Downloaded 12 times

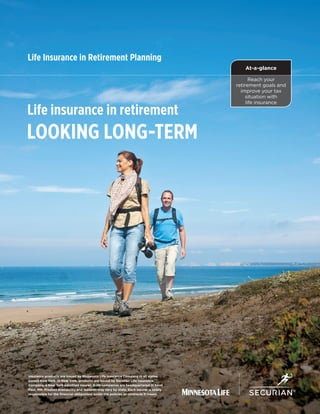

This document discusses how life insurance can help achieve retirement goals by providing tax advantages. It notes that life insurance builds cash value on a tax-deferred basis that can supplement retirement through tax-favored loans and withdrawals. The document provides an example of a couple using policy withdrawals in retirement to lower their taxes while funding special expenses. It highlights the benefits of leveraging a life insurance policy for retirement through its death benefit, tax-deferred growth, and potential access to cash values.

![Slirp 4 9 09 Final[1]](https://cdn.slidesharecdn.com/ss_thumbnails/slirp4909final1-12667828759198-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)