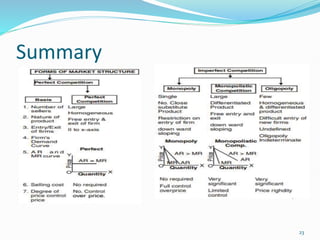

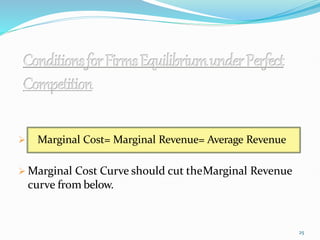

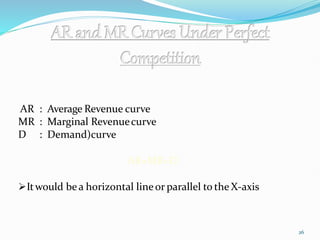

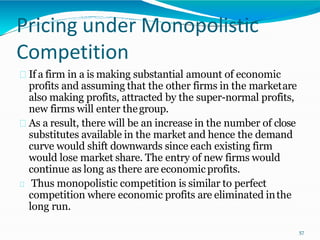

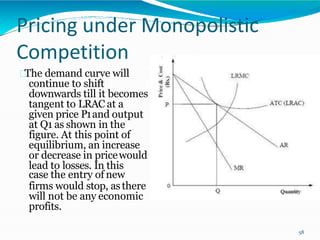

This document discusses different market structures:

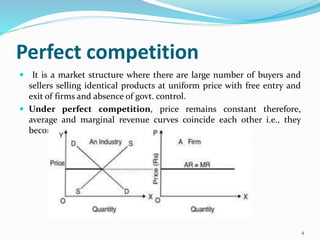

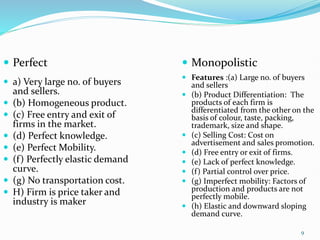

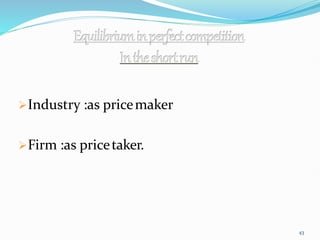

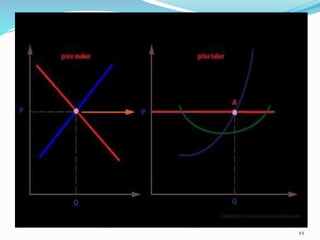

1) Perfect competition is defined as a market with many small firms, homogeneous products, free entry and exit, and price-taking behavior. Firms under perfect competition are price takers.

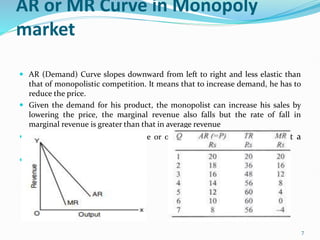

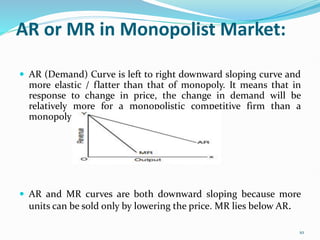

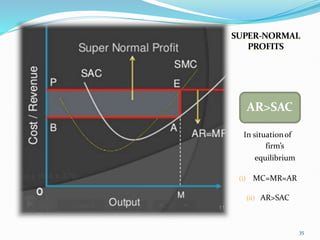

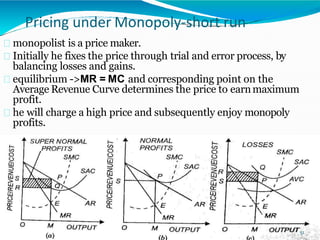

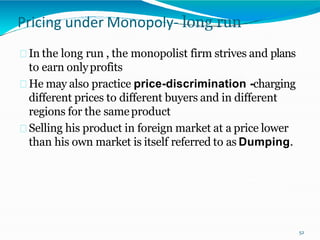

2) Monopoly is a market with a single seller and many buyers where there are barriers to entry. A monopoly has control over price and faces a downward-sloping demand curve.

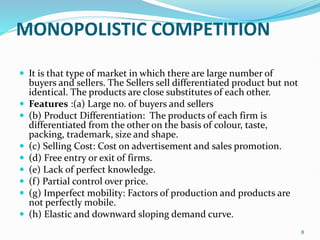

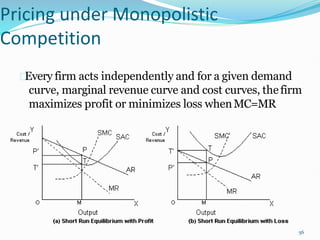

3) Monopolistic competition is like perfect competition but with differentiated products. Firms have some control over price and face downward-sloping demand curves. Entry and exit of firms is relatively easy.

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)