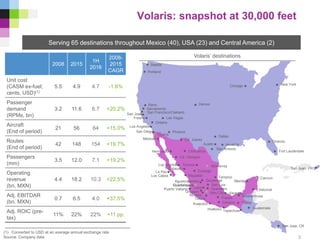

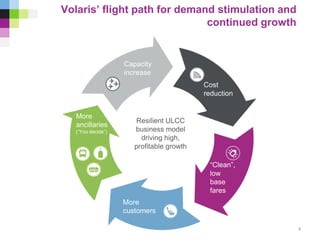

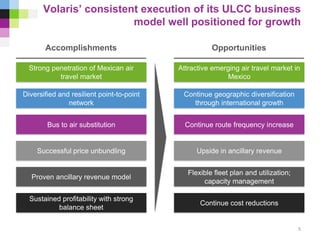

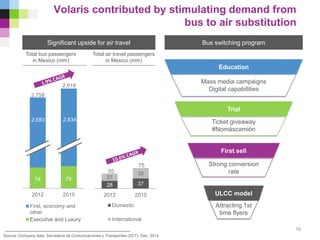

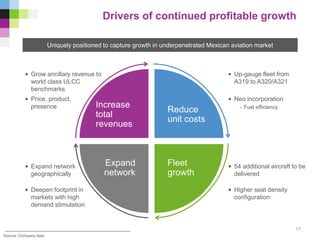

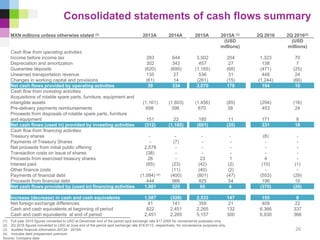

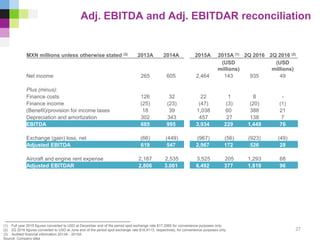

Volaris is the leading ultra-low-cost airline in Mexico, serving 65 destinations in Mexico, the United States, and Central America. It has a young and fuel efficient fleet of 64 aircraft that enable it to have the lowest unit costs in the Americas. Volaris has experienced strong growth over the past years through capacity increases, network expansion, and stimulating demand through low base fares and ancillary revenues. It is well positioned for continued profitable growth by further reducing costs, expanding its fleet and network, and increasing total revenues.