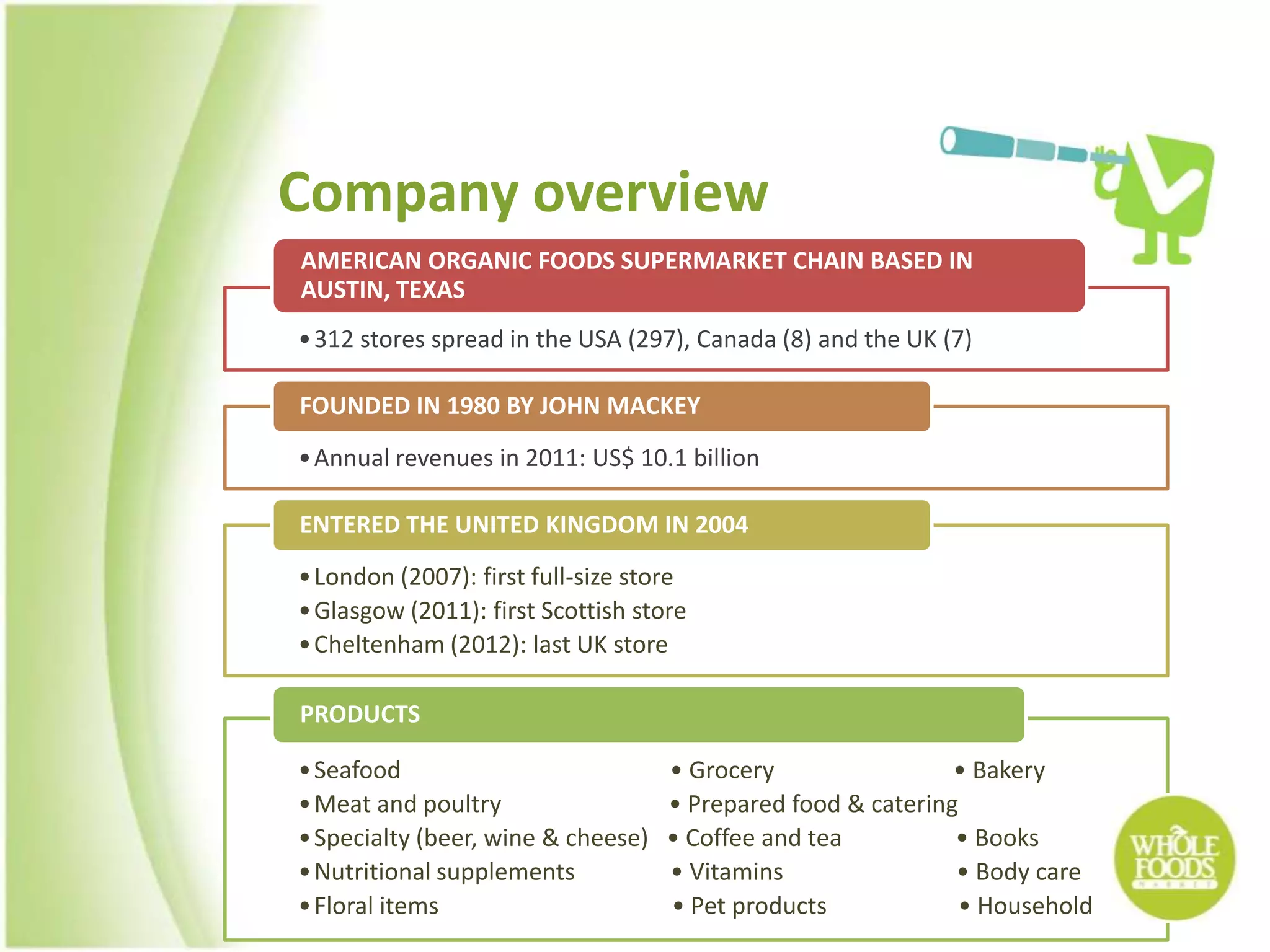

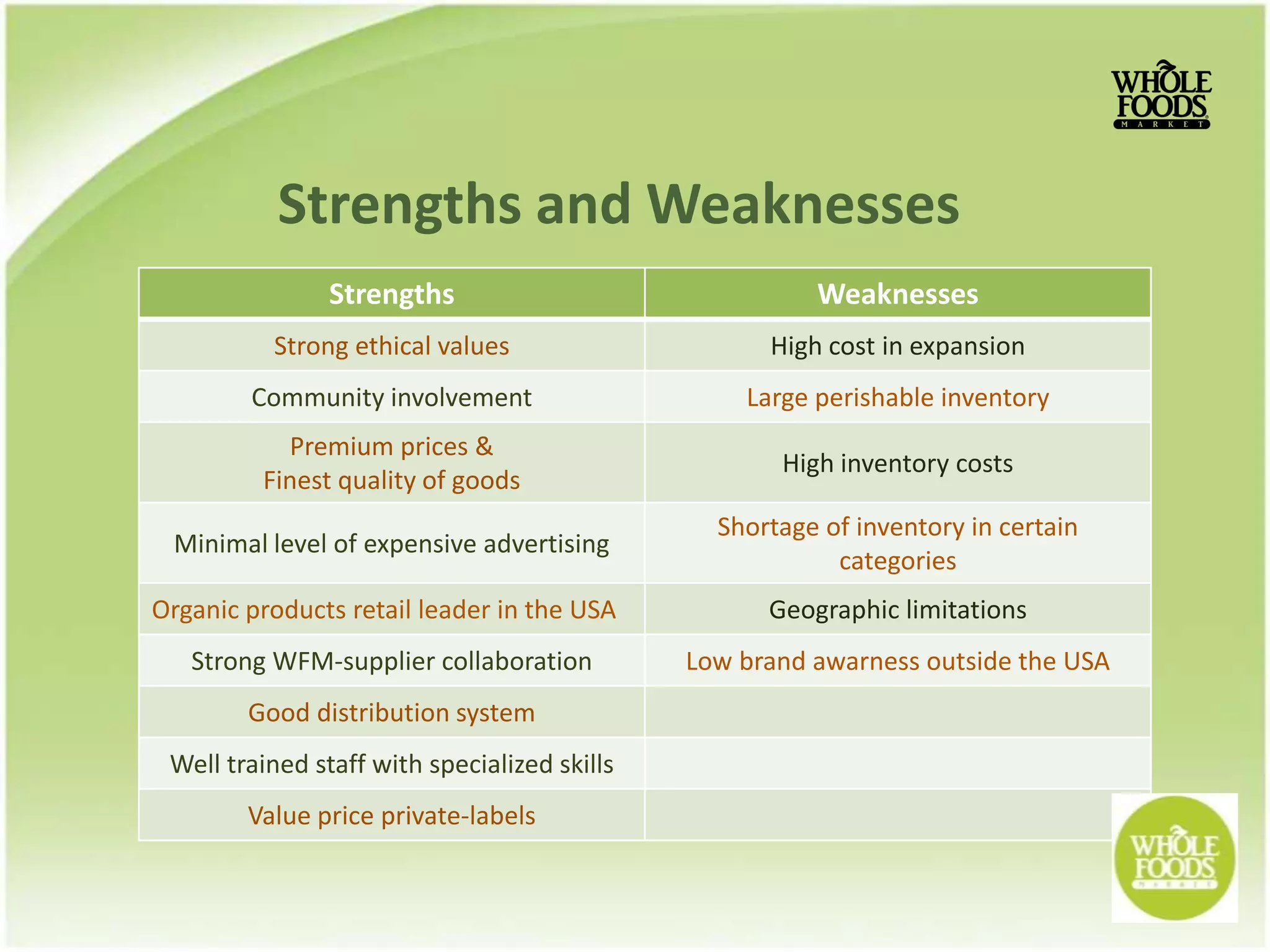

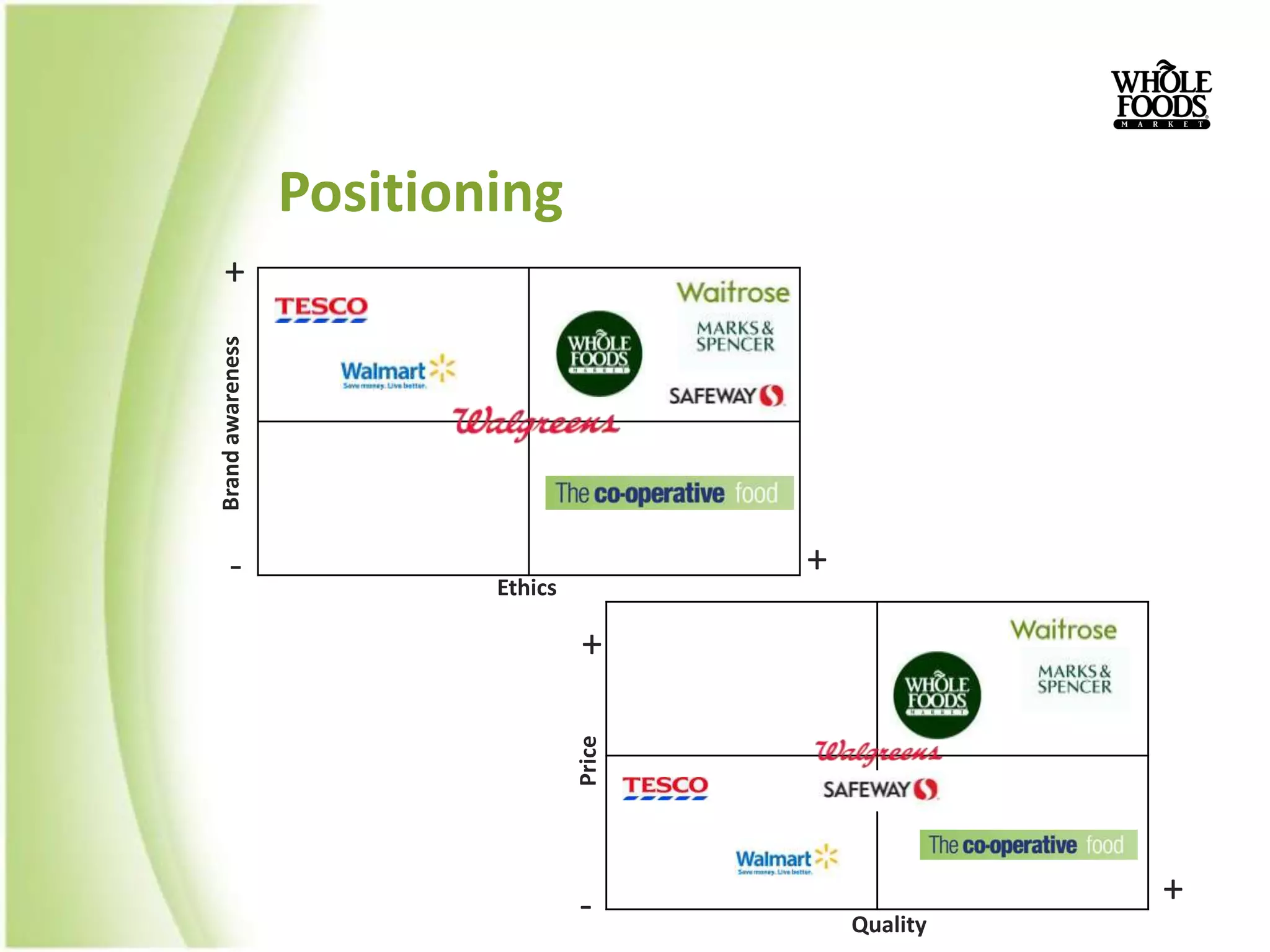

