Downloaded 100 times

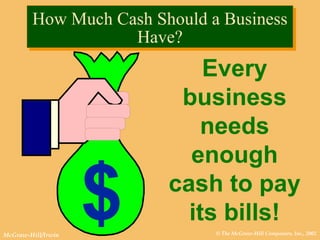

This document discusses various aspects of a company's cash and accounts receivable, including: - How much cash a business needs and how excess cash can be invested temporarily - How financial assets like cash, accounts receivable, and short-term investments are valued on the balance sheet - Techniques for estimating uncollectible accounts, writing off accounts, and adjusting the allowance for doubtful accounts based on accounts receivable aging