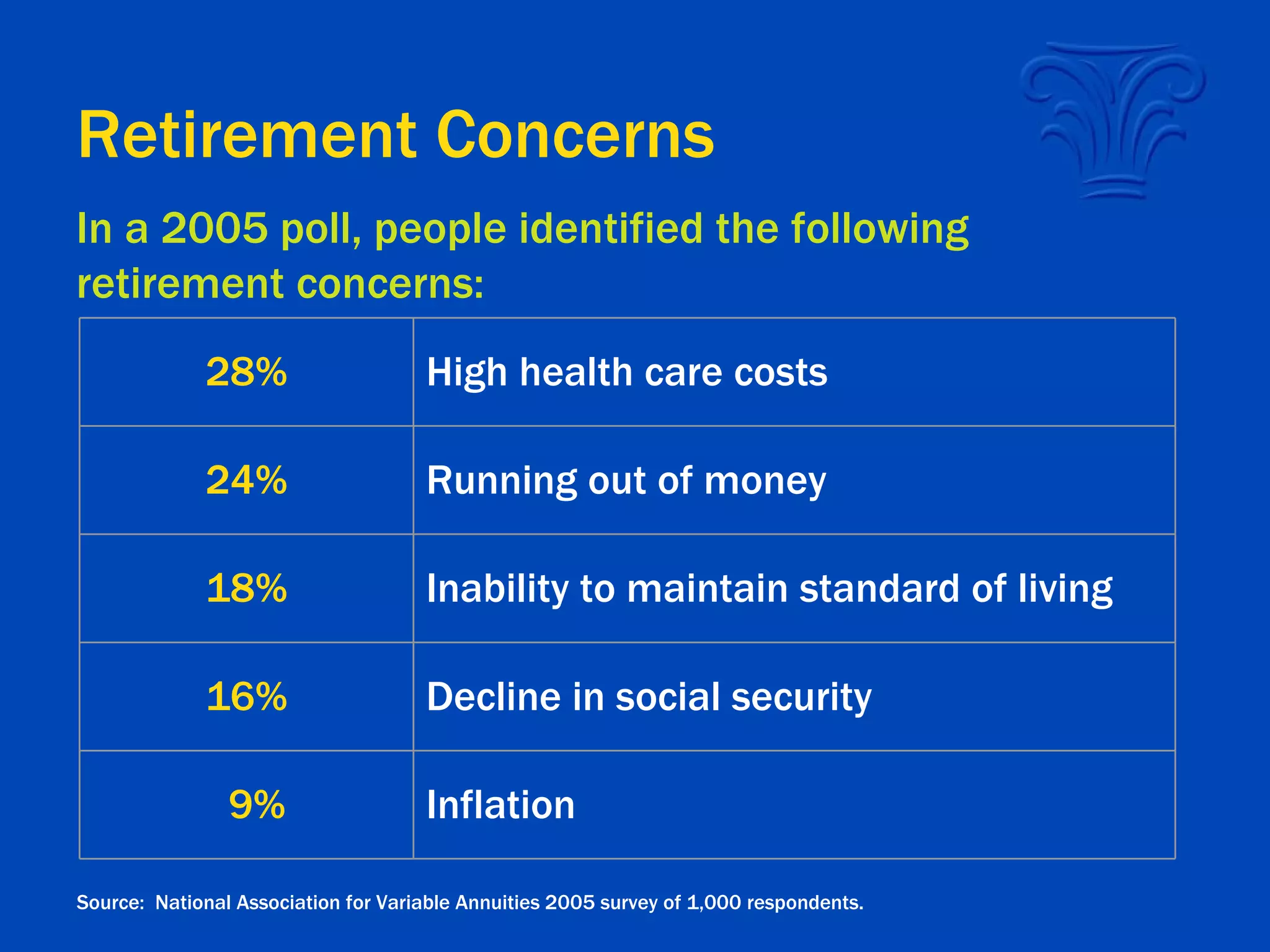

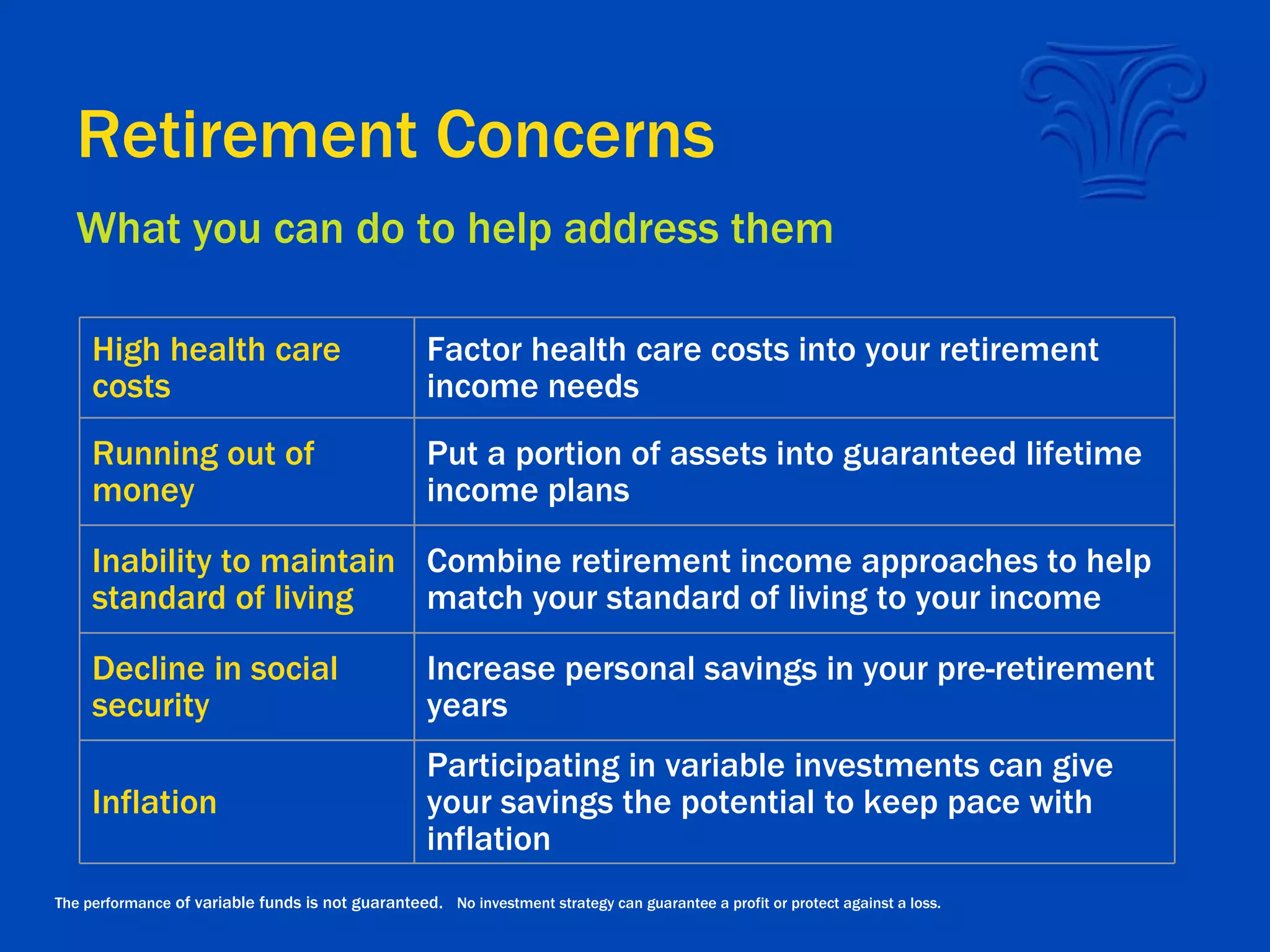

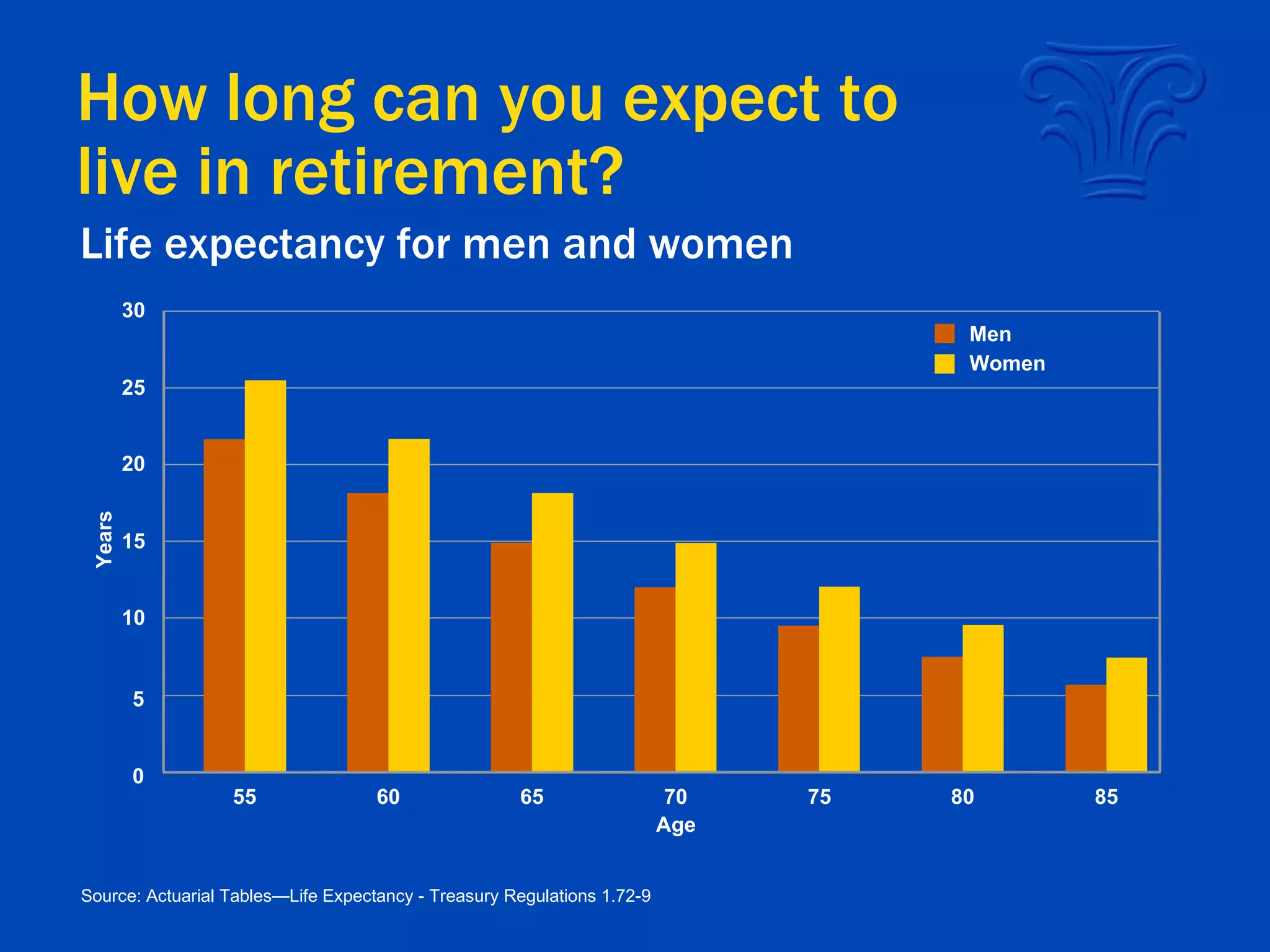

