Download as PDF, PPTX

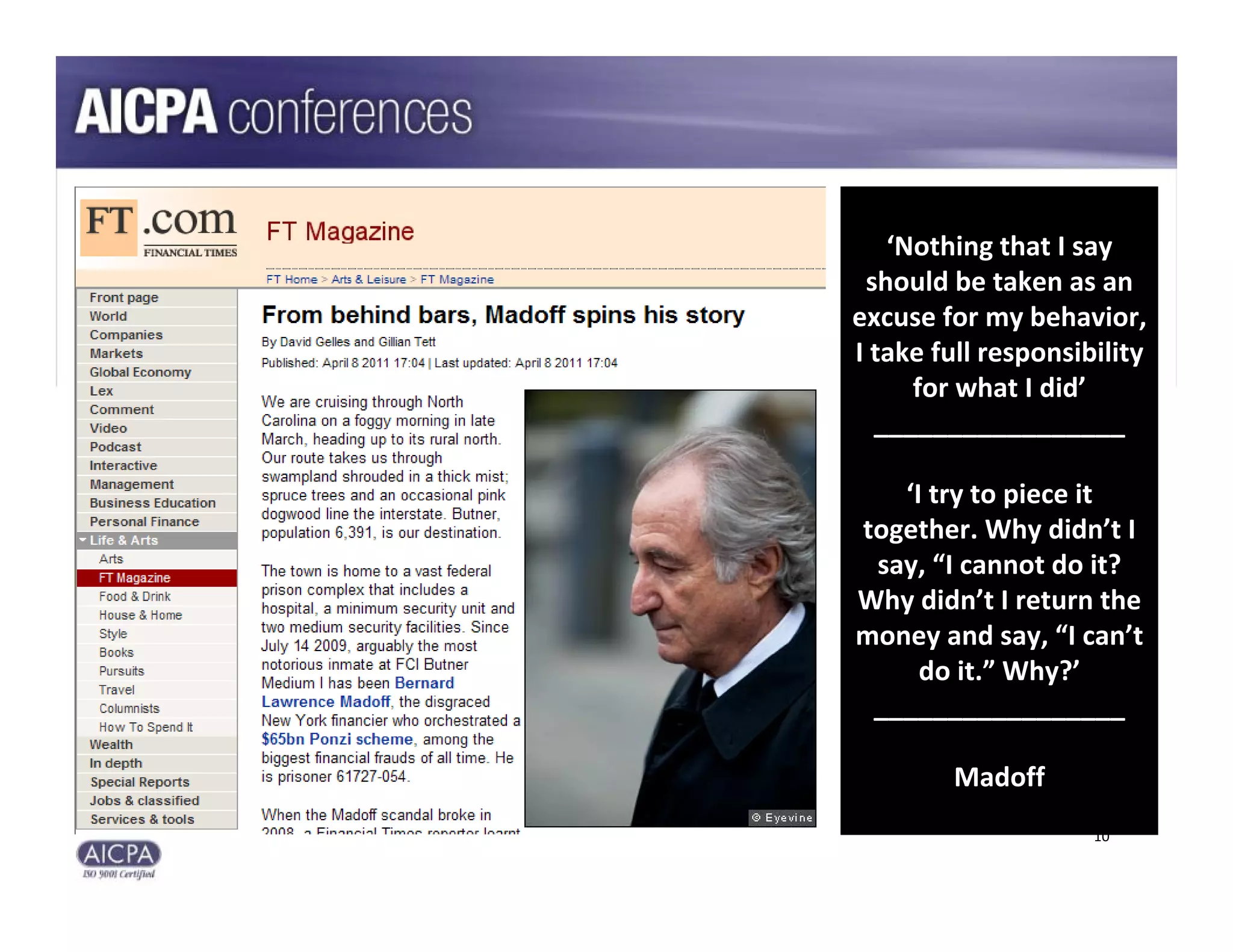

![‘Look, I am not a banker. But I know that billions of

dollars going in and out of a bank account is something that

should alert you to something. [They] got all the financial

statements. [They] could have seen – I was using them as

custodian, and they never questioned it.’

