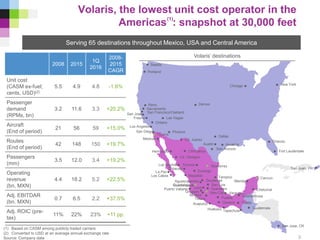

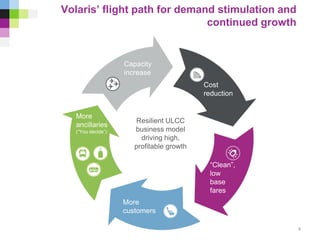

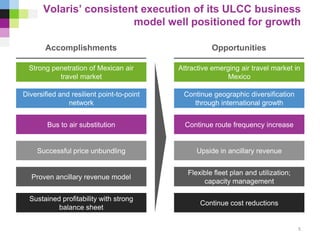

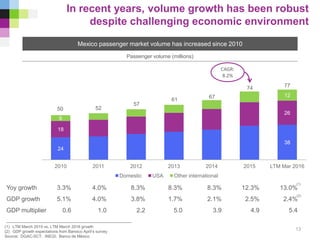

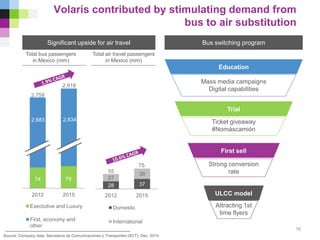

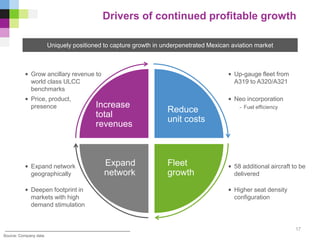

Volaris is the leading ultra-low-cost airline in Mexico, Central America, and the United States. It has a fleet of 59 aircraft serving 65 destinations. Volaris has achieved a compound annual growth rate of 15% in aircraft and 19.7% in routes since 2008 through consistent execution of its low-cost business model. Key to its success has been industry-leading low unit costs, revenue from ancillary fees, and network expansion into new markets.