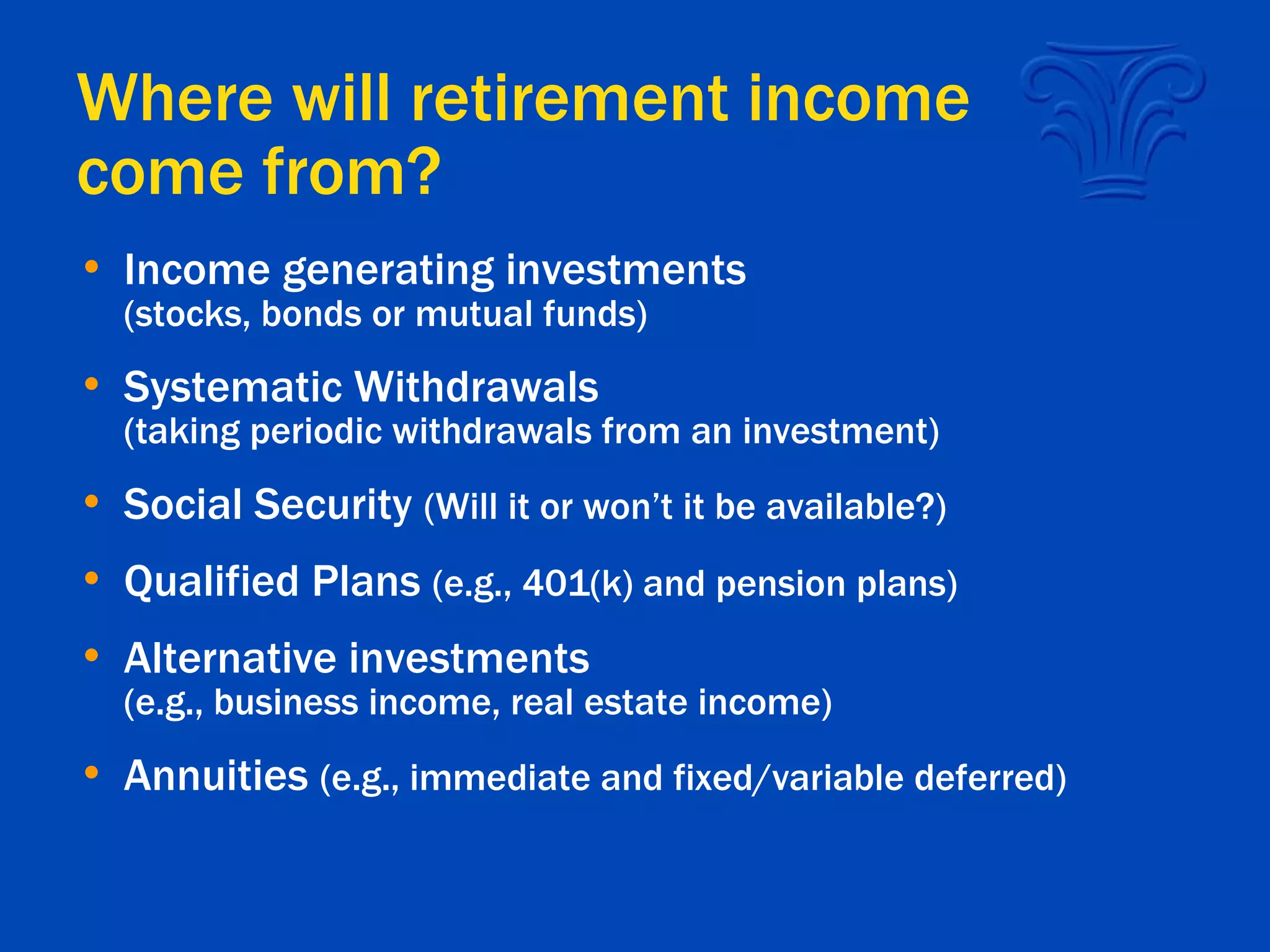

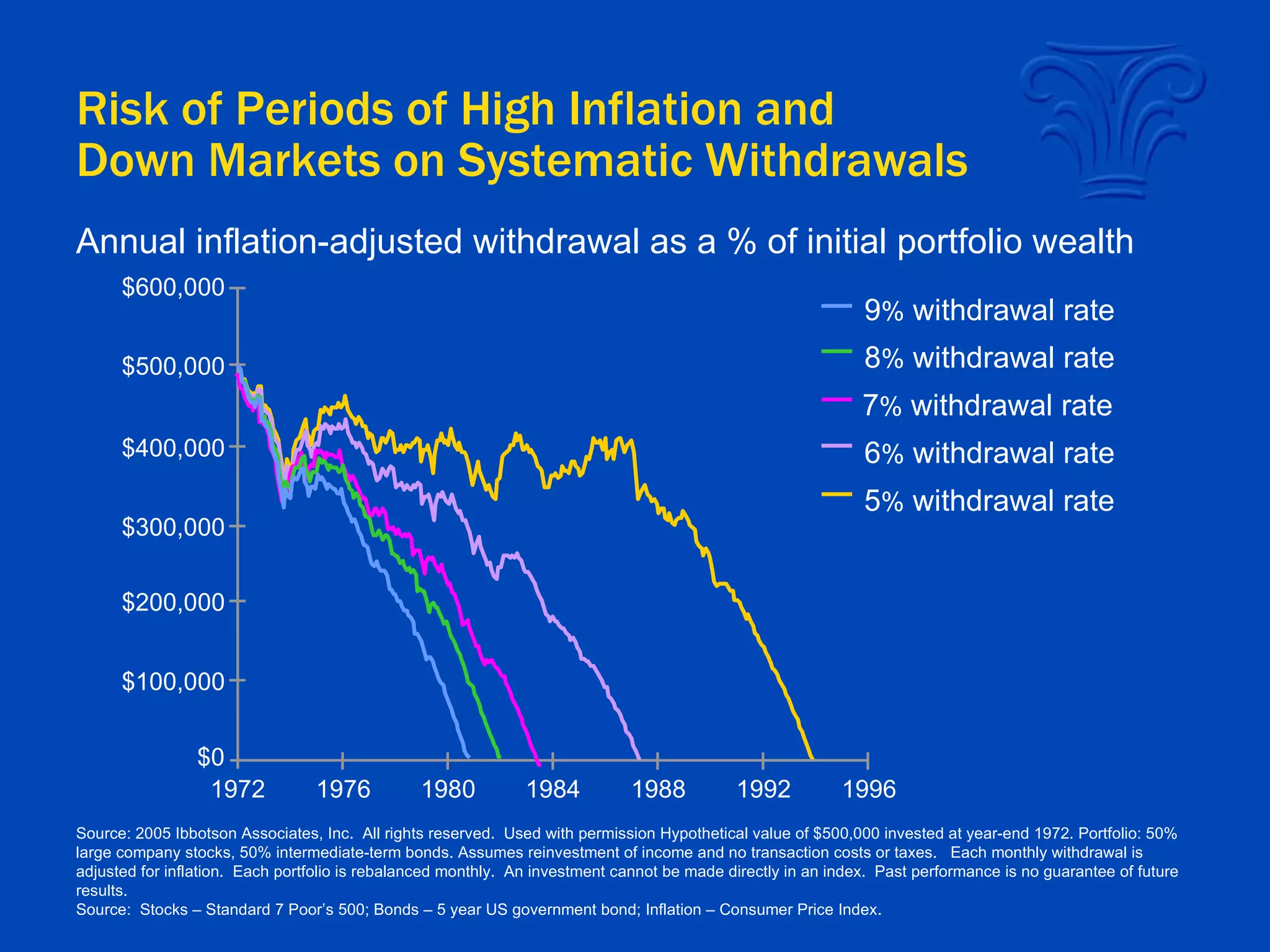

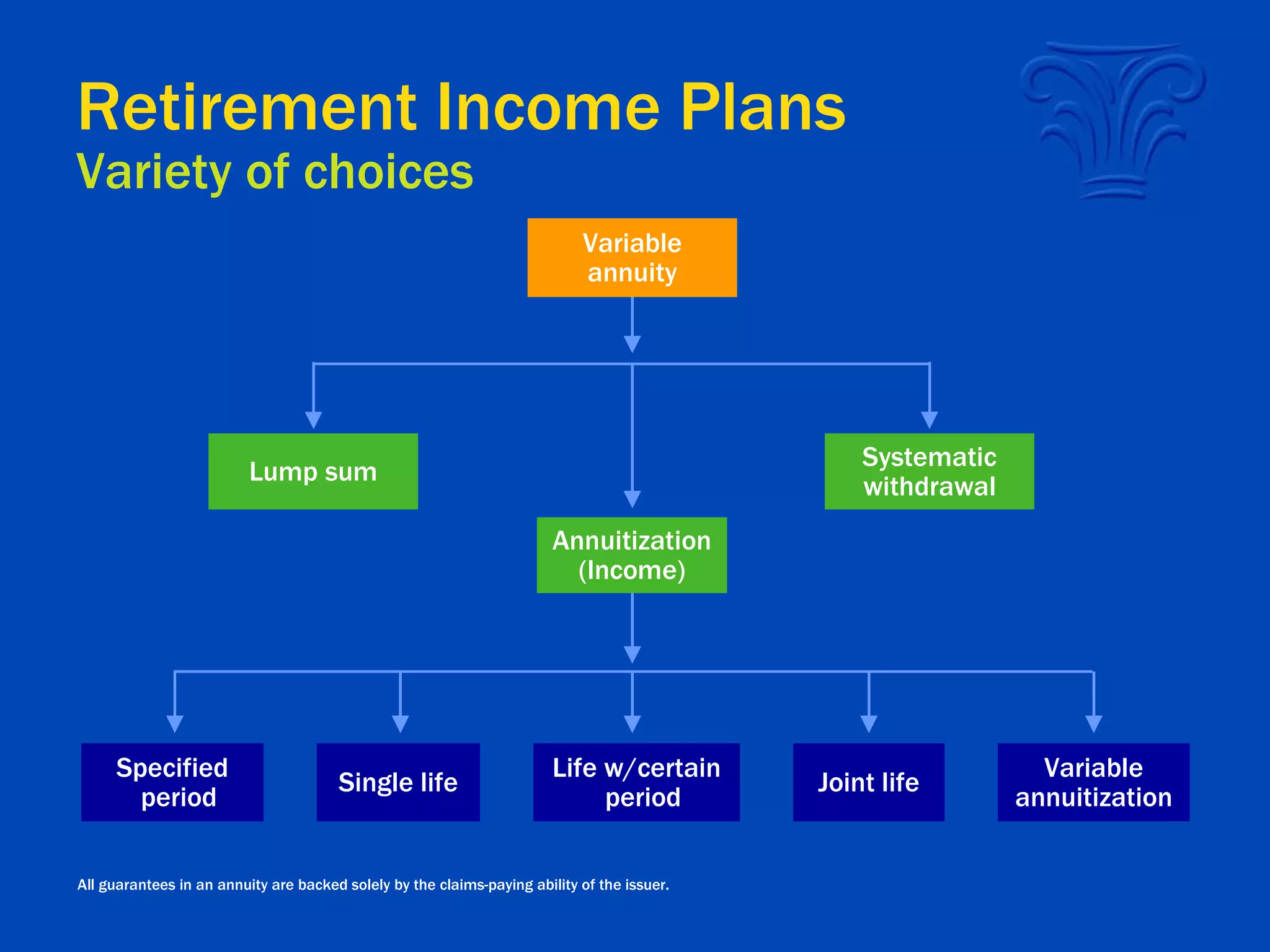

