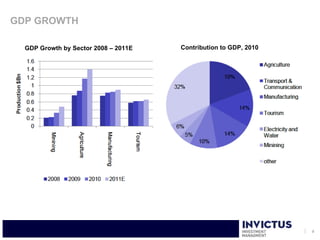

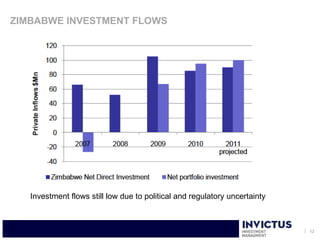

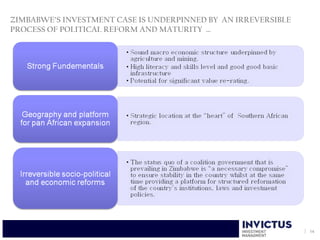

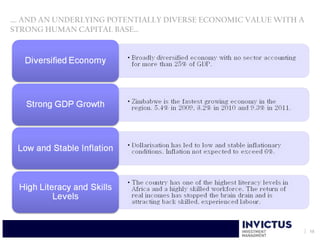

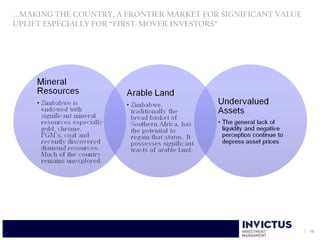

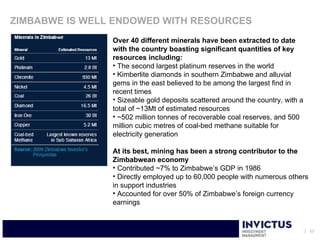

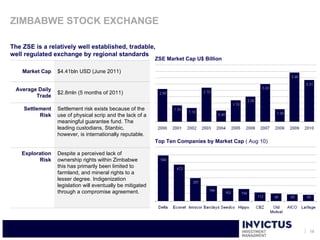

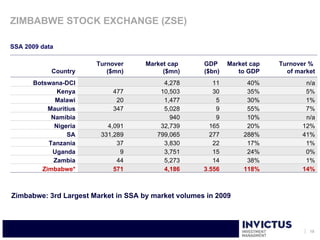

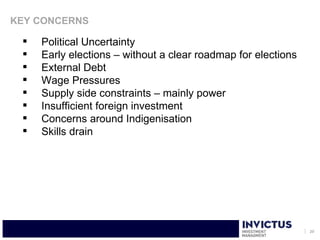

Zimbabwe is recovering from a significant economic decline characterized by hyperinflation and political chaos, with GDP growth driven by stronger performance in the mining and agricultural sectors. The country possesses rich natural resources, including substantial mineral reserves, and has a highly educated population, although challenges such as political uncertainty and low foreign investment persist. Moving forward, Zimbabwe presents an investment opportunity for 'first-mover investors' within a transitioning economic landscape marked by improved macroeconomic fundamentals.