Definition

Cost Accounting isthat branch of accounting

which deals with presenting and providing

accounting information to the Cost in a

systematic way so that it can perform its Cost

functions of planning, controlling and decision-

making in an effective and efficient manner.

3.

Definition

According to theInstitute of Cost Accountants (IMA): “Cost

accounting is a profession that involves partnering in Cost

decision making, devising planning and performance Cost

systems, and providing expertise in financial reporting and

control to assist Cost in the formulation and implementation of

an organization's strategy

4.

According to AmericanAccounting

Association, Cost Accounting is “the application

of appropriate techniques and concepts in

processing historical and projected economic data

of an entity to assist Cost in establishing plans for

reasonable economic objectives and in the making

of rational decisions with a view towards these

objectives”.

5.

Nature of CostAccounting

Analysis & Interpretation of data

Future-oriented

Serves as a yardstick

6.

Scope of CostAccounting

Financial Accounting: Financial Accounting provides

historical information useful for future planning and financial

forecasting

Cost Accounting: It provides various techniques of costing

which are used in the process of planning and decision-making.

Forecasting and budgeting: Cost Accounting exercises the

tool of forecasting and budgeting in the process of planning,

controlling and decision-making

Tax accounting and tax planning: the analysis of implication

of tax provisions on future projects comes under Cost

accounting.

7.

Contd..

Internal Control& Audit: Cost Accounting highly depends

on internal control system existing in the organization to

identify the weaker sections of the organization.

Cost Control Procedures: include inventory control, cost

control, budgetary control, variance analysis etc.

Financial Analysis and Interpretation: Various financial

analysis techniques such as Ratio Analysis, Fund Flow

Analysis, Trend analysis are used to analyze and interpret

financial data.

8.

Contd…

Reporting toCost: The Cost Accountant is required to

submit reports to the Cost as per their requirements.

Office Services: Cost Accountant is expected to maintain

and control office routines and procedures like filing,

copying, communicating, data processing etc.

Statistical Tools: Various statistical tools like graphs,

charts, diagrams are used in the process of planning,

controlling and decision-making.

9.

Objectives of CostAccounting

Analysis and Interpretation of Financial Statements:

Planning and policy-making

Decision-Making

Controlling

Coordinating

Communicating

Helps in evaluating the efficiency and effectiveness of policies

10.

Tools & Techniquesof Cost Accounting

Financial Statement Analysis

Fund Flow Analysis

Cash Flow Analysis

Budgetary Control

Standard Costing

Marginal Costing

Cost Reporting

Statistical and Operations Research techniques

Limitations of CostAccounting

Reliance on accounting data

Based on historical data

Highly Expensive

Complicated application

Lack of objectivity

13.

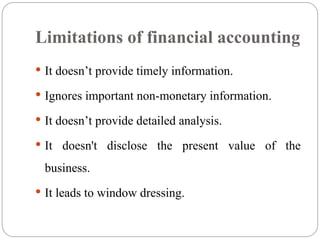

Limitations of financialaccounting

It doesn’t provide timely information.

Ignores important non-monetary information.

It doesn’t provide detailed analysis.

It doesn't disclose the present value of the

business.

It leads to window dressing.

14.

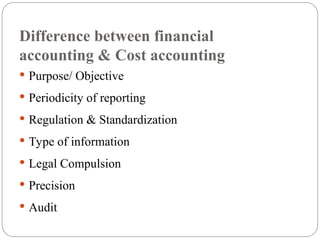

Difference between financial

accounting& Cost accounting

Purpose/ Objective

Periodicity of reporting

Regulation & Standardization

Type of information

Legal Compulsion

Precision

Audit

15.

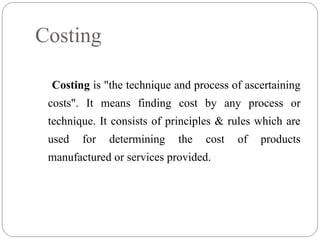

Costing is "thetechnique and process of ascertaining

costs". It means finding cost by any process or

technique. It consists of principles & rules which are

used for determining the cost of products

manufactured or services provided.

Costing

16.

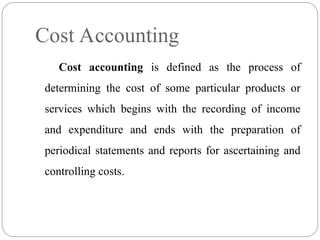

Cost accounting isdefined as the process of

determining the cost of some particular products or

services which begins with the recording of income

and expenditure and ends with the preparation of

periodical statements and reports for ascertaining and

controlling costs.

Cost Accounting

17.

Cost accountancy hasbeen defined as "the

application of costing and cost accounting principles,

methods and techniques to the science, art and practice

of cost control and the ascertainment of profitability.

Cost Accountancy

18.