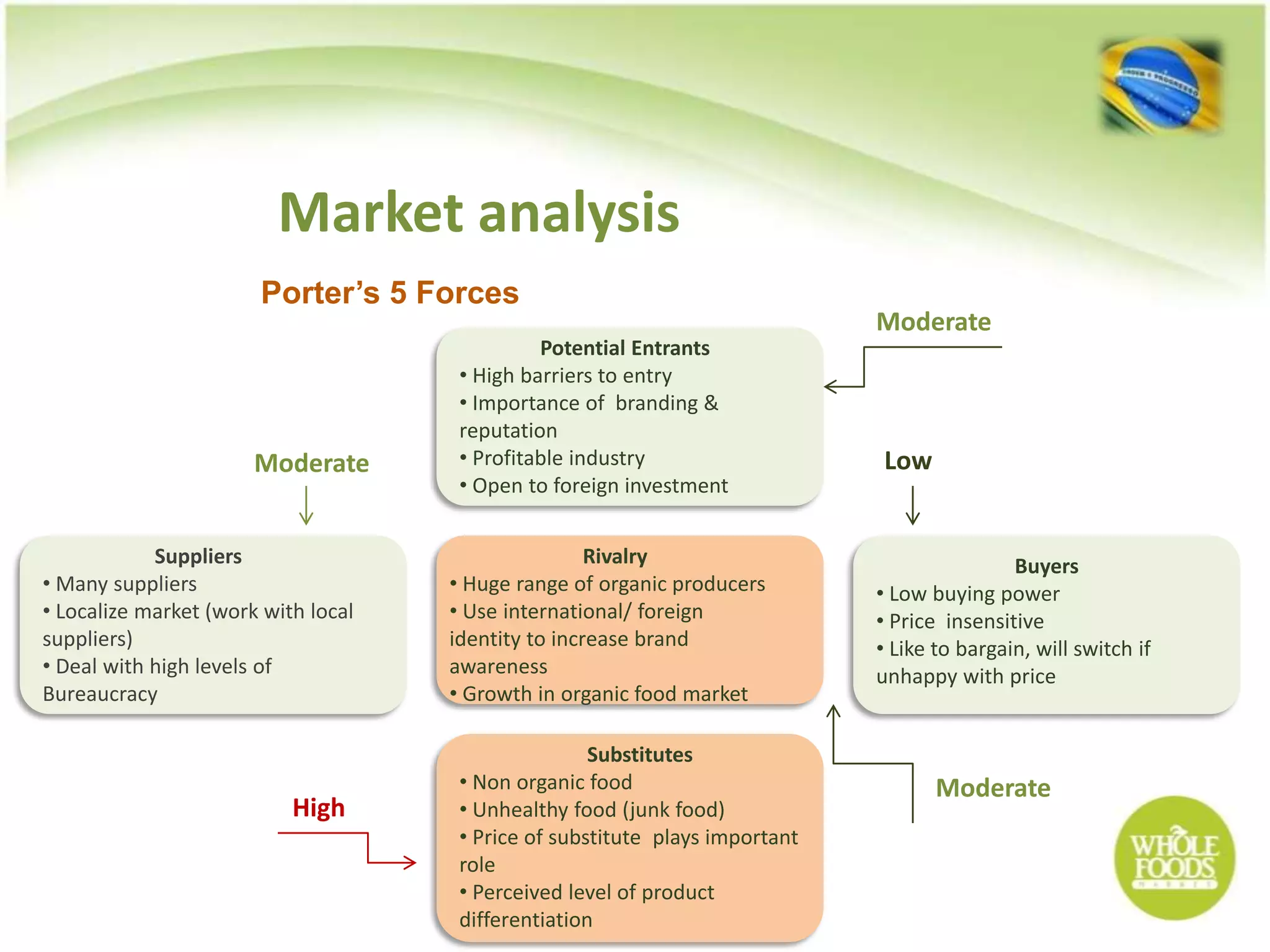

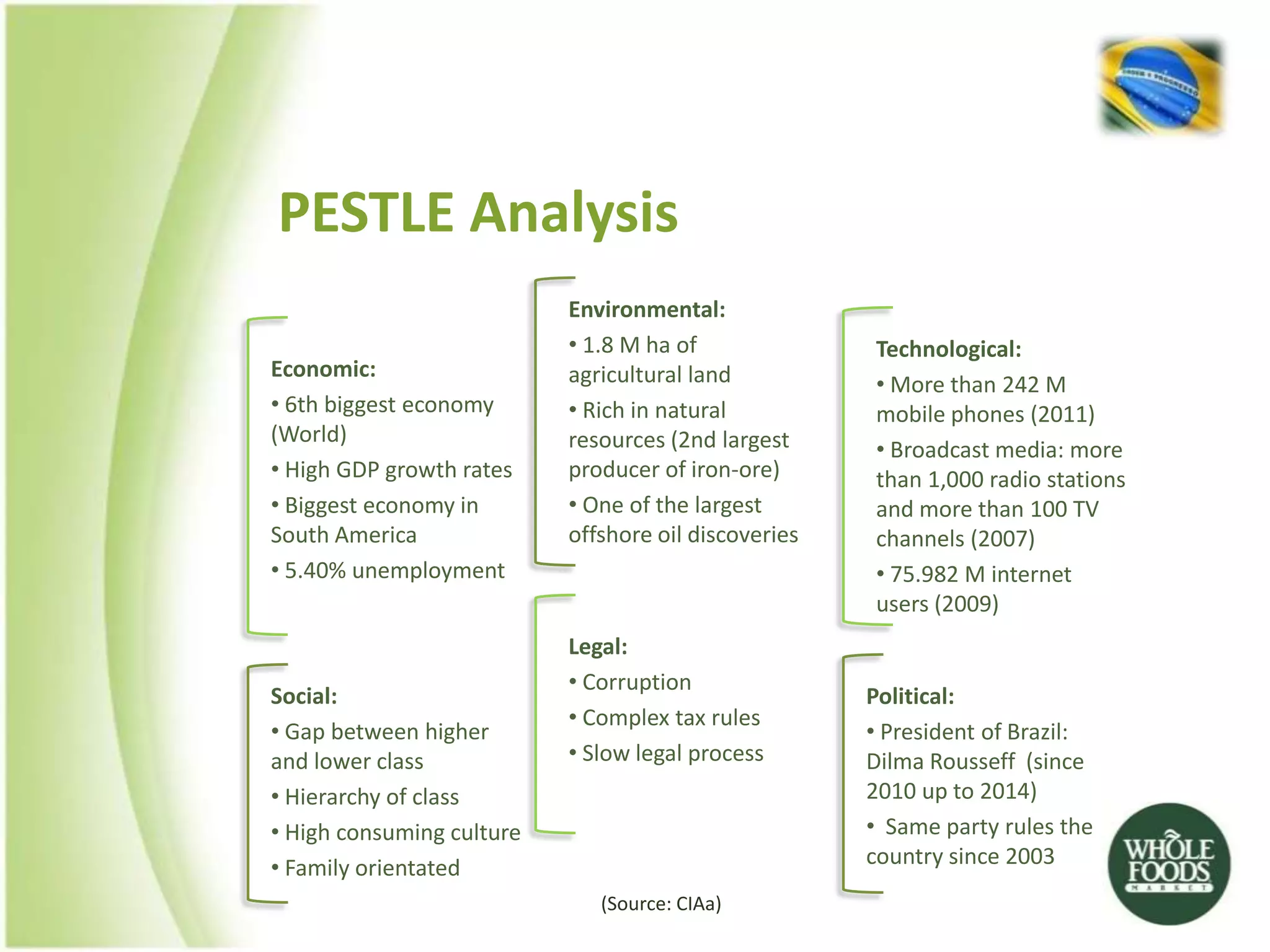

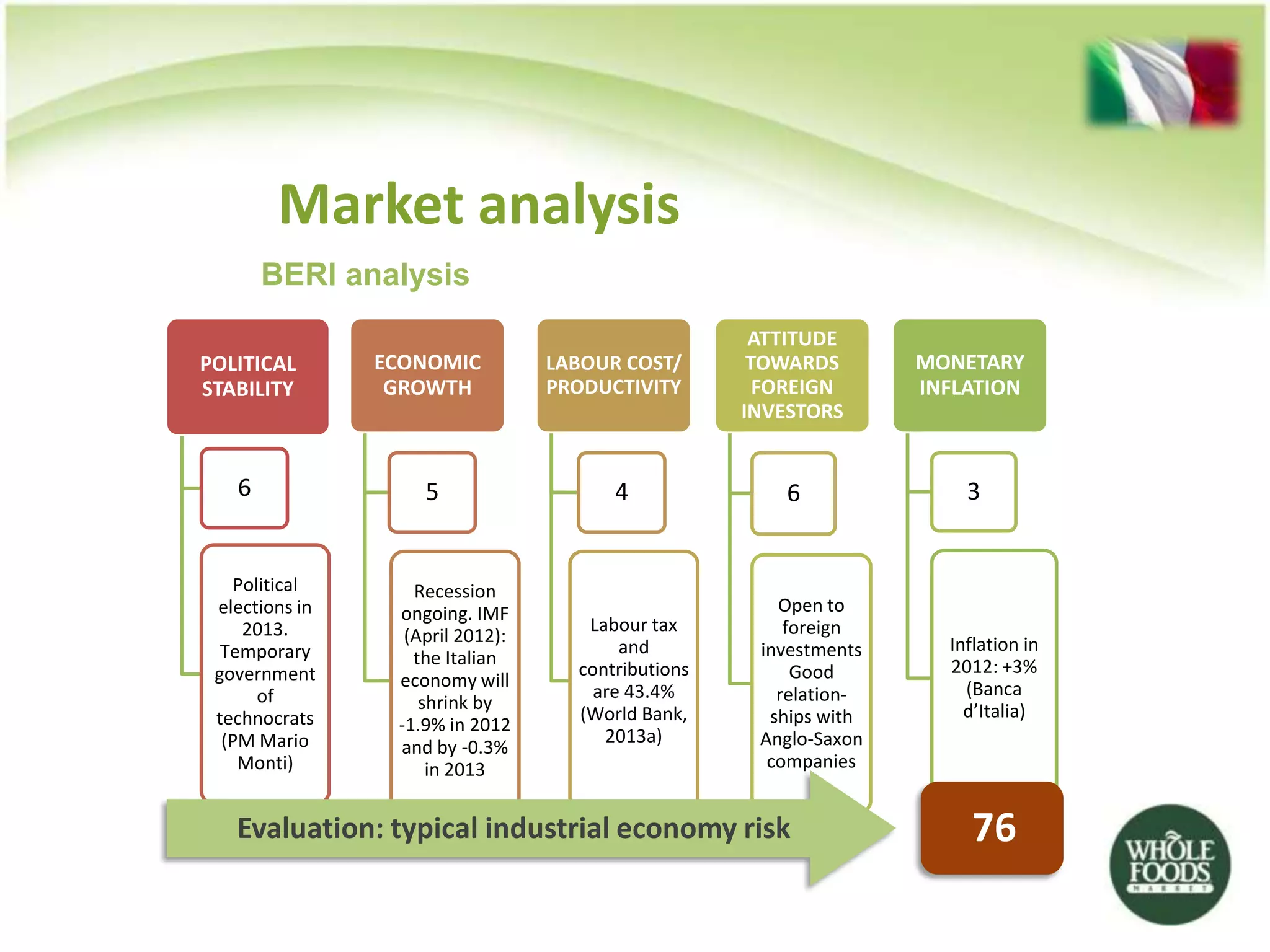

