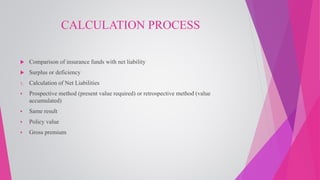

The document outlines the valuation of insurance liabilities and the determination of surplus, focusing on methods to assess solvency and compute net liabilities. It discusses the calculation of insurance funds, the sources of surplus, and the distinction between surplus and profit, as well as methods for distributing surplus among policyholders. Key aspects include the bases of valuation, calculation methods, and various bonus distribution strategies.