Determination ofselling price

Controlling cost

Providing information for decision-making

Ascertainment of cost & profit of individualized basis

Implementing a system of cost control

Facilitates reliability

To organize cost reduction programmes

Objectives of Cost Accounting

19.

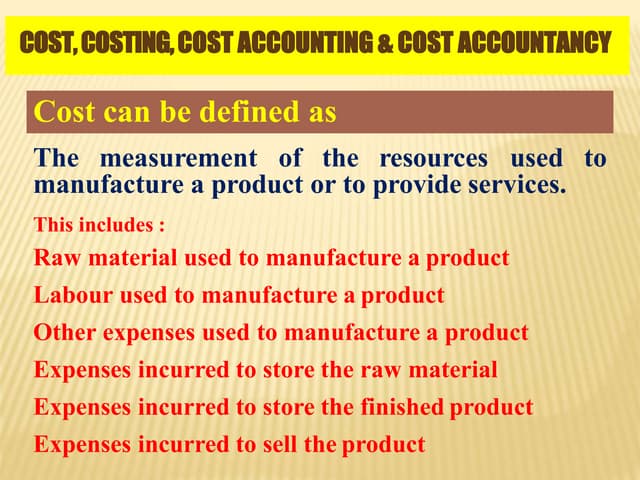

The literal meaningof cost is the amount paid or required in

payment for a purchase or for the production or upkeep of

something. It is the amount of resources given up in

exchange for some goods or services.

Cost is generally measured in monetary terms.

Cost is always ascertained with reference to some object

such as material, labor, job, process etc.

Cost - Meaning

20.

Cost control:It is an act of controlling or regulating the

cost within the standards laid down, through the application

of various management tools & techniques such as standard

costing, budgetary control etc.

Cost reduction: It is concerned with achieving real &

permanent reduction on the unit cost of goods or services

rendered without impairing their quality or suitability.

Terminologies

21.

Cost audit:It involves checking up the arithmetical accuracy

of cost accounts & verifying whether the principles laid down

have been followed or not.

Cost unit: It is unit of product, service or a combination of

them in relation to which costs are ascertained & expressed.

For e.g. in steel & cement industry cost unit is ‘tonne’ while in

transportation services the unit may be passenger-km.

22.

Cost Centre:It is defined as a location, person or item of

equipment for which costs may be ascertained & used for the

purpose of control. A cost centre is charged with all the costs

that relate to it e.g. if cost centre is a machine, it will be

charged with the costs of installation, power, depreciation etc.

Cost Object: It may be defined anything for which the cost

can be measured separately. It may be a product, service,

activity or process etc.

23.

Cost Driver:It is a factor that influences cost. A change in the

cost driver will led to a change in the total cost of a related cost

object. Examples of cost drivers are: number of units

produced, number of customers served, number of

advertisements, number of sales personnel, number of products

produced etc. Any change made in any of the cost drivers will

cause a change in the total cost.

24.

Role of costaccountant

Cost accountants play a crucial role in organizations by focusing

on the financial aspects of production, operations, and overall

business activities. Their primary responsibility is to manage

and analyze costs associated with the production of goods or

services. Here are some key roles and responsibilities of cost

accountants:

25.

Cost Analysis:

Analyzingand evaluating the costs associated with various

business processes, such as production, distribution, and

administration.

Identifying areas where costs can be reduced or efficiencies

improved.

Cost Planning:

Developing and implementing cost-effective strategies and

budgets to guide the organization in achieving its financial goals.

Assisting in the preparation of financial plans and forecasts.

26.

Cost Control:

Monitoringactual costs against budgeted costs and analyzing

variances.

Implementing cost control measures to ensure that the

organization operates within budgetary constraints.

Product Costing:

Calculating the cost of producing specific goods or services,

including direct and indirect costs.

Helping management make informed decisions about pricing,

production, and product profitability.

27.

Inventory Management:

Managingand controlling inventory costs by implementing

effective inventory valuation methods.

Advising on optimal inventory levels to avoid overstocking or

stockouts.

Decision Support:

Providing financial information and analysis to support

management decisions.

Assisting in the evaluation of alternative courses of action by

considering their financial implications.

28.

Compliance and Reporting:

Ensuringcompliance with accounting standards and

regulations related to cost accounting.

Preparing and presenting cost reports and financial statements

to management and stakeholders.

Continuous Improvement:

Identifying opportunities for process improvements and cost

savings.

Collaborating with other departments to enhance overall

organizational efficiency.

29.

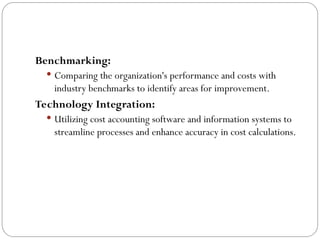

Benchmarking:

Comparing theorganization's performance and costs with

industry benchmarks to identify areas for improvement.

Technology Integration:

Utilizing cost accounting software and information systems to

streamline processes and enhance accuracy in cost calculations.