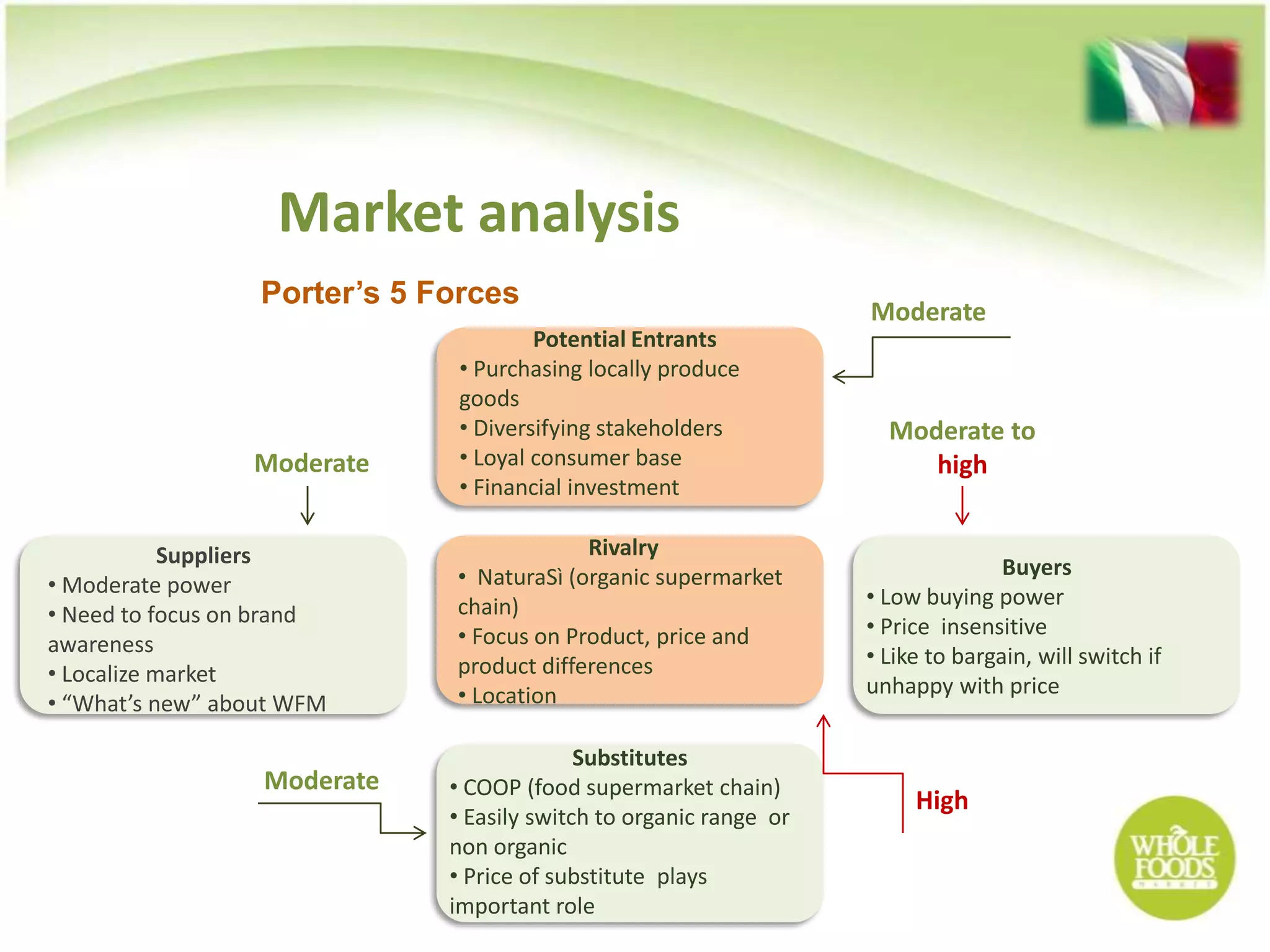

Whole Foods Market plans to expand into Brazil and Italy. It currently operates 312 stores across the US, Canada, and UK, with annual revenues of $10.1 billion in 2011. Whole Foods is known for its high quality organic and natural products. To enter Brazil, Whole Foods will leverage the country's large agricultural industry and growing organic food market. A market analysis shows Brazil has low political risk and high economic growth, though inflation is a challenge. Competition in organic retail is moderate, and suppliers are plentiful.