04Problem