This document discusses OpenWay Group's digital payment platform called WAY4. It provides the following key points:

1) WAY4 is a digital payment platform that aims to help payment companies embrace challenges in the digital era by providing payment software solutions.

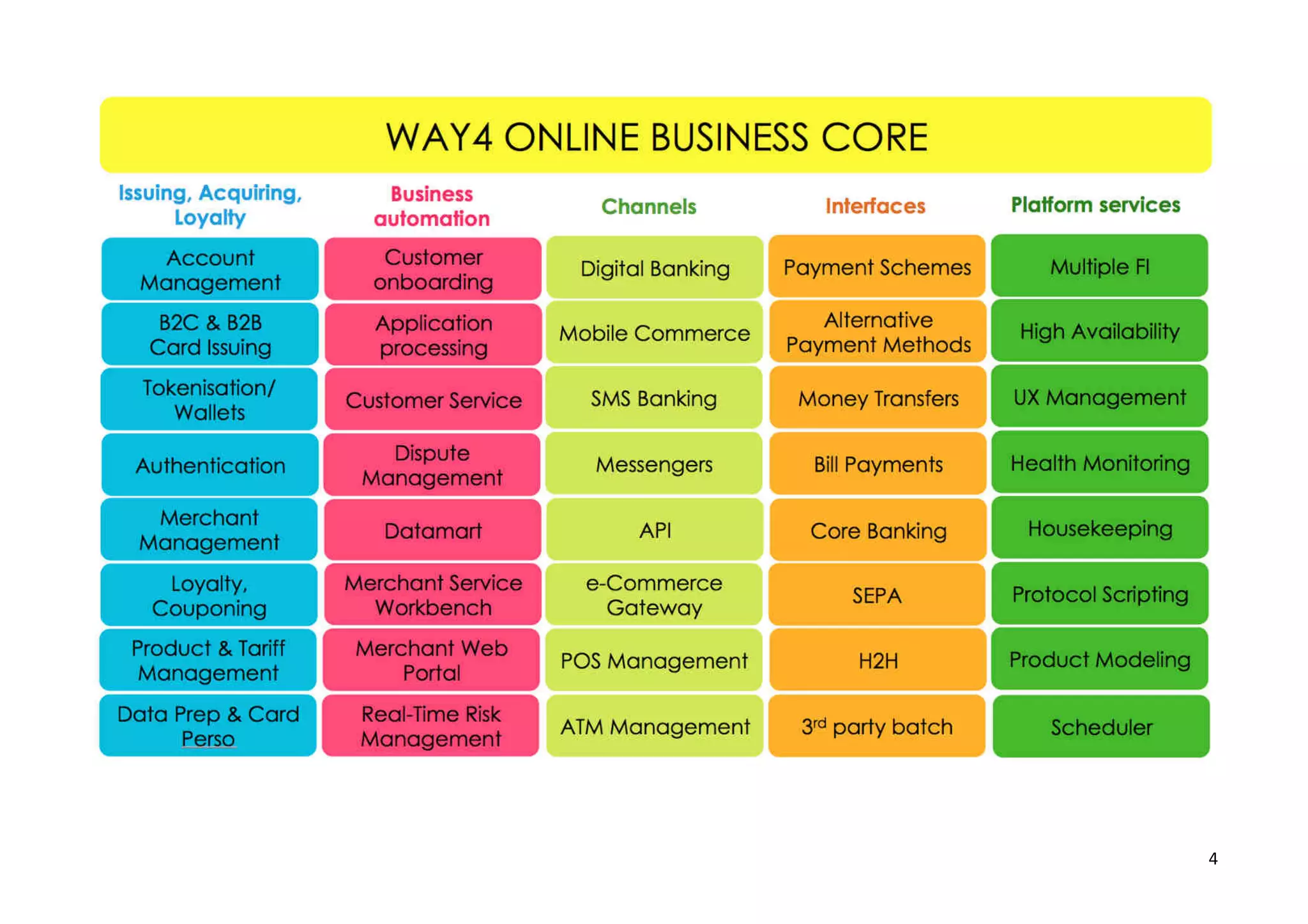

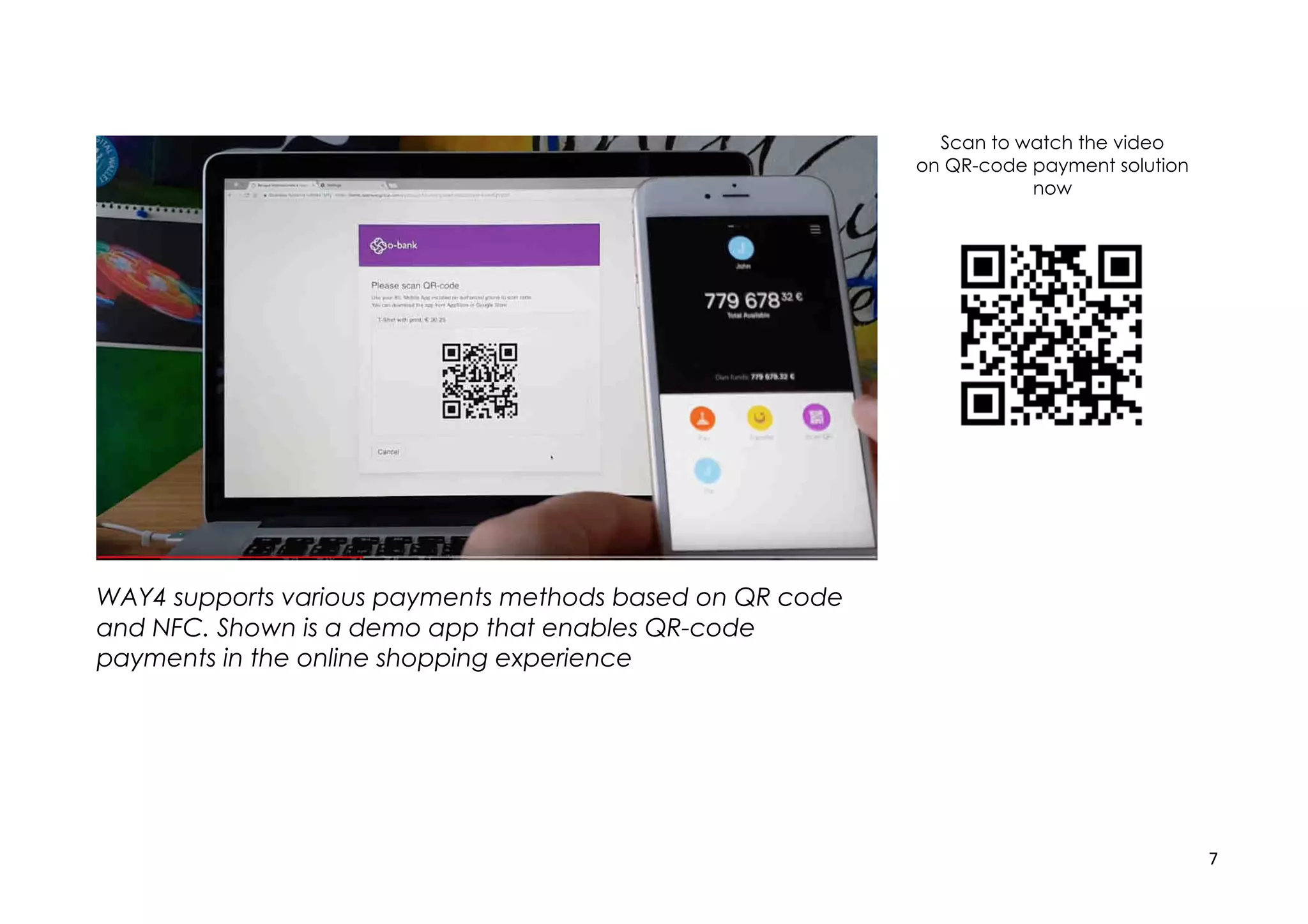

2) It offers digital wallet, card issuing, acquiring, switching and other payment products and services in a unified and flexible way to ensure secure customer experience.

3) OpenWay is a leading global provider of digital payment software, ranked number 1 by Gartner and Ovum, and its WAY4 platform is used by major banks and payment processors worldwide.