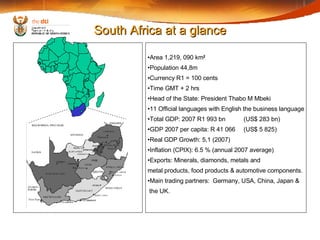

This document provides an overview of South Africa's economy and investment environment. It notes that South Africa has a highly developed economy and infrastructure, and is the largest economy in Africa. Key sectors for investment include mining, tourism, manufacturing, agro-processing, and financial services. The country has competitive costs and a skilled workforce. The economy is expected to grow steadily in the coming years, supported by public and private investment.

![the dti Call Centre: 0861 843 384 the dti Switchboard: +27 12 394 0000 Investment Promotion: +27 12 394 1333/1339 Website: www.thedti.gov.za E-mail: [email_address] Postal Address: Private Bag X 84 Pretoria 0001 South Africa the dti’s Contact Details](https://image.slidesharecdn.com/iqbal-minnesota-1216844947285004-8/85/Why-South-Africa-16-320.jpg)

![Week 9 slides growth&business cycle [core]](https://cdn.slidesharecdn.com/ss_thumbnails/week9slidesgrowthbusinesscyclecore-130605145537-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)