Madoff | Financial Times | 4/9/11

$6.4 billion lawsuit, filed in federal bankruptcy court, claims that the bankers at

J.P. Morgan discussed the possibility that Madoff was operating a Ponzi scheme

“While numerous financial institutions enabled Madoff’s fraud, JPMC was at

the very center of that fraud, and thoroughly complicit in it”

115‐page lawsuit by Irving Picard | Bankruptcy Trustee

11](https://image.slidesharecdn.com/sgaaicpanationalcfoconference2011-110620164125-phpapp02/75/Understanding-the-Latest-Developments-in-Financial-Fraud-11-2048.jpg)

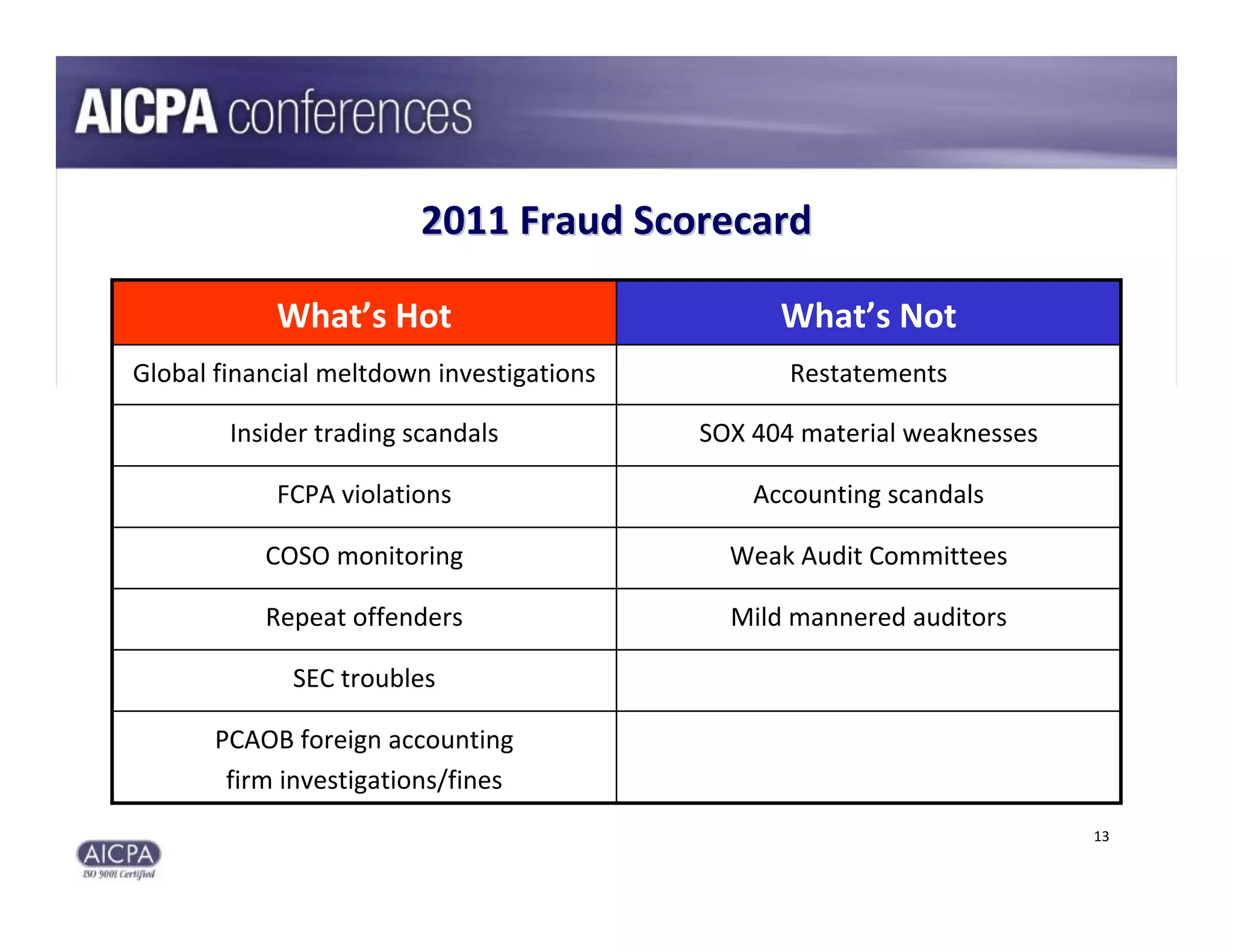

The document highlights the evolving landscape of financial fraud, with a focus on prominent cases and regulatory responses from organizations like the SEC. Notable events discussed include insider trading allegations against Raj Rajaratnam and the collapse of accounting firms due to improper practices. Additionally, it emphasizes the importance of compliance and ethics in financial reporting, as well as the introduction of monitoring guidelines and the increasing enforcement of fraud prevention measures.