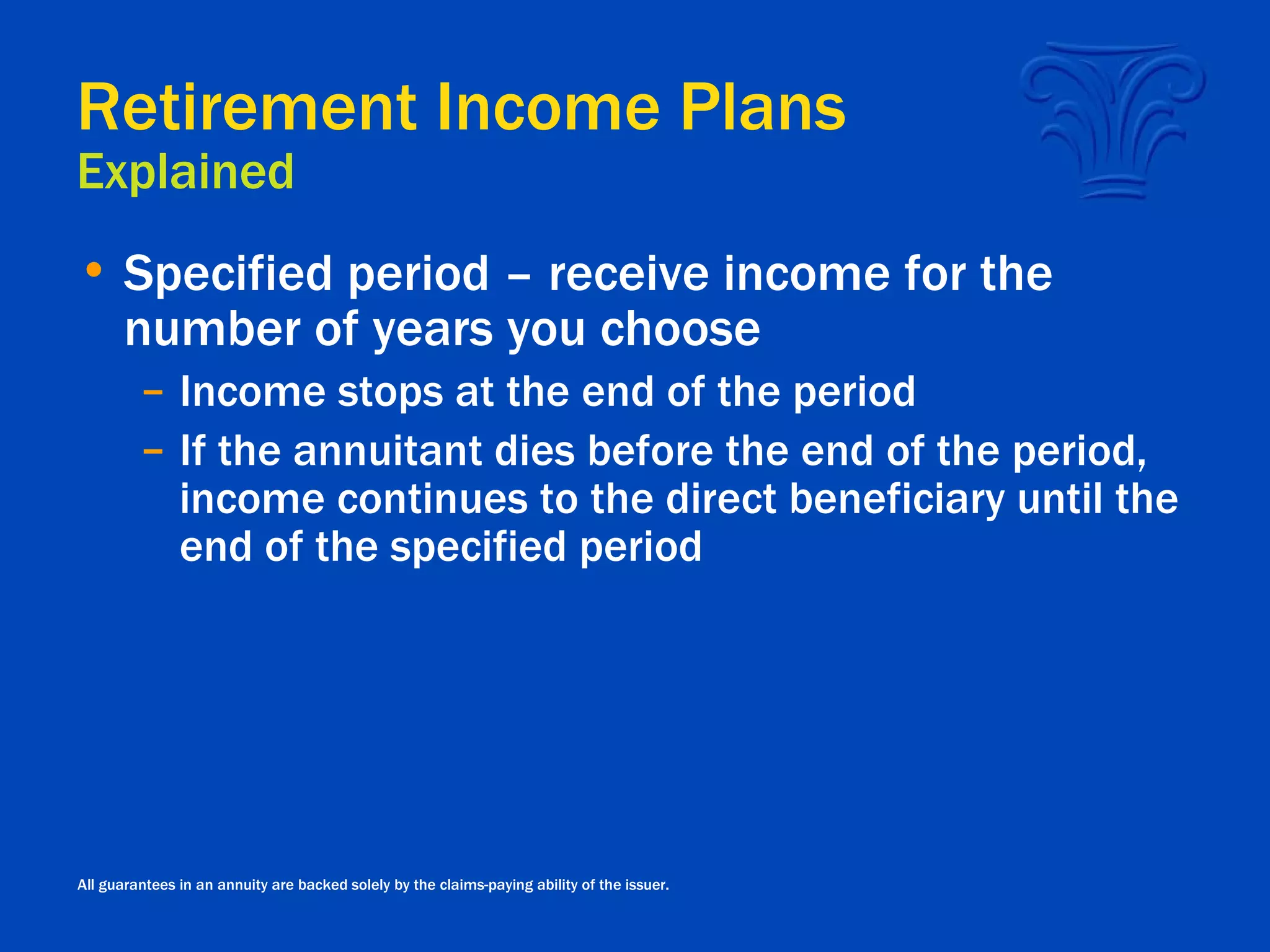

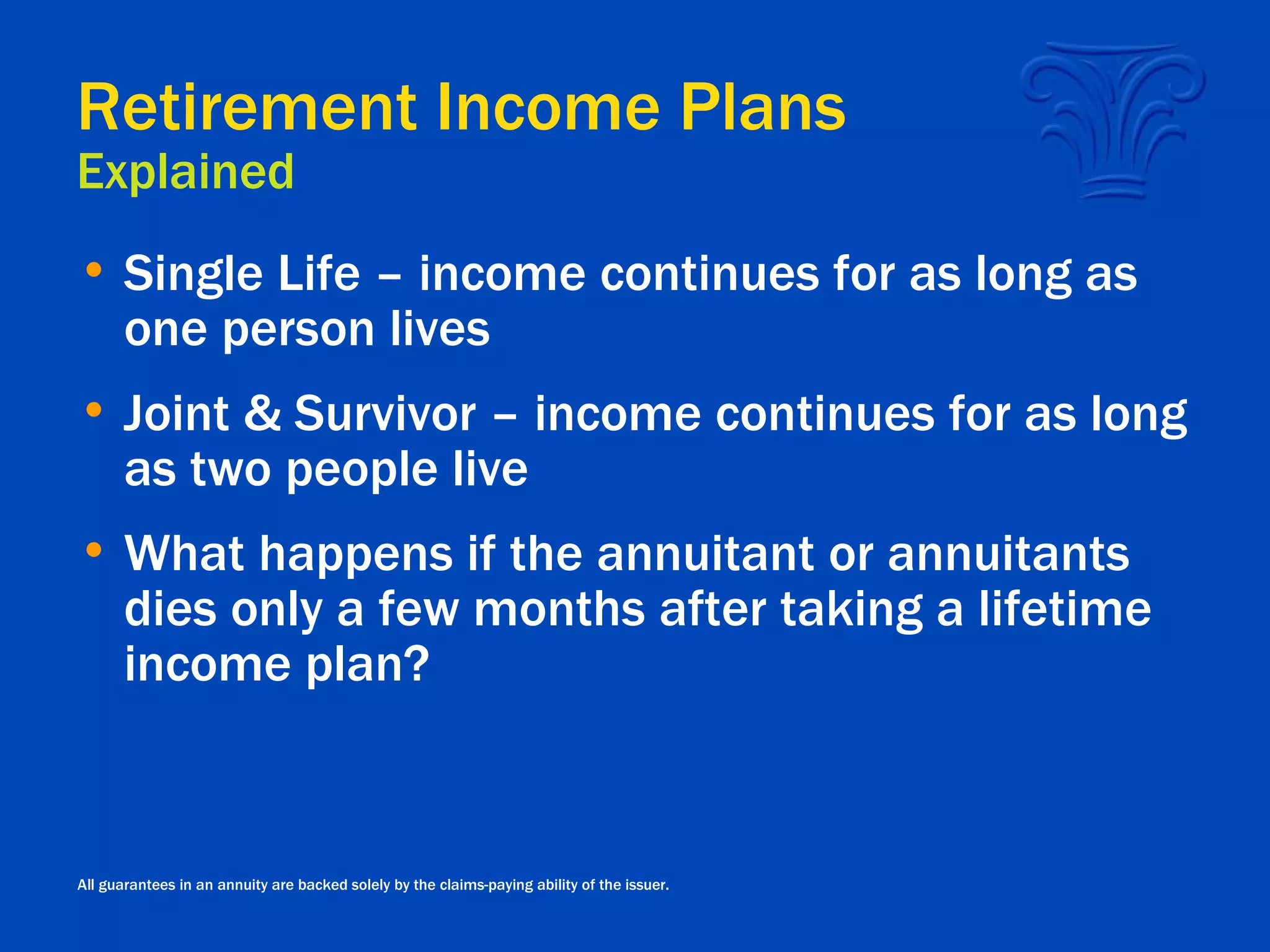

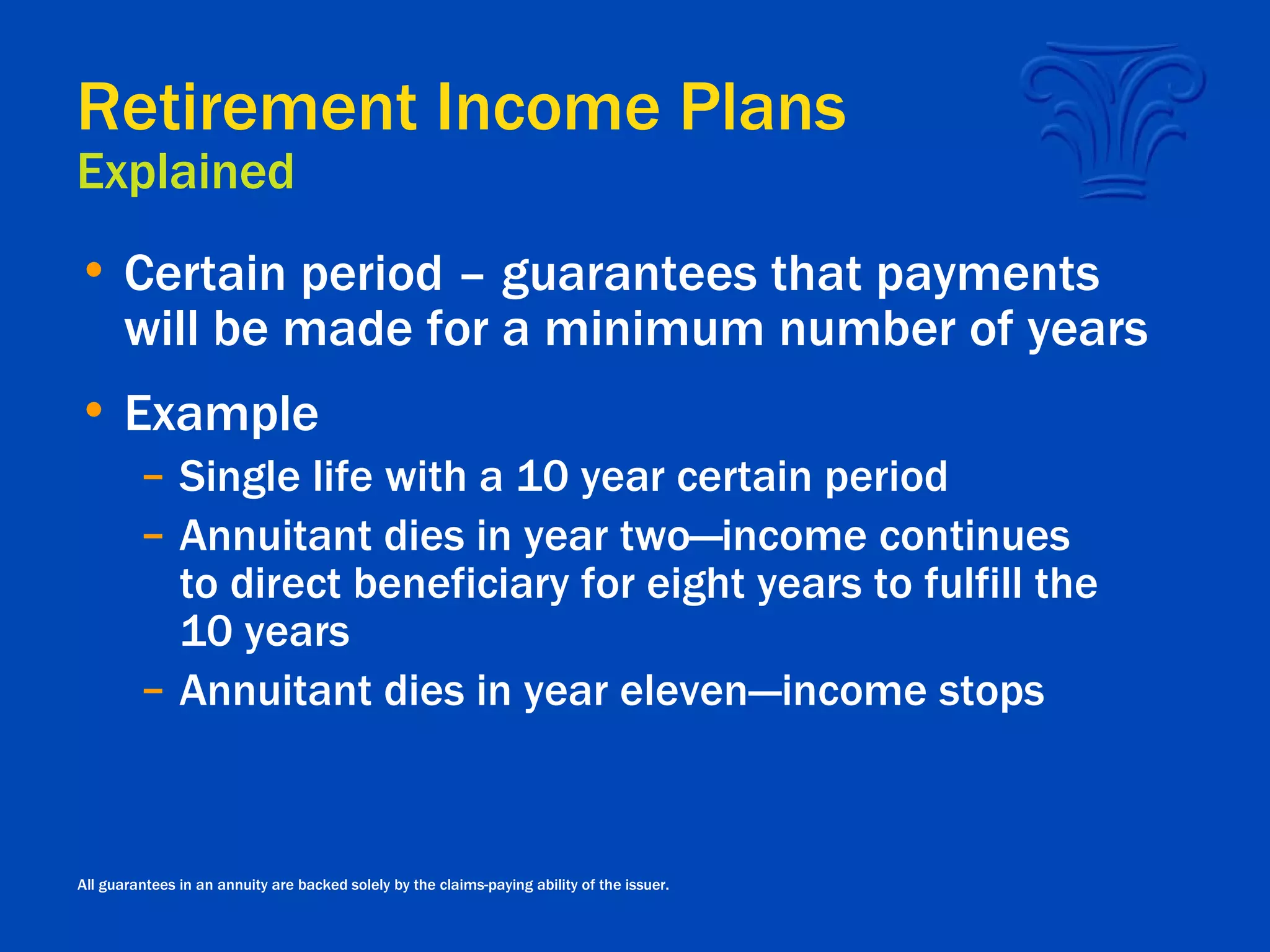

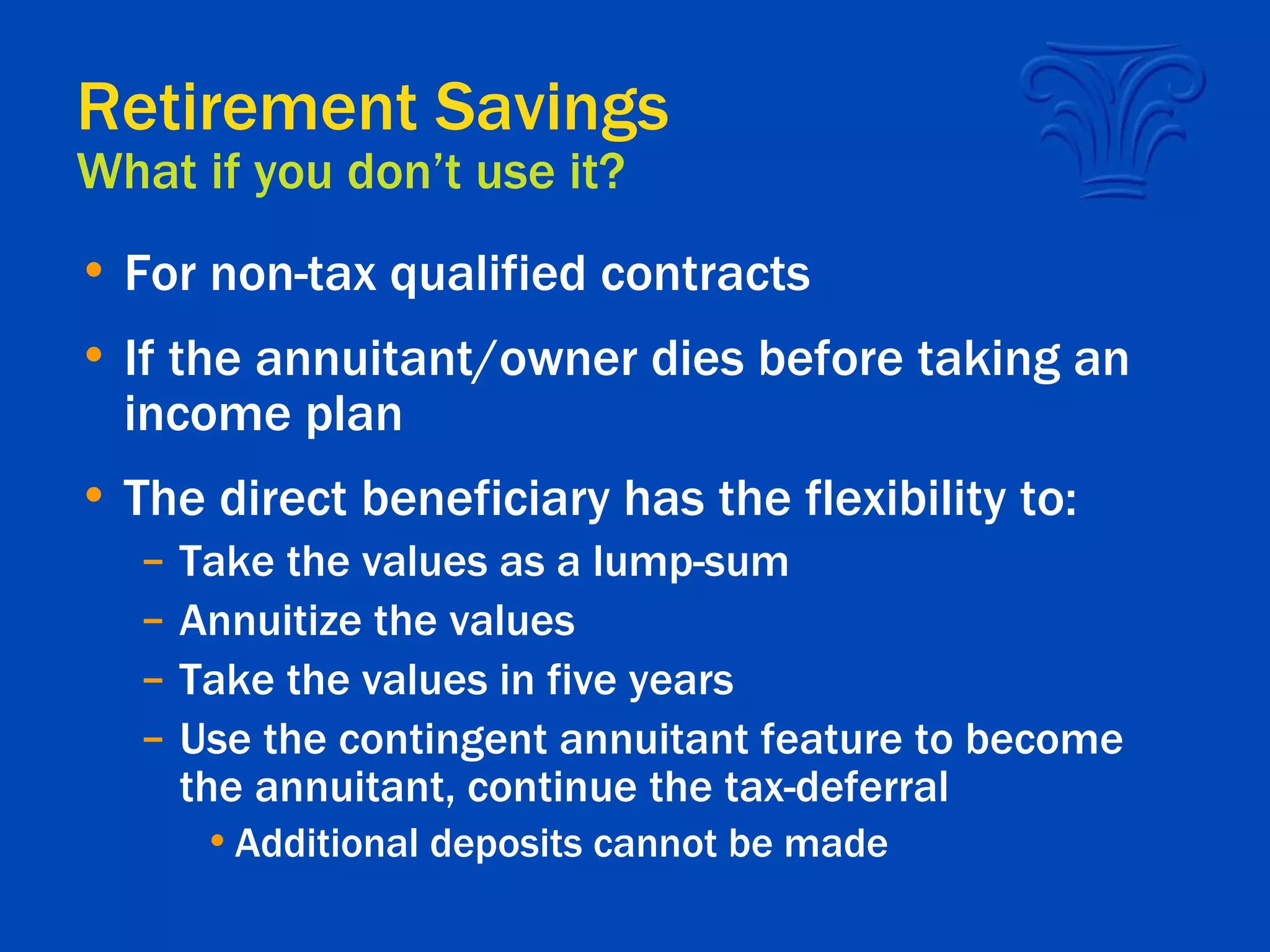

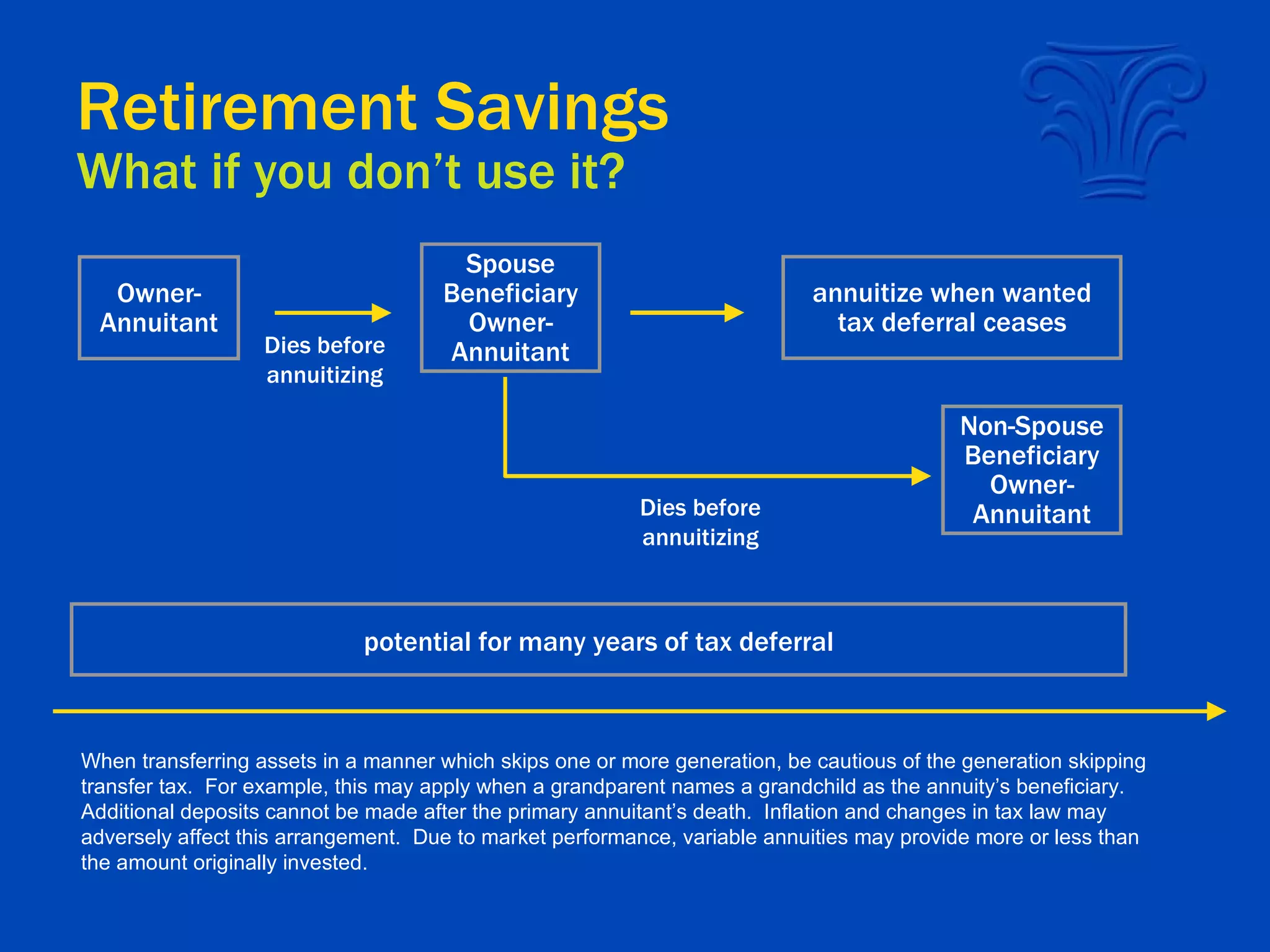

The document discusses preparing for retirement with a variable annuity product called the Northwestern Mutual Select Variable Annuity. It outlines key features like tax-deferred growth, guaranteed death benefits, and options for guaranteed retirement income. Concerns around running out of money, health costs, and inflation in retirement are addressed through the annuity's features and investment options.

![Benefit gold brochure[1]](https://cdn.slidesharecdn.com/ss_thumbnails/benefitgoldbrochure1-130524